everything in this screenshot has been discussed & priced in for about 4-5 years now. If you see carefully, the screenshot is from FY17 annual report Just for a quick recap:

- CSR activity - many corporates have their own foundations.

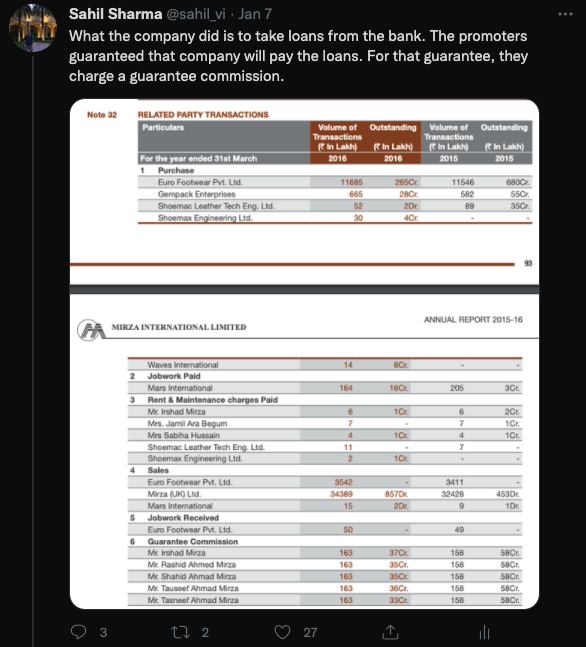

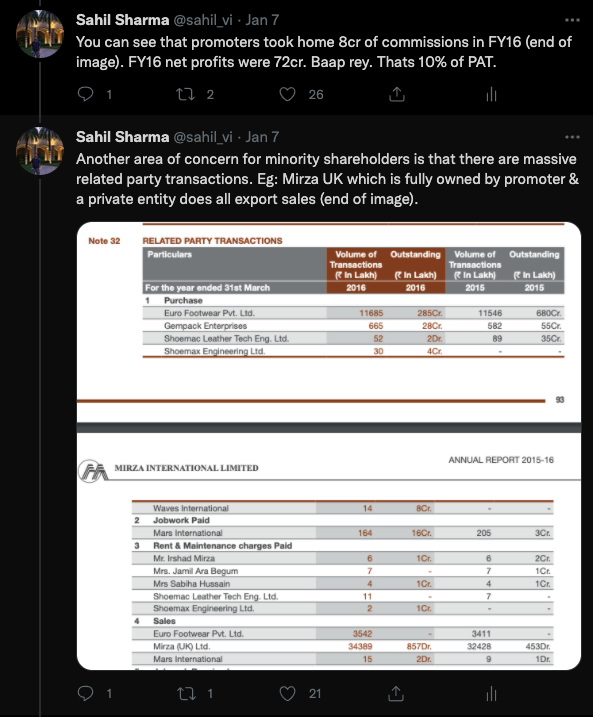

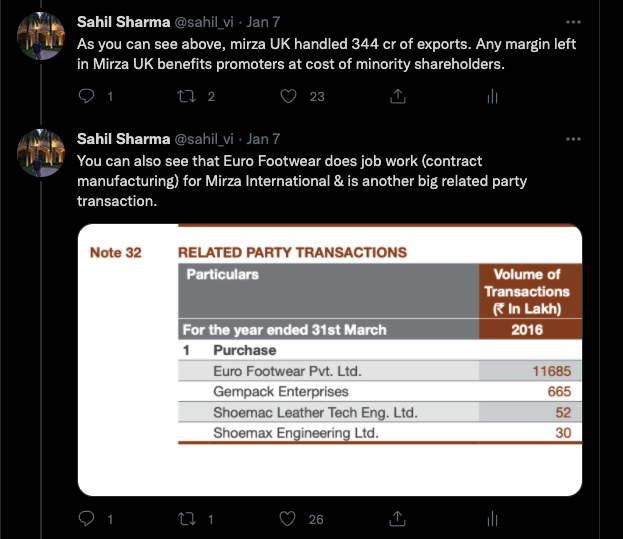

- Company has 6 plants but still does job work - If the investor took the pains to listen to the concalls investor would understand why this happened. Euro footworks was a competitor & mirza wanted to align the competitor with themselves so they took a minority stake of 49% in the company. Although this is a related party, it is controlled by a private individual. Since mirzas own 64% in mirza international, it is in their own self interest to retain more margins in mirza. Nonetheless this remains one of the corporate governance overhangs. Once Redtape demerges though this would go away since jobwork would be done for leather shoes & will most likely end up in mirza international, not red tape. For me personally, red tape is the company worth owning going forward. I would be looking to exit mirza international post demerger.

