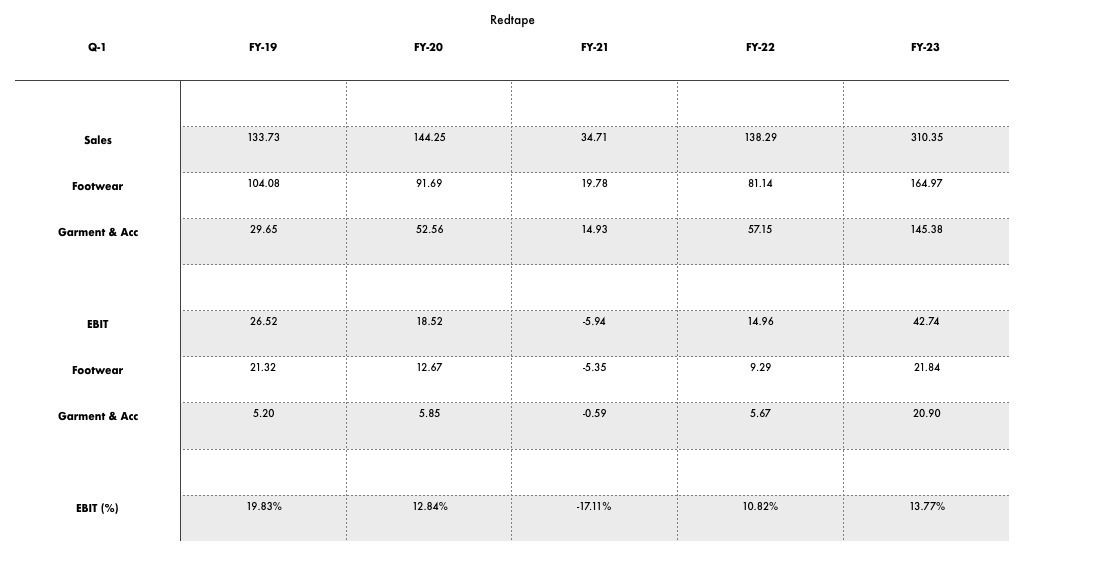

9% YoY growth in garments (below par… tbh their range is quite impressive… visited a store recently)

50% YoY growth in profits for the 2 divisions (23crs to 36crs)

Q4 ROCE has improved from 7.5% to 11.88% YoY

Margins have also improved YoY from 9% to around 12%

Buildup of inventory and debtors, should clear out by Q1 most likely. Debt reduction by 62crs (net)

Broadly similar OCF (hit due to #6 above)

Overall, good show. Maybe a bit more of investor communication and this can be a prime example of re-rating.

EDIT - Please don’t compare Q4 with Q3. Courtesy Diwali and festivities in Q3, its usually peak consumer season in India. What’s important is that RedTape and Garments are consistently showing topline growth.

Mr. Farzan Mirza. member of the Promoter Group of the Company. on 07.06.2022. regarding disposal of 5.00.000 (0.42%) equity shares of the Company on 06.06.2022. by way of gift;

Mr. Tasneef Ahmad Mirza. Promoter of the Company. on 07.06.2022. regarding acquisition of 5.00.000 (0.42%) equity shares of the Company on 06.06.2022. by way of gift.

