A technical perspective. The monthly RSI is 93 which is hugely overbought. Although the business is doing great, the risk reward is not favourable at the moment for an investment. Maybe wait for some time or price correction.

12 Likes

@ayushmit . Did you ask their management to start with concalls once again? And any progress on the demerger when you met them at AGM?

Regards.

1 Like

Yes, he did say that they will start with investor presentations. Demerger may happen in next 2-3 months

16 Likes

They acquired a hotel company with nil turnover in CP Delhi. I wonder why! It may be a store, but who knows. Does anyone have any idea?

TNS HOTELS BS 2021.pdf (965.6 KB)

TNS Hotels has in its Annual Report shown cost of land in its books of accounts at Rs 2 crore. (market value would be higher). This piece of land/property could possibly be at or near prominent retail location.

3 Likes

Yeah lets hope so. What was your reason to exit?

No particular reason per se, several fators…it was 5x for me, bought @ 50,I wanted to take away some gains. Also, I wondered if the company has been doing so well lately why in last 15-20 years it has failed to trade above its IPO price and have fallen back quite a lot in these years too. I took the profit and pared my home loan. It has risen more after I sold but I was satisfied with the 5x in 10 months.

2 Likes

Direct communication to clear all doubts of shareholders, love the clarity of message. It shows how serious the management is about the perception of company. Also, looks like company is having big space for current office which it wants to sell and use for debt reduction.

Overall, a great note to disperse any doubts.

