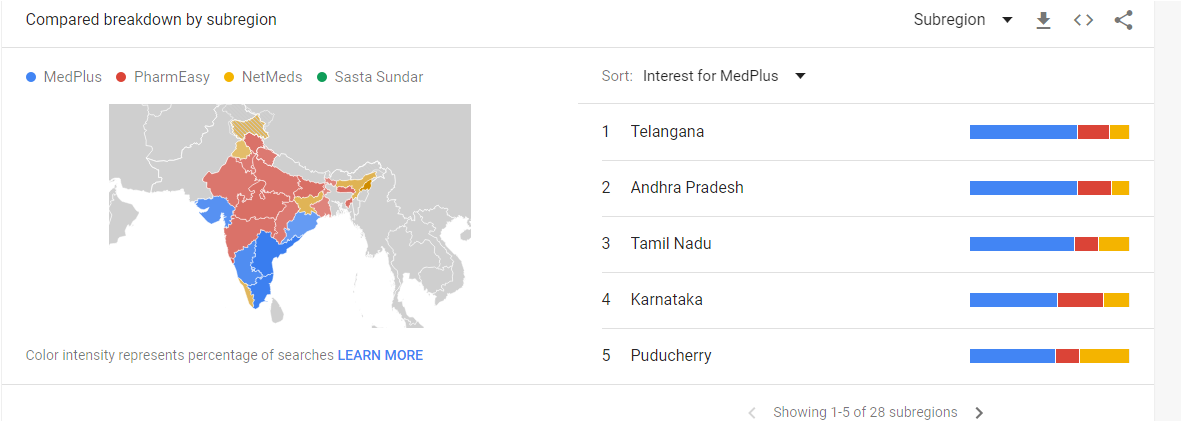

Did some google trends search. MedPlus is absolutely dominating the locations where it claims it is currently the leader:-

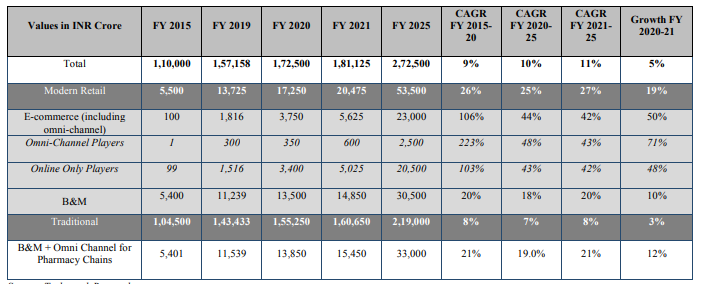

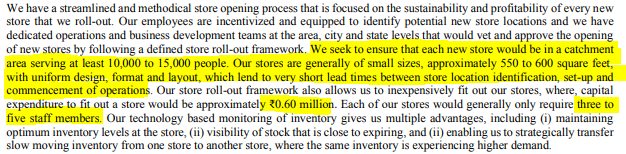

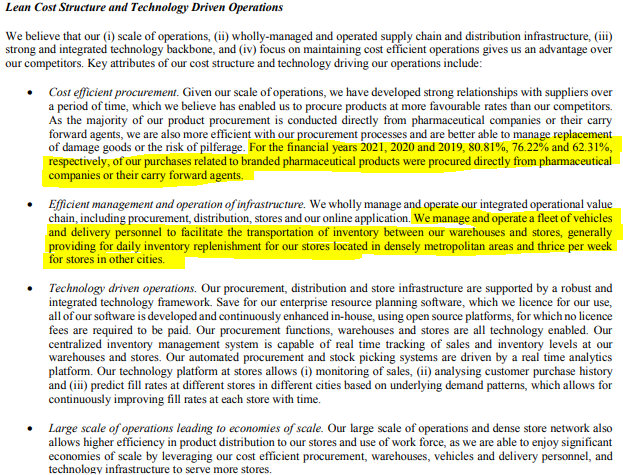

Also the DRHP is interesting. Some screenshots.

-

Omni channel has recorded the highest growth CAGR among all peers and the article posted on Reliance’s strategy to go omni channel via tie-ups with traditional kiranas indicates some form of superiority of the model over pure play epharmacies:-

-

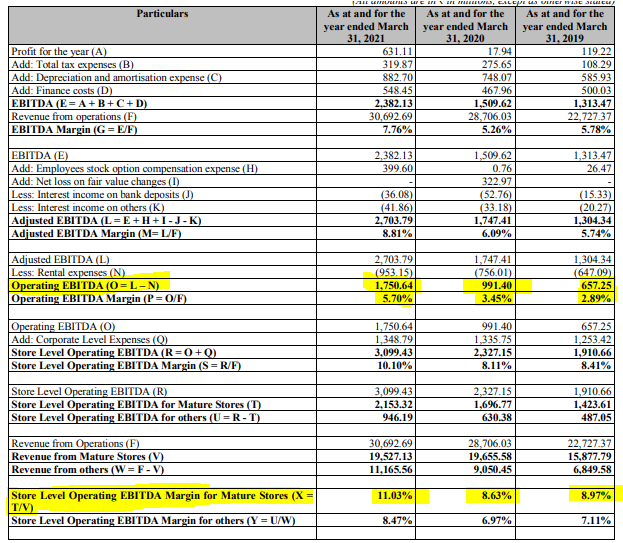

Financial metrics. I think the most important metric here is operating EBITDA and mature stores EBITDA (free cash flow machines). As can be seen that while the margins are high, due to sales growth out of nearly zero incremental capex, the ROCE is >60%.

-

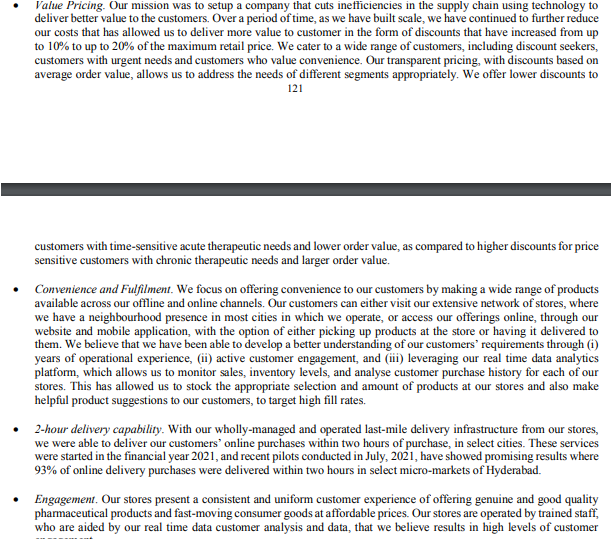

Competitive advantages

Interesting. Reminds me of IndiGo. They placed huge orders of one aircraft type, which just led to huge efficiency gains overtime.

Specifically on the first point - this advantage would not be available if online pharmacies deliver via their offline unorganised partners. In that sense omni channel players will benefit unless ofcourse online pharmacies do a centralised procurement even for their offline partners (difficult)

Why 2 hour delivery is important? Because the discounts are lower on acute drugs (urgently needed) vis-a-vis chronic drugs. And you can only deliver it if you have a well organised B&M infrastructure.

What are competitors doing?

Basically copying what MedPlus and Apollo are doing but the target is very small and notice how they’re not targeting cities / metros where MedPlus is dominant.

I don’t see this model driving being sustainable at all. While it may be easy to scale in the short-term but cost advantages available to at-scale players like MedPlus will eat the market share.

(article link Tata-owned 1mg, PharmEasy go offline for omnichannel presence - The Economic Times)