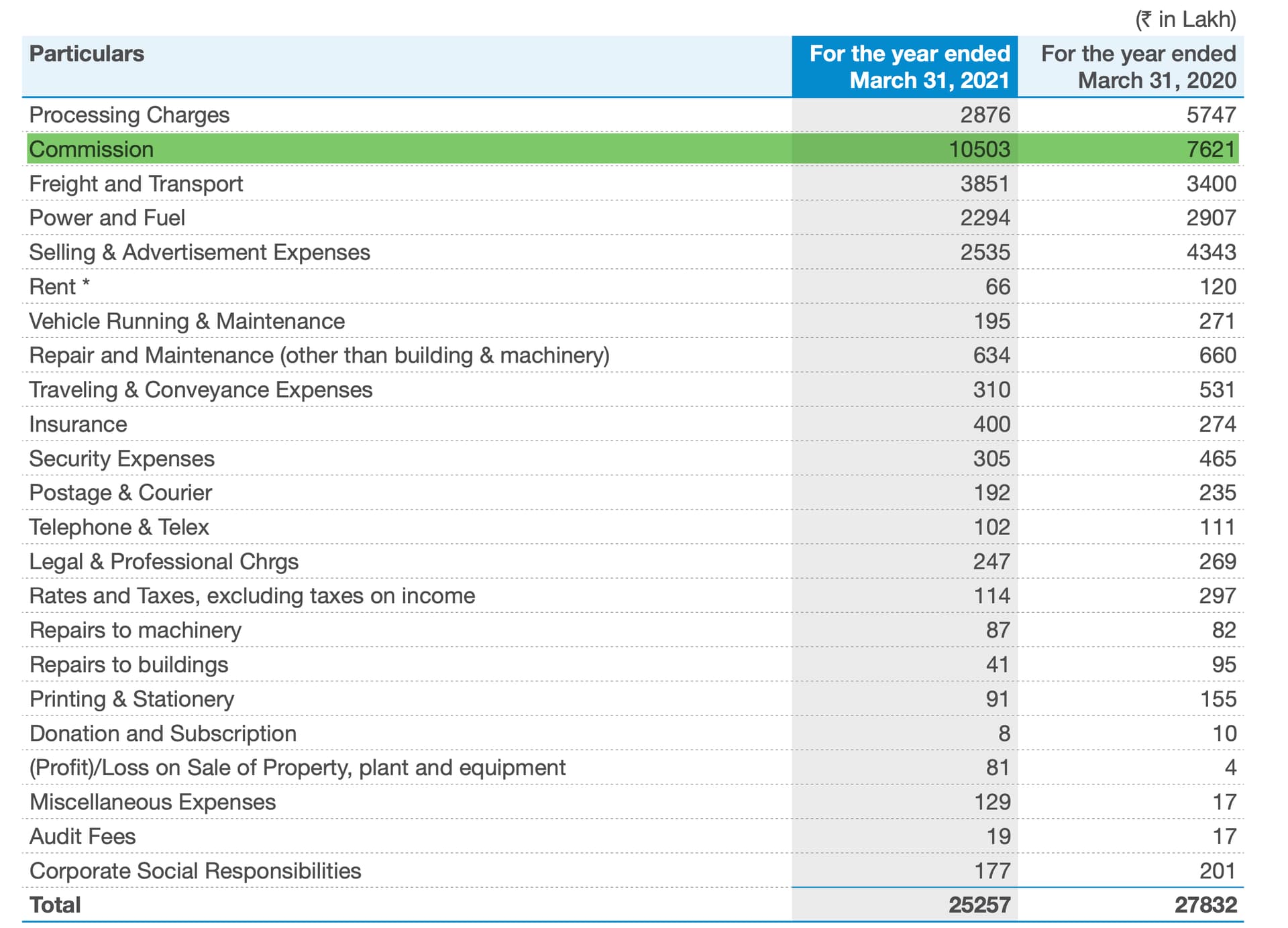

I am assuming this commission is different than the “guarantee commission” promoter takes since 105cr is such a significant amount to be a “guarantee commission”.

Can any one of you throw lights on what this commission is?

I can’t be 100% sure but going by the fact they sell on platforms like Amazon and other ecommerce site, this “Commission” may be referring to “Commission” being charged by various platforms.

Similar to relaxo, I was expecting 2-3x growth in 5 years. This script gave me good learning relate to importance of governance and management.

I still foresee good growth within this sector. Its up to the management how much they want to tap this market aggressively. But, based on my long journey with this script, it still does not qualify to be in the core portfolio by ticking all the criteria. Hope it helps.

Disc: I am invested in this counter around 15 Rs. So my views can be biased.

Commission expenses over here are franchisee commission which is 25 % of sales for every store… Given the debt has reduced considerably the guarantee commission is 4 cr for current year as per the RP transaction filing.

What is the reason apart from past corporate governance issues that Mirza is getting mere 2x sales as compared to peers like Bata, Metro, campus etc. getting around 9x sales. Is it because its primarily into leather shoes and there is some terminal value risk associated with it? And can it ever get valuations similar to bata, metro if recent performance is maintained and further governance issues do not come up?

Leather shoes make up to 20% of total footwear sales (which are approx. 40% of total sales in Redtape) - so cumulatively 8% of total sales.

In my humble view, we should not assume that if any stock is trading at hefty valuations, other stocks will follow that. Primary focus should be on the growth of brand and then compare it with peers.

Once Redtape is listed separately and if at all they start doing concalls and provide more disclosures through investor presentation, it might command certain premium.

Governance issues are often raised during downturn of any business/company.

Disclosure - Holding from lower levels (<100) / won’t add more before redtape is listed.

