Hi Friends,

In the recent times, there have been couple of articles on Avanti Feeds (Dalal Street magazine and TV interviews) and I have been thinking that the company is at a very interesting point given that they have shown superb leadership and quality in the feed business (which has become a cash cow) and the smaller contributor for the company (the processing segment) is going to be the growth engine for coming years. Management aims to be a $1 Bln turnover company in coming years. So I thought of sharing thoughts so that we can try to research more:

The Feed business:

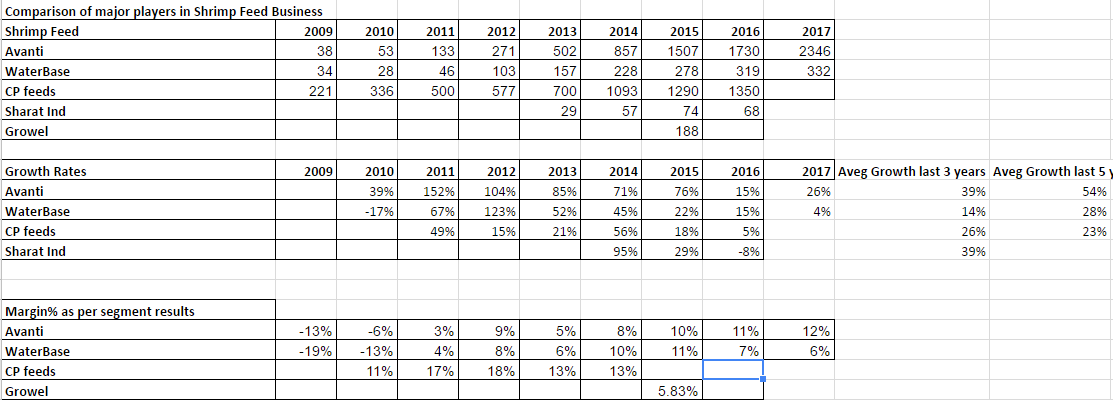

- The company has grown rapidly over last 5-7 years and grown from hardly 7-8% market share to almost 40% now.

- The company has continuously gained market share despite tough times in industry (FY16 saw de-growth in the industry) and FY 17 had heightened competition in the feed business (industry capacity is now also double of the needed quantity)

- This gain in market share has come with improving balance sheet quality. Co has increasing negative working capital vs Waterbase has 90-100 days of debtor days and nil advance from dealer network.

- It seems that company is confident to be able to utilize the new expansion of 1.25 lac tonne done last year in the up-coming season.

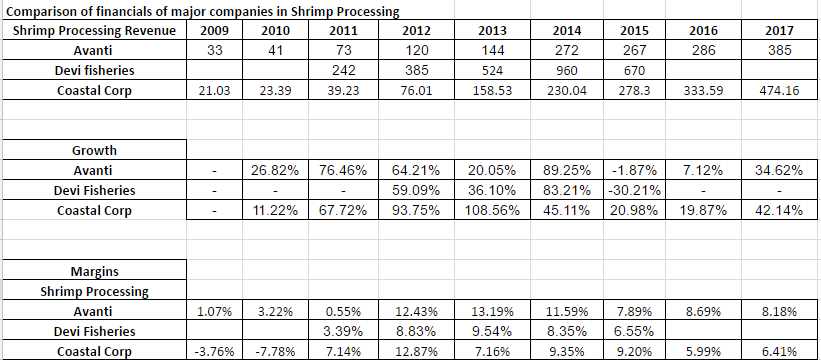

But while discussing with others, I see that general perception is that processing business is not good and it may lead to poor earning quality. I think it may not be so:

- I have numbers of some unlisted processing companies and I see that they usually do 8-9% margins despite being in commodity area. While if we see the interviews of Mr. Indra he seems to be pretty focused on this expansion and emphasis is on value-addition. So i do see a possibility of a bit better margins than peers.

- Even if margins are not higher, I like the idea that this will be the new growth engine for the company. Mr. Indra has mentioned in latest interview that they aim to do 3500 Cr (vs 400 Cr today) from this segment by 2020!! So I like the idea that the feed business has become a cash cow and the surplus cash will be channelized towards say a 15-18% ROCE business rather than earning hardly 7-8% on fixed return instruments.

I think the company has come to a very respectable size and despite the problems in the industry etc, the numbers have been pretty stable. So if the overall business is able to maintain say 20% growth, then Avanti can’t be ignored and may lead to perception change and better valuation from markets.

Key negatives:

- The risks of the industry

- Heightened competition in the industry. Industry hasn’t grown much over last 2 years while everyone has expanded. Hence its important that there should be reasonable growth in the industry.

Views Invited

Regards,

Ayush

Disc: Invested from before