5 Likes

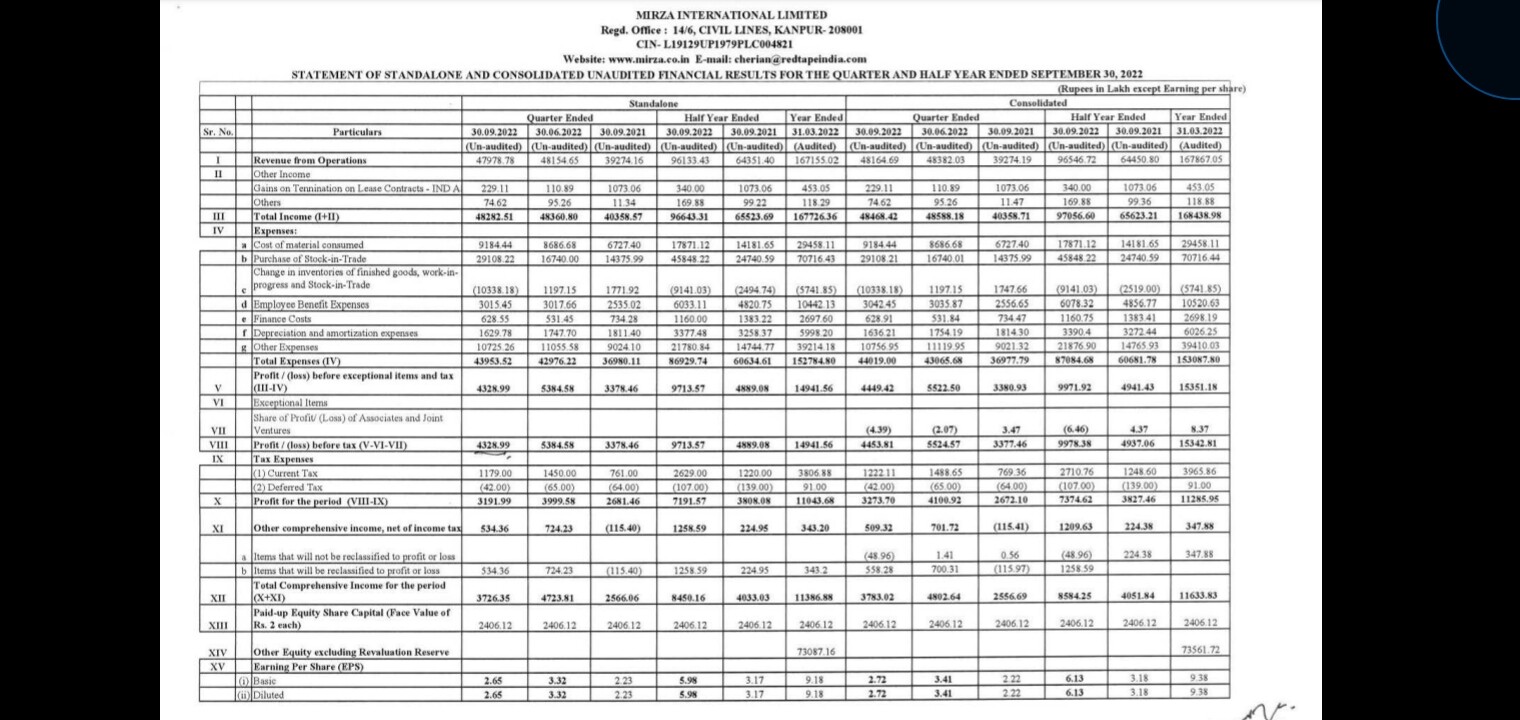

Decent YoY .

QoQ is lower but there is significant difference in purchase of stock in trade compared to previous quarter or previous years same quarter . My idea is that its because of the festive season in Q3.

9 Likes

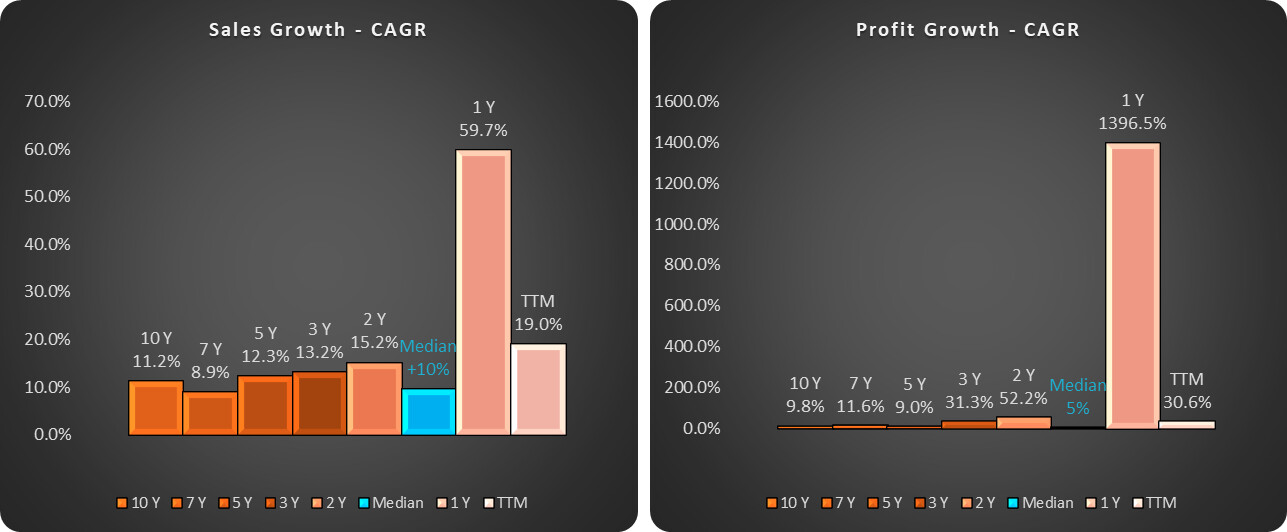

Growth and Profit visualized over the years.

There was clearly a big leap in the last year or year and a half. What’s interesting is that the new level of performance has somewhat sustained. The TTM numbers continue to punch above the medians down to the last quarter.

Has someone tried to understand what were the main triggers?

My take;

- Change of guard in Management

- Debt reduction (PAT positive)

- eCommerce Success

- New Stores + Success in Franchising

Were there more that I may have missed? More importantly is this new level of performance here to stay?