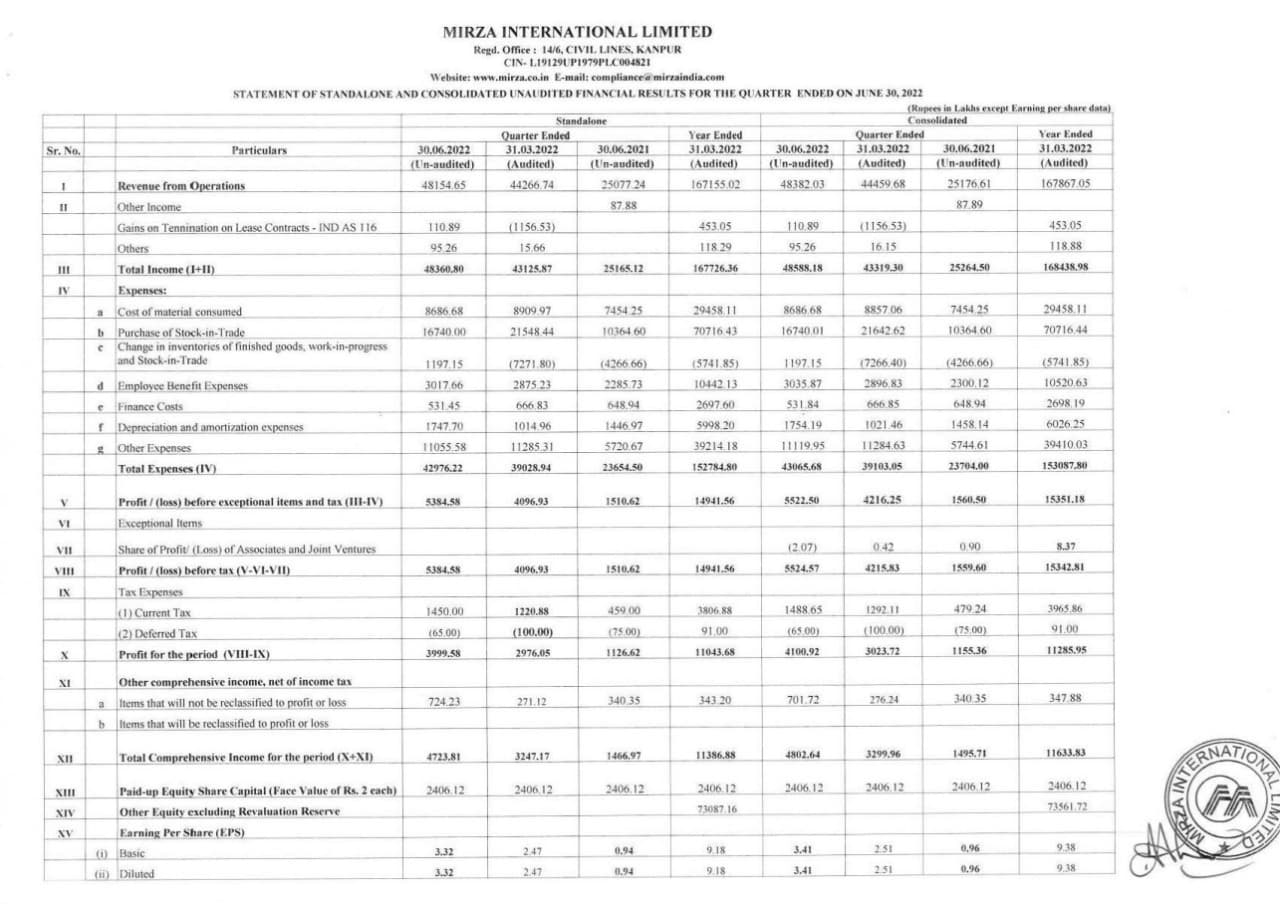

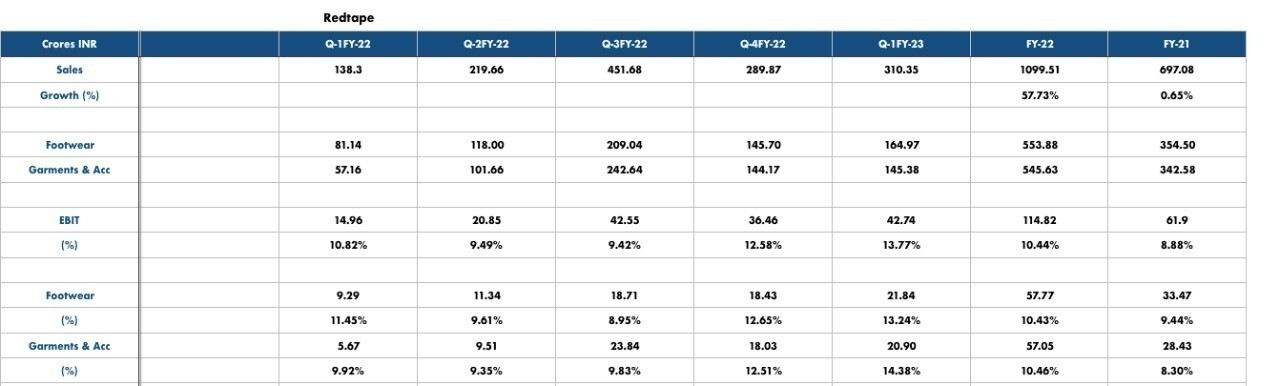

Good results but nothing surprising in my opinion. Q1 last year was covid effected and this q1 everyone is revenge shopping. I am not sure to what extent their improved performance can be attributed to managements efforts. Will have to wait a few more quarters

Disc: invested

I traveled to Kanpur to attend the AGM of the company. It was a formality kind of thing as it was largely just employees. Just 1 more investor had come from Mumbai apart from us.

Suja Mirza (takes care of Red Tape) was there along with Faraz Mirza (take care of export business) and they seemed to be the key people running the companies. Few key points:

China was closed post Covid and imports really dropped. This has been a big welcome change for the domestic shoe industry and hence most of the cos have started doing very well. Earlier there was dumping of poor quality goods from China and un-organized players in Delhi used to import and create unhealthy competition. Now domestic cos are doing well.

We added 72 stores in Red Tape. Count is about 350-360 now. Shift from shoes to garments. We are doing very well in garments and are a fashion company now.

Export team is very bullish and local RM availability is helping us. We can grow multifold in this segment too.

There is huge opportunity for exports over next 3 years

For red tape - we are doing very well and see a strong growth ahead. Plan to open another 40-50 stores and may close about 10. We are largely a north India brand but now plan to go South too. Opening in Mumbai, Karnataka, Bihar etc.