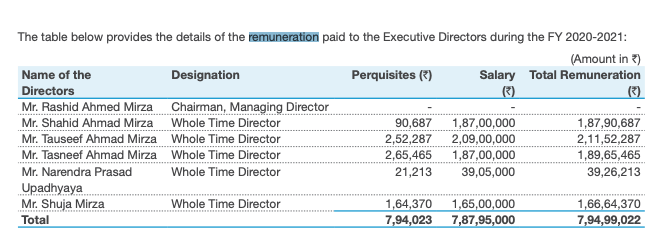

- Toal remuneration of 8.5 cr to mirzas which was 12% of PAT in FY17 has been reducing for some time. Take a look at this screenshot of FY21 annual report. Specially look at Mirzas comp:

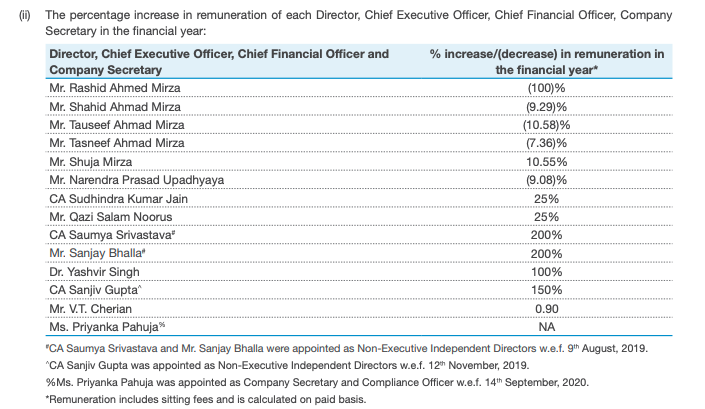

some of them have gone down by as much as 100%. Only one going up was Shuja mirza who is the work horse running the business.

Total remuneration to Mirzas has gone down from 8.5cr to 7.95 cr. Notable is fact that Rashid mirza takes home a salary of 0 now. - The guarantee commission has been the biggest problematic issue. It has gone down from 8cr to <2cr this year. Red tape should have no guarantee commission since it will be a cashflow machine which is able to grow from internal accruals & would not need debt. For me one major anti-thesis is if guarantee commission does not continue to head downward over the years winding down to 0 in 2-3 years.

It certainly can and will be. Aggregate of these experiences is reflected in same store sales growth which has been wonderful for Red tape (around 18-20%). Much higher than peers.

6.

Not a fair comparison since AFL does not have the profitability. As i have shown in segmental analysis few posts ago, Red tape has pretty good balance sheet, growth & profitability.

7.

I am personally offended at this insinuation of not covering the negatives properly since you mentioned twitter threads & i am the only one who made a thread in the last few days. The corporate governance issues for mirza have been covered front right & centre. I have also meticulously explained that this is a high risk high reward scenario & that it is important for investor to position size the bet since this is sort of an all or nothing bet. If corporate governance improves on ground, you get a mega upside, if it remains same, you lose everything.

Please dont tell me that the negative side has not been discussed at length, because it has been.

There is no hope involved here, only facts. Please listen to the concalls that happened until Feb’20. Shuja mirza is the one who has been patiently answering investor concerns on CG on all calls, talking about guarantee commission going down, talking about demerger.

