You’re absolutely right about the potential impact of technology on the claim processing industry, especially with advancements in automation. The core idea is that a significant portion of claims—about 85%, as mentioned—are straightforward and can be processed without human intervention. This opens the door for tech-based solutions, like AI and machine learning, to streamline the process.

Key Points of Automation in Claim Processing:

Plain Vanilla Claims: These are routine claims with no complexities, such as standard medical treatments or procedures. Automating these can save time and reduce operational costs for insurers and third-party administrators (TPAs).

Tech Startups in SE Asia:

Smarter Health and DocDoc are good examples of startups working on tools to automate and simplify healthcare claim processing. Their platforms likely use AI algorithms to verify claims against policies, detect potential fraud, and assess risks.

Impact on India:

In India, startups like i3systems are already exploring this space, using AI to process claims faster and more accurately. If this tech proves successful, it could indeed reduce the reliance on TPAs, which traditionally handle the bulk of claims processing.

Reduction in TPA Role: As automation advances, the role of TPAs may shift from handling routine claims to focusing on more complex cases or adding value in areas like customer service, fraud detection, and claim validation where human oversight is necessary.

Automation could revolutionize claim processing, not just speeding it up but also enhancing accuracy and lowering costs for both insurance companies and policyholders. If widely adopted, especially in markets like India, this tech could fundamentally reshape the industry.

As per my understanding,In the United States, health insurance companies typically do not use Third-Party Administrators (TPAs) in the same way as they are used in some other countries like India. However, TPAs do exist in certain contexts within the U.S. healthcare system.

I think Tpa’s role will decline day by day . Here large health companies now use in-house claim settlement process

Even health insurance advisors asks people to chose those companies which does have in-house claim settlement team.

I believe the scenario is different when it comes to group health insurance ie for corporates - thus mediassist has a bigger market share in that segment - though I haven’t done any thorough research on the same but thats what I felt intuitively

Also this article might help understanding a bit of competitive advantage they have

You can please refer to screener or moneycontrol which is showing selling of promoter and same is captured by FII and DII…and this action took place at the CMP of 611.buyers were Goldman Sachs, smallcap world inc,HDFC,ICICI and other mutual funds.

And transaction was done on 3 September.

its most likely a placement to mutual funds and institutions. usually happens when intitutions approach company because market doesnt have enough liquidity. Plus i think the selling promotor is also a PE fund.

Management is very strong about growth! but why are they selling ?

Medimatter Health Management Private Limited, pre ipo holds 27% now it stands at Q2 FY25 4.89%, irony is that medimatter board directors are same dr vikarm and satish, this is big red flag right now!!

whereas, other promoter Bessemer India Capital Holdings II Ltd, also sold in OFS and is selling post ipo, they are PE funds so they need to take exit and this can be taken as pinch of salt.

Major issue is why Chairman and CEO diluting there stake ?

On the contrary side, its like cherry on the cake, all the selling is absorbed by Big and reputable institutions,

conclusion ; major holding is on big hands ,

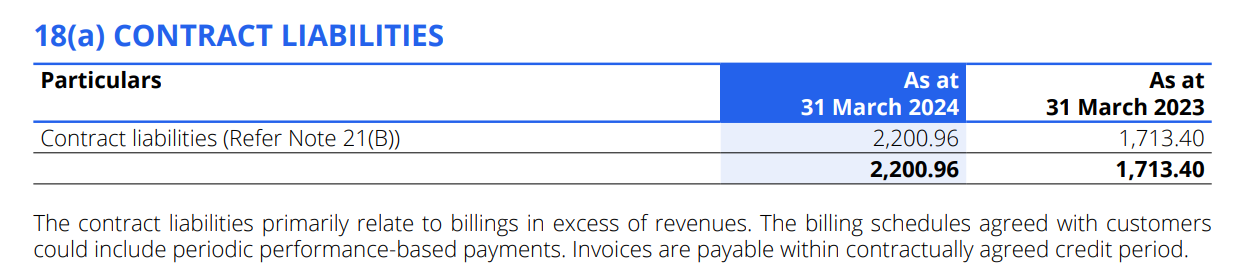

Think like you bought one year Amazon subscription at the end of September. You paid 1000 rupees to it. Validity is 12 months. As per your purchase date, 6 months of your subscription falls in one financial year and other 6 in next financial year. But you paid the entire amount in 1st financial year itself and company has to provide you service in next financial year also. So what amazon do to book 500 rupees as a liability in the 1st financial year balance sheet.

