Menon Bearings ( MBL), a Menon Group company was established in 1992 and is one of the few companies in the continent having fully integrated manufacturing facilities under one roof, to produce a wide range of critical auto components like bi-metal engine bearings, Bushes & Thrust Washers for light & heavy automobile engines, two wheeler engines as well as for compressors, refrigerators, air conditioners etc. The company started its commercial production in April 1993.

MBL is listed on the BSE ( Bombay Stock Exchange ) & is globally positioned with business activities spanning 24 countries around the globe. Exporting 35 % of its production capacity, with exports growth at more than 25 % per annum, the engineering capabilities at MBL enjoys strong brand equity among leading OEMs all over the world.

Menon Group is a multi-product, high end critical auto components group with a turnover exceeding Rs 300 crore & globally positioned with business activities spanning 24 countries around the globe exporting 35 % of its production. The Menon Group’s historic commitment to quality and customer service, strong corporate values, disciplined & professional management systems, emphasis on trust in business relations & its ability to meet special needs is recognized the word over.

MBL manufactures a whole range of bi-metal engine bearings, bushes & thrust washers for light medium & heavy automobile engines, 2 wheeler engines as well as for compressors & for refrigerators & air conditioners.

Product range of the company includes:

Bearings

Bearings for Connecting Rods

Bearings for Crank shafts

Flanged Bearings

Trimetal Bearings

Bushes

Truncated bushes for Connecting rods

Ball indented bushes

Bushes for Connecting Rods

Cam Shafts, Rock Shafts

Rocker Arms

Thrust Washers

Washers with Thrust

Face Contours

Ring Type

Thrust Washers.

This information was gotten from their home website. This particular stock popped on one of my screens, and seemed quite interesting.

Fundamentals

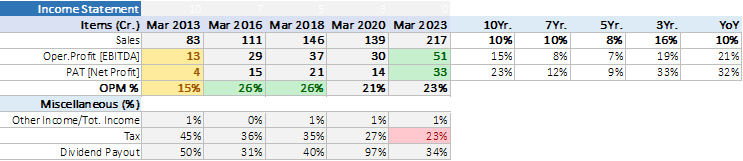

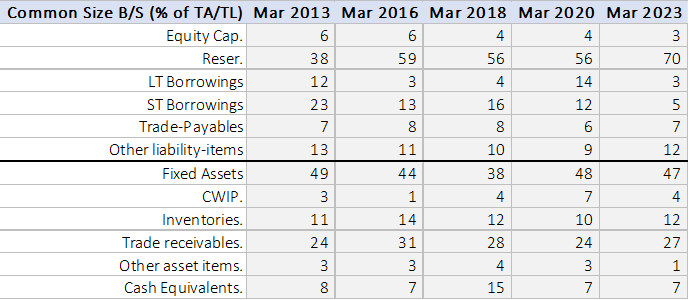

It is a micro-cap with a total market cap of 478 Cr, that has suddenly beginning to show improving OPM’s from 15% in 2013 all they way upto 27% now.

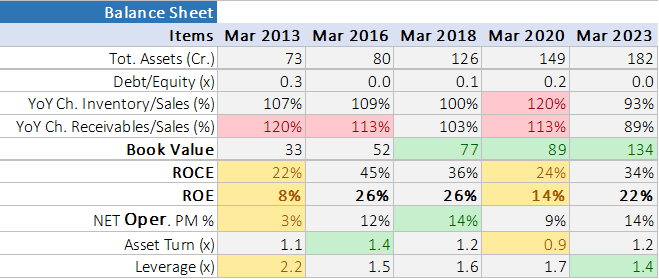

ROE has increased from 25.37% in 2012 to 31.46% in 2016.

ROCE has increased from 17.61% in 2012 to 25.94% in 2016.

TTM Profit at 17.36 Cr

TTM Sales at 118.69 Cr

Although I feel ROE and ROCE in excess of 15% is itself good enough for most companies and extremely difficult to maintain in the long term.

Operating Profit Margins at 26.08% (2016). Highest levels over the last ten years

NPM at 13.4%(2016)

Debt to equity at a manageable 0.24 having come down from 0.69 levels in 2012.

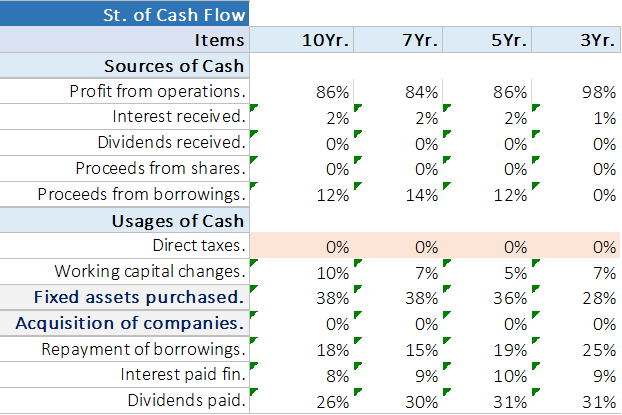

The stock has also strong dividend payouts in excess of 30% over the last ten years. This seems to indicate that they do value the interest of minority shareholders as well.

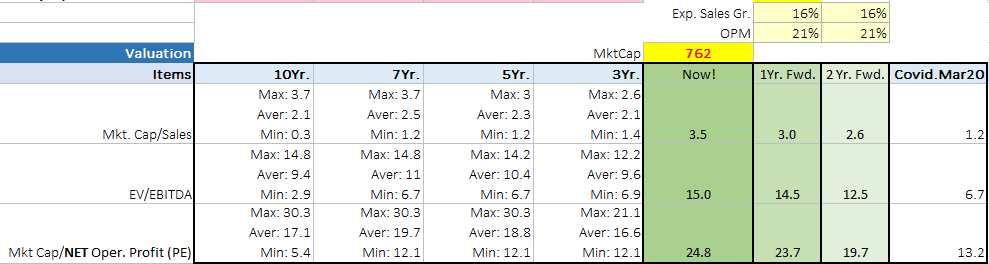

With the expected pickup in the auto ancillary space, I feel this may be a multi-bagger in the making especially at the current juncture. I feel it’s not too expensive currently at 4 P/S for a firm with a high profit margin doesn’t seem like a lot to me. More than that I feel the long term value creation is more important, and if this stock is capable of delivering profit and sales growth in excess of 15-20%, the stock returns may eventually be rewarding.

CAGR Sales over 3 Years 10.22% (This is still a bit dull, I look for a minimum of 15%)

Profit CAGR over 3 Years 61.83%

Promoter Holding 74.67%

Please do provide your insights into this company.

Thanks,

Prashanth