Megastar Foods

Current Price : Rs. 25.4 ( as on 22 Feb 2021)

Market Cap: 25.2 cr

Book Value : Rs 22.3

Stock P/E : 7.4

The Company is engaged in the manufacturing of food based products such as wheat flour, organic wheat flour products and allied flour products.

The Company is located in Ropar (Punjab) and is run by promoter who has three decade of experience in wheat processing industry.

In 2011, the promoter incorporated Megastar Foods in Punjab and its IPO was launched in 2018.

Industry Outlook

Wheat is widely produced cereal all over the world, most of which is for human consumption. According to FAO, in 2014, the total wheat production is 729 Mn tonnes across the globe.

China is the largest wheat producing country with the production capacity of 126 Mn metric tons while India is the second largest wheat producer with the production of around 95 Mn tonnes. India and China together account for around 20% of the total wheat production across the globe.

The food processing industry in India is estimated to reach $482 billion by 2025. With the increasing use of flour in bakery products and the ease of availability of raw materials, there is acceleration in the flour market.

Notable Points

(a) Was awarded as “MOST DEPENDABLE PARTNER” in year 2018 by Jubilant Foodworks Limited

(b) In year 2019, Megastar was awarded for recognition of “EXCEPTIONAL PERFORMANCE” by ITC Limited

(c) The company sells 2/3rd of total production to corporate buyers.

(d) The company obtained international certification which paves the way for international trade. The management envision to develop themselves as Global Quality Wheat Processor.

The Megastar Foods has following value chain:

(1) Procurement : The bulk of wheat is procured from local farms of Punjab and the FCI body.

(2) Transport of Raw Material : The company has its own fleet of trucks to transport raw material and finished goods to its destination

(3) Processing Factories: The Company has state of the art modern machinery at its wheat processing plant in Punjab, India, with an installed capacity of 84000 MT

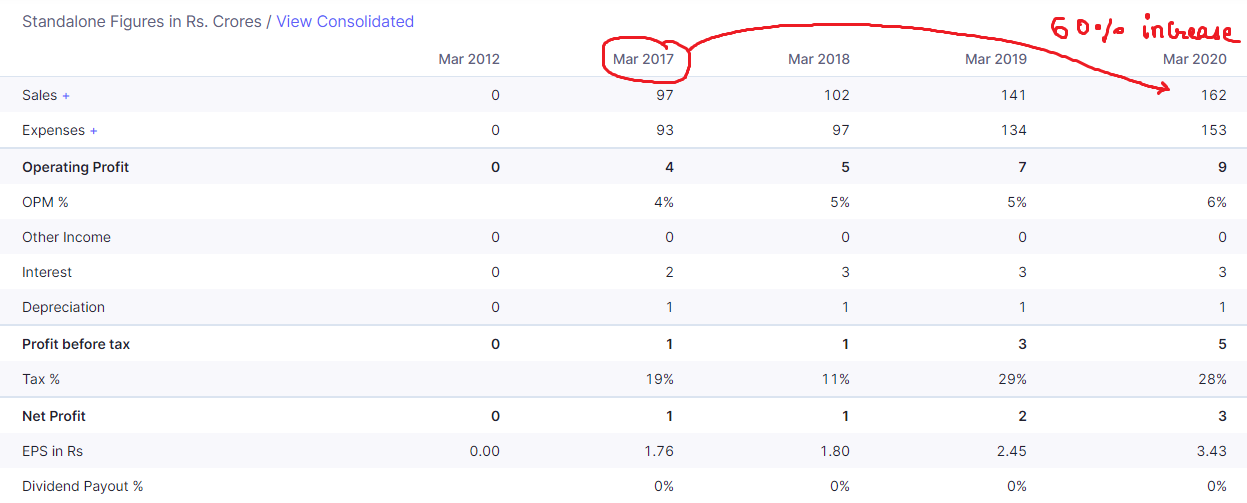

Company Performance

(1) The company has increased its sales by 60% over the period of three years.