In mediassist case, they received some amount in current financial year, but for that they have to provide services in next year also. So they are showing proportionate amount as liability towards the advance received in current year

Thanks Sidharth.That’s exactly my understanding as well.

I assume higher the contract liability is better as this provides a revenue visiability for the company and it keeps growing in the balance sheet every period. Also, this is shown in current liability, which means within 12 months this is moved to P&L from balance sheet. ( $521 cr. as of Sep’24).

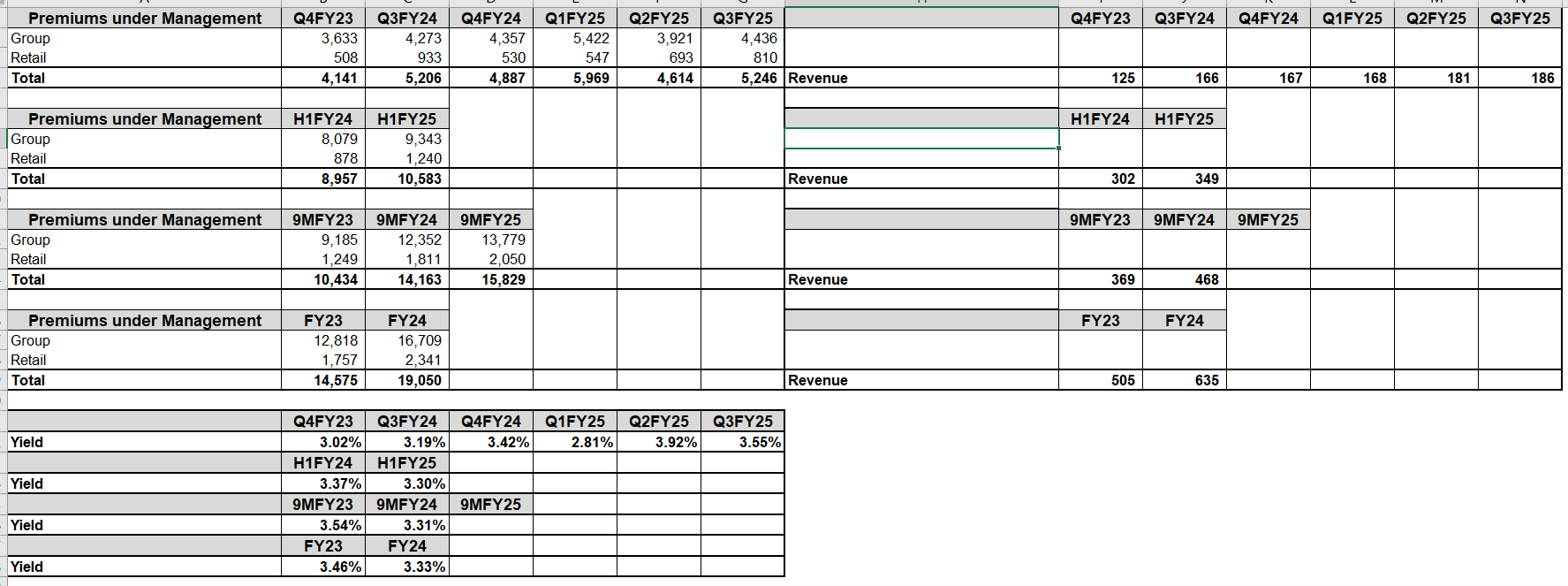

The revenue/PUM growth rates have been slowing down plus the margins have not started expanding as guided by the management in FY24. While the company keeps stating that they are winning market share, this is not translating into strong growth numbers.

While the valuations have become reasonable after the recent drawdown, I am not sure about the key variants for the stock price to move up.

This is the historical trend of their yeilds. What i can understand is that they dont have any further pricing power, even with scale. Can anyone read something else between the lines?