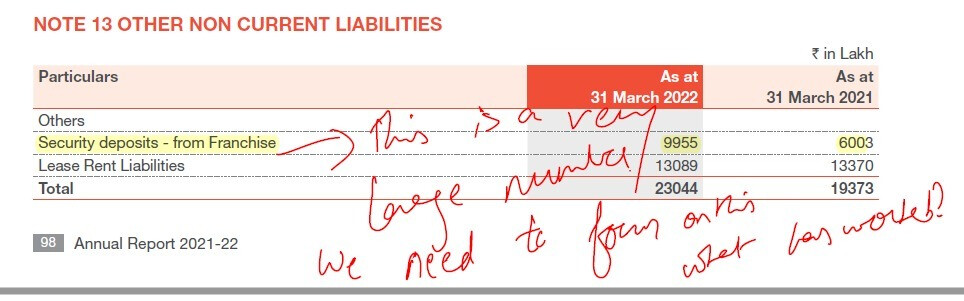

It was interesting to see the sharp jump in deposits from franchisees in the latest AR

Shuja in his usual self was very ambitious and bullish about things. As per him, the franchise model is doing really well and there are lot of people wanting to open more stores but we are going in phase manner.

Disc: Invested in family acs. May change position randomly

Thanks Ayush for sharing your thoughts after attending the AGM. It’s a big help to get first hand info. The growth potential in the garments division is indeed exciting. As it is, Mirza is amongst the most attractively valued branded footwear players in the country as can be seen from the data below, which includes the tannery operations which adds a certain amount of dead weight & brings down the efficiency ratios. Post the de-merger, the Red Tape numbers will only get better.

The stock may have run up some distance, but as the perception changes to Red Tape being more of a marketing Co. with an asset light model, its valuations will only get better.

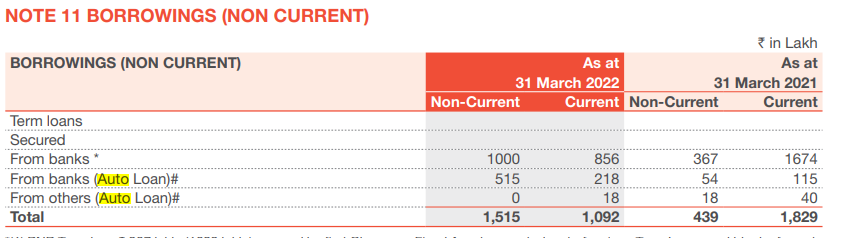

While they have paid almost all long term borrowing outstanding by FY22, 15cr outstanding is shown as auto loan. Can someone help me understand is it normal a 15cr auto loan or it means something?

You always have to look at it in relation to overall business size. It is big for a company with 50 crore revenue but not so big for a company with 500 crore sales.

Also, from the screenshot you shared, it seems the auto loan is only 5 crores, not 15 crores.