Minda Industries has posted good Q3 results.

Ref: https://www.bseindia.com/xml-data/corpfiling/AttachLive/1960a075-de67-4c0c-ae01-0a2f0d656cd2.pdf

Minda Industries has posted good Q3 results.

Ref: https://www.bseindia.com/xml-data/corpfiling/AttachLive/1960a075-de67-4c0c-ae01-0a2f0d656cd2.pdf

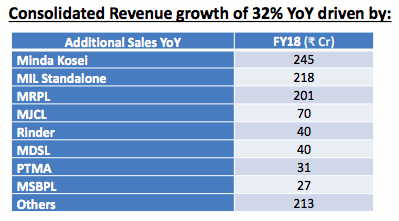

Topline growth is 26% check footnote in consolidated results

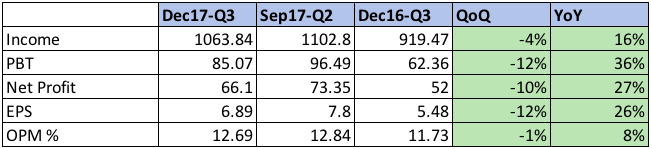

Nothing significant …if you take into account dec2016 was a demonetization quarter as earnings in dec2016 for most companies were abysmally low. QoQ all parameters are low and YoY results are okish. Lets not forget last quarter was GST quarter and Expected to show good growth QoQ as post the GST qusrter sales should have picked up . But if it corrects can look at …

For a cyclical business we should consider the YoY.

This suits to the entire street isn’t it ![]()

Btw, just to to give a headsup on DeMon quarter in which almost all the companies posted less nos. Minda Industries posted ~55% rise in net profit.

Dec-15 Net Profit: 28.85

Dec-16 Net Profit: 44.74 (Oct-Dec DeMon quarter)

I am holding on to this business from the past 3 years been surprisinged almost all the quarters, comp enters in to JV then buys out at a later period. Debt from 3 times in the past 3 years has come down to 0.43. One of the best stock been closely been watching on comp development with diverse pf. Battery business which initially they failed and later on they got in to JV with Panosonic effectively making right use of their assets with new technology. I continue to believe the business will do well going forward but I am only concerned about the high PE multiple VS peers. I would appreciate if any one can share there thoughts on how to play on PE stock.

Discloser : I am invested in this stock

I compared minda and pricol and picked up pricol .lets see

Minda Industries posted strong set of numbers once again.

Consolidated figures:

Other notes:

Detailed results:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/333a3913-6c23-40fa-a459-2efc2837ea72.pdf

Yes @manivannan.g - i have to say now after checking the results that certain companies can go above and beyond what you imagine they would do in the normal course of business. These guys are doing an exceptional job. I am wondering at the way they are maintaining the quality of this balance sheet despite the exceptional growth in both top and bottom line. The operational efficiency seems to be kicking in as explained by the management during their last quarter. Thought they would do 500 Cr bottom line by 2020 but now it could well happen by March 2019. Kudos to you @manivannan.g for your effort in helping many of the fellow borders with your investment rational(and proving me wrong with my rational on why one should consider selling out) - and as you mentioned earlier this could well restart its northward journey. Congratulations to everyone who trusted the management and continued to hold on to their investment despite the turbulent market conditions. Minda is a winner - so are its shareholders!

Disclaimer: Sold out 75% of my holdings earlier this year at around 1100. Balance 25% is continuing to grow my portfolio value.

AJ

My Only question/concern is can they grow exponentially in coming qtrs and years? what special mix of products they have when other auto ancillaries doesn’t have ? and some others are nothing growing at all by the likes of bosch

Whats the contribution of mindarika to sales?

MRPL - Mindarika Pvt Ltd

It’s worth mentioning that, last year MIL had only 27% holding in MRPL, but this year they acquired another 24% and making it as subsidiary from associate.

All segment wise details and the subsidiaries details are available in Q4 investor presentation.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2c1417d3-e409-4c93-b539-b6a66c9b3195.pdf

Q4 conference call:

The record date has been fixed as 12-July-2018 for bonus issue.

Auto-sales for April-May 2018 compare to April-May 2017:

Two wheelers grew : 15.16%

Passenger vehicles : 13.28%

Passenger cars : 14.71%

Utility vehicle : 24.11%

As we see more two wheeler & passengers cars sales, expecting MIL to post yet another robust set of numbers.

Geojit team thinks that the premium valuation to sustain:

Some comments on the opportunities from the recent Govt. safety norms and EV exploration.

In my limited understanding, the company is expensive. Hardly any major global auto ancillary company trades over 20 times earnings. Frankly, I’m astonished that such valuations have been accorded, to say the least.

Yes at the P/E 35.49, it’s quite expensive. I expected this to correct in this mayhem, but it denied. Also, when you take a look at the PEG, it’s at 0.71 and is being supported by good fundamentals. Apart from that the near term things that gonna further fuel are the safety norms, EV and good sales growth in auto-sectors. So, I found there’s more room for growth, hence sticking with my conviction.

Many thanks for the response. Yes, the stock has been resilient.

Overall a good quarter (FY19 Q1) for Auto sector.

Minda Industries acquire iSYS RTS, a leading embedded developers to gain more strength in controller (ECU) business. iSYS posted revenue of 6M Euros last year.

Also, they entered a JV with Kasei (Stake details: Minda: 49.9%, Kasei: 50.1%).