Best!

6 Likes

2f57b47f-f9d2-43dc-bd00-84b4dc9a501d.pdf (563.2 KB)

Really hope this is a genuine mistake.

@ayushmit

Your post has helped me in building further conviction in the story. The Co.'s quest for becoming a fashion Co. opens enormous opportunities across multiple products for Mirza. The Co. has already walked the talk & created decent value if one considers the happenings over last ten years or so. Red Tape from being just an inhouse brand for men’s leather shoes manufactured by the Co. is today largely a brand the Co. uses for multiple products outsourced by them! The marketing infrastructure is already in place & constantly being ramped up to push up volumes. Clearly a scalable business model!

Any idea how much of their garment sales are manufactured inhouse? If memory serves me right, they did have a couple of garment manufacturing units earlier.

23 Likes

Hi @RajeevJ ji, sorry missed replying earlier. Yes, it’s interesting the way the company has grown the branded business. Recently I was traveling across 2-3 states in North India and we could see 3-4 stores at locations we never expected (eg Solan). Recently the co opened another large store in the center of Lucknow city (this one would be having very high rentals)…they now have 4 large format stores in Lucknow.

I hope they can open up and share more metrics about the business.

I don’t think they are manufacturing any of the garments. Infact since Shuja came into the business, he has done things very differently. The sports shoes are also outsourced from places like China, Bangladesh, Vietnam etc. By doing this they are able to focus on designs etc and bring fast changes.

Ayush

38 Likes

The stock has started to make lower low n lower highs which is a sign of stage 4 down trend. today it managed to open below 200 dma with 10% gap down. somehow it managed to close above 200 dma. So technical analysis says bearish time ahead.

Also a video on technical analysis on Mirza International. Giving some perspective how to use stage analysis. One needs to identify probable tops and have an exit strategy unlike Abhimanyu.

Disclosure: Not invested, Didn’t study fundamtally, No recommendation. Moderators feel free to delete the post if dislike.

6 Likes

@RajeevJ Sir, I am unable to comprehend the reason of the downfall in Mirza international share, while fundamental looks intact. Any specific reason you can share that led to stock downfall (Note- This is my first small cap investment, and new in market)

I can add a bit although question is directed to Rajeev sir.

- Despite the current fall stock is up. 2x in last 1 year. After such steep rises stocks can take breather in middle as participants with shorter time frame (momentum chasers) get out & are replaced by investors with longer time frames

- This is not isolated. Have a look at other footwear cos like campus. They have also seen a huge fall

- There can be some concerns about discretionary spending going down due to high inflation

- As per my channel checks co is doing fairly well biz wise in Q3 as well as per limited discussion with some store owners & investors who have talked to such store owners