9. For those that believe that there is no redemption, once a chor always a chor, please do due diligence & study existing threads on valuepickr. ![]()

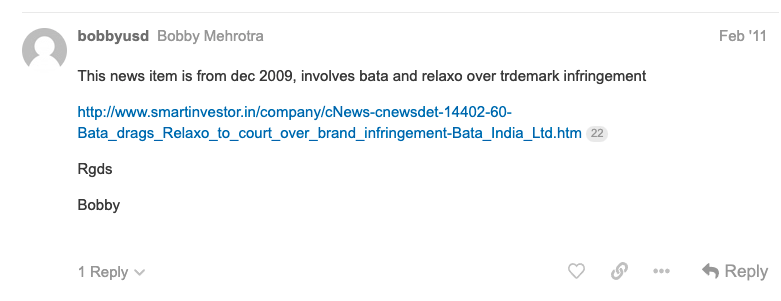

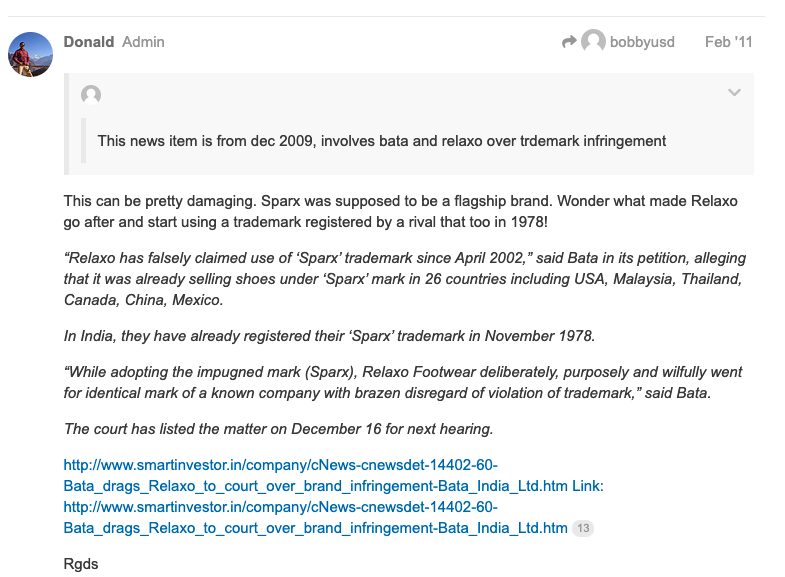

![]() Study the relaxo thread to see how CG issues have evolved. Quoting from the relaxo thread:

Study the relaxo thread to see how CG issues have evolved. Quoting from the relaxo thread:

Does the word guarantee commission ring a bell?? Evidence suggests that as long as managements walk the talk on improving CG, rerating occurs. Look at APL apollo, look at borosil group (people mention the real estate transactions even today, despite clean up that has happened & is happening). Whether you believe that such changes are true change of heart or window dressing a pig with lipstick is a matter of personal choice. I am in neither camp. I am not eager to make up my mind. WHat i will do as an investor is actively seek evidence from all investors AND sellers to understand what conviction or concerns they have. And then try to ascertain how much truth there is to such claims. Attaching a few other screenshots of relaxo CG concerns raised on forum.

10.

Market works on probability not possibilities. It discounts current evidence. Evidence is that CG is improving:

(i) guarantee commission going down

(ii) promoter remuneration flat for 4-5 years. Key promoter remuneration down to 0

(iii) Merger of UK privately held subsidiary into mirza international

(iv) jobwork will also stay in mirza int & red tape would not have lot of RPT in my understanding.

11. We have seen prior examples (Relaxo, apl apollo, borosil twins) where cleaning up the mess does result in sustained rerating. There is redemption even for poor CG past if they walk the talk. Whether tthey are walking the talk or not is something which investors need to develop their own conviction about. I for one am not sanguine about this investment. I am actively seeking disconfirming evidence which can show that they have other skeletons in the books which are not priced in. Havent found any yet. If i do , this forum would be the first to know.

12. Let us also discuss why I decided to invest in this company despite the CG concerns (my personal decision might not work for others). Red tape is growing at 30% CAGR. I Expect topline to be at least 3x in next 5 years. The valuations are at around 2x sales. All peers are valued at > 10x sales. The CG is headed in right direction. If it continues to head in right direction, i expect valuation gap to narrow. a rerating would not be out of ordinary. My upside is multifold. My downside is in the case where CG continues to become worse. I lose all my capital & it goes to 0. Hope the disproportionate risk reward setup is clear. Still i have position sized to 3% since loss of capital is a real possibility here.

Disc: invested, but very hyper aware of the possibility of capital loss so position sized to 3% of portfolio.