Wheat is the most common used food item through out the world. I think that these numbers are sustainable and will only grow if quality standard is maintained by the company.

(2) Company Survival

The company has interest coverage of around 2.5 which means that it has sufficient earning to fulfill its interest requirements. I think that the earnings are sustainable as there food items are always in demand no matter how difficult is the crisis.

You can observe that even in COVID crisis, the company has managed to grow its sales from the previous year

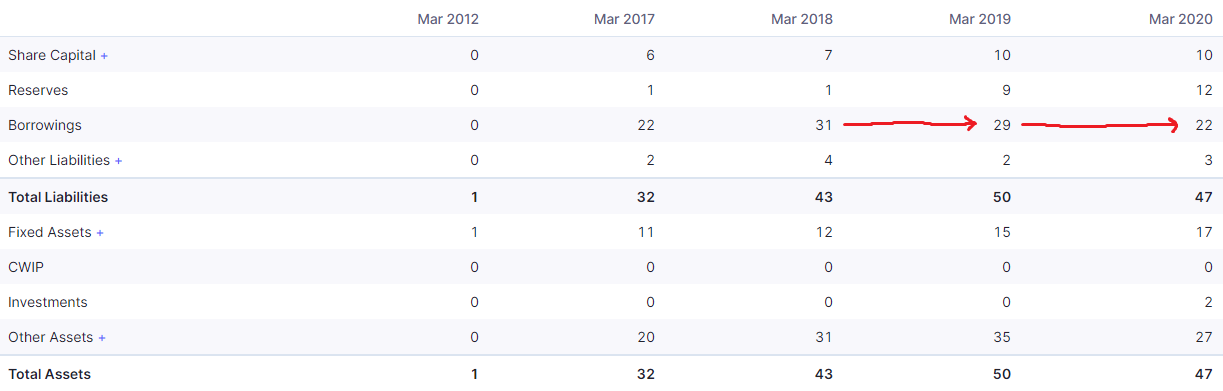

(3) Debt/Equity

The company has debt/equity of 1 which is on higher side.

But if we look into the balance sheet, the company has reduced its borrowing continuously for the past two years. This gives us the hint that the company understands the problem of debt and is taking measures to control it.

(4) Receivables

With increase in sales, the receivables is decreasing.

This is positive sign for the company as it shows now the company is demanding better contract terms for their customers

(5) Promoter Holding

Current Promoter Holding is 68% which is healthy.

Pros:

-

Company has maintained relationship with branded customers such as Jubilant Foodworks Limited, Nestle India Limited, GSK etc.

I think that these brand names will help the company to acquire more customers in the future -

The company claim to have processing machinery from Germany and is making effort to automate its business process.

I have tried to search their employees on Facebook and found some photos working in the factory. There is some credibility in the story and i think one can do further investigation on this company -

They have made investment in Food Laboratory and Security which i think can attract more corporate client as they are very particular about the quality of items purchased

Cons

(1) Raw Material- The raw material used in the manufacture of Products is wheat only and which are procured from suppliers available both locally from mandies and from Food Corporation of India to meet our requirements.

The Price is ever fluctuating and is highly dependent on climate

(2). Heavy investment in working capital

The product is a commodity and in order to standout from the competition, the company need to provide credit and bonus facility to the client which can put strain on the working capital requirement

(3). Electricity, Water and Freight Expense the major expense which varies considerably throughout the year

(4) Uncertainty over farm law

you never know what turn can the law take. The environment is still uncertain but there is hope that the wind will favor Agri Industry

Ratings

CRISIL has given BB+ (Stable) Rating

LAST POINT

The company has incorporated subsidiary Magapacific Ventures which deals with production and trading of packaging material. The subsidiary has reported revenue of 19 Lakhs with 0 Rs Profit.

Here the company is trying to integrate value chain i have personally seen some companies taking these types of move to keep cost low. But i hope they don’t dilute their vision to develop themselves as Quality Wheat Processor.

I request seniors to contribute and share their expertise, will like to have your view on this.

I have not invested yet but keeping in track of the new events related to the company