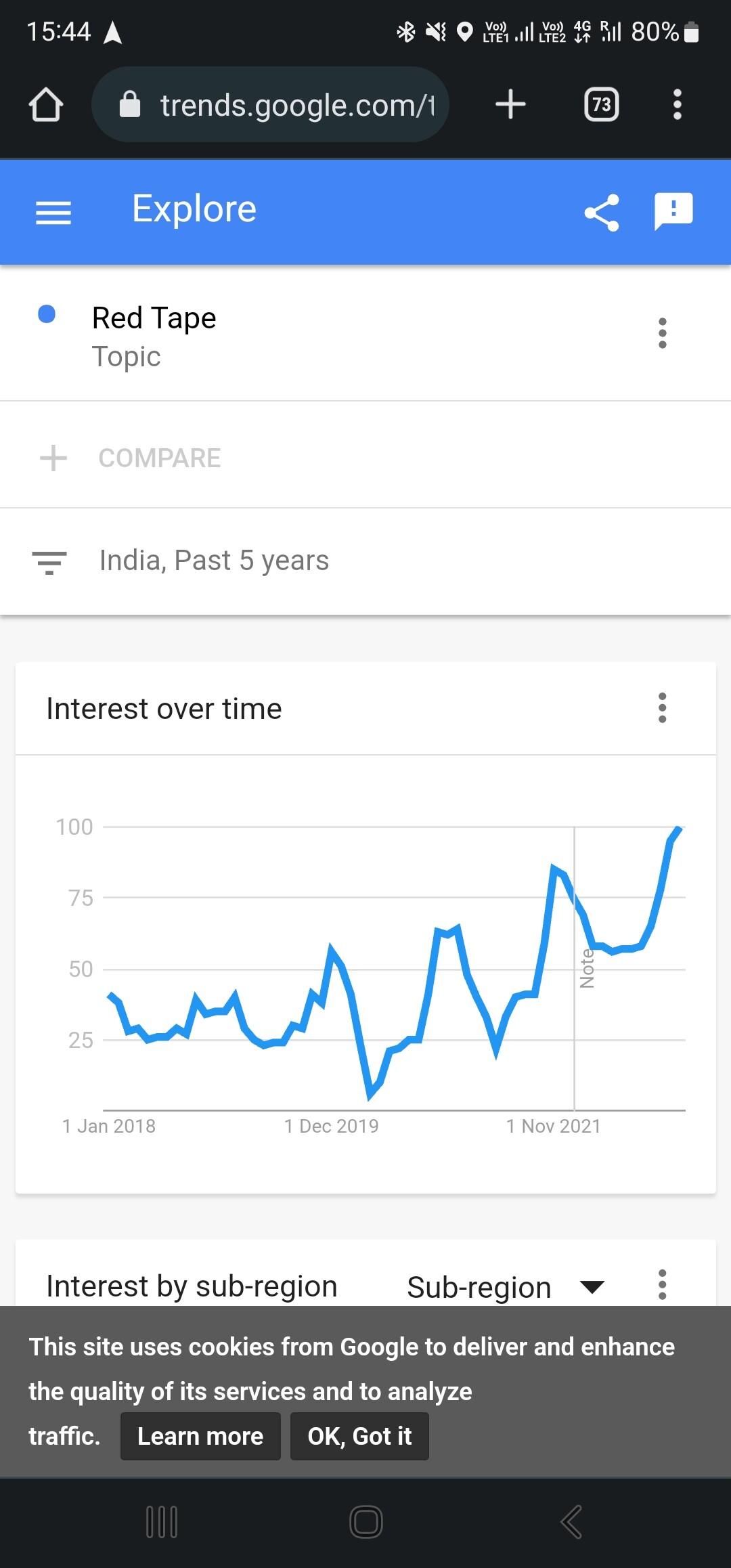

- You can see on Google trends that the longer term organic interest of indian public in red tape brand is at an all time high right now.

Whether and to what extent this interest translates to actual buying will be revealed post Q3 results - This is actually not such a large co mcap wise. Smallcaps can fall decent amount even on smaller selling. Even other cos with strong biz momentum like Navin fluorine, Gujarat fluorochem have fallen below 200 dma.

- Could be a market wide adjustment to higher interest rates (discount rates going up will drive down multiples no matter what, incremental capital might go to bank FDs with some banks offering 8-9% now)

At end of day, biz has to speak for itself. If co can grow 20-25% then i don’t see how these prices or multiples will last. If co cannot deliver 20-25% growth then i personally would be happy to sell out since my style is more of biz momentum.

Disclaimer: invested & biased. Might sell without prior notice.

22 Likes

Thanks @sahil_vi, you hold some valid points. Will have to cut out the noise and focus on business growth. Short term macro will be offset with long term yields

1 Like

This is a forum where we discuss stock ideas. We obviously hold positions in many such stocks. Some of the members here have a good following on VP as well as Twitter etc. Does this mean that they are pumping & dumping stocks? Hitesh Sir discusses what he owns on the most read thread on this forum. Is he pumping & dumping? Sahil clearly said that he’s invested & biased. He isn’t forcing you to buy anything. It’s not right what you said.

3 Likes