If you look at the above the options turnover has jumped significantly. While the futures have taken a hit because of leverage going away from the markets. Q2 is on track to be better than Q1 (hopefully the company is monitising options trading)

HDFCsec has updated its coverage report on MCX. It aligns with the thesis of further growth in options in Oct’21 and Nov’21. Would be interesting to watch this quarter results if gains from charging options contract makes up for loses from consistent drop in futures volume.

Some other potential triggers (shifting to its own software platform, permission to domestic financial institutions & offshore managers to participate in commodity markets, launch of futures on indices listed etc.) are still way out in future.

Disclaimer: Not invested, tracking for any future potential

Justified , if I see the chart technically, but I firmly believe there is a growth story which is intact there, if we believe in the growth story of India at a macroeconomic level then such commodity derivatives platform will be sustaining a YOY growth

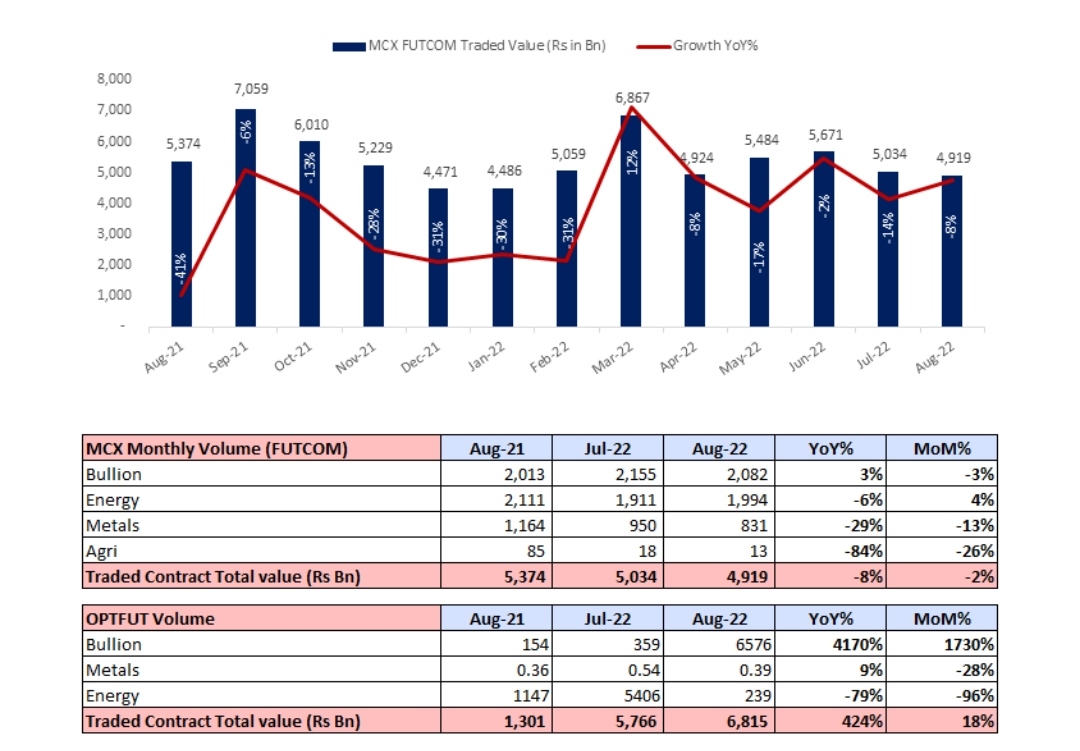

Option Trading is picking up in MCX finally.

In Jan they did a prem turnover of 4.4k crs meaning a revenue of 2.2crs

In Feb they did a prem turnover of 7.7kcrs translating in revenue of 3.7crs

March data is awaited.

From this I can estimate the at the revenue will be higher by 15-18% this qtr over last qtr.

Very useful Vikas - and your revenue estimate is probably conservative if we assume that volatility / prices for key commodities was even higher in Mar (of course I am assuming that the greater the volatility the greater the likely trading - which may not be true).

What is the source of the information above - would be interesting to track.

I got the data from MCX historical data page.

Higher volatility would lead to higher margins which inturn would reduce trading. I heard that the peak margins in Nickel went to 120%, such moves are very bad for the contracts in the long term. That is what happened in Crude a couple of years back and the same hasn’t been able to recover yet. If you look at the ADV its up by around 10% but the commodity prices have gone up more than that meaning the quantity traded has gone down.

Looking at ADT - there seems to be a substantial bump in Futures for 14 days of March (also options continues to remain strong). Drivers seem to be crude oil, silver and gold - if I have interpreted the data appropriately

Company told exchanges that everything regarding the tech transition is shared with investors in concall. There is nothing else to be shared.

IMO mcx management is very transparent. They upload transcripts of analyst meets also. I haven’t seen any company doing that. Sometimes such media reports are speculative in nature.

On the business front Volume of Options is increasing month over month rapidly while Futures volume is constant more or less.

Once the tech transition to TCS is completed which is to be done by q3fy23 the Depreciation will increase but software charge will reduce. Combinely there will be some cost saving on depreciation+software charges But the main part is there won’t be any charges on the revenue which 63 moons is charging as of now. So once the tech transition happens and as revenue increases based on Options volume increase operating leverage will play out.

Mcx result is awesome. revenue at 143 cr pat up 50% qoq. I calculated a revenue of 119 cr this quarter! this is epic!! the price volume of the stock didn’t price it in

small correction: I thought operating revenue will be 119 cr based on monthly data they publish. the operating revenue came to be127 cr. and 18 cr is other income. overall good result. If Options volume explode like this the operating revenue will increase only and we might see some more operating leverage playing out. Unless the other income part doesn’t betray

MCX profit is likely to take big hit for Q3 due to the exorbitant license fee extension for the quarter from 63 moons. Chances are high MCX might post a loss for Q3 on this one time expense.

Anyone has visibility on how is the progress on their new software testing and parallel run? Let us hope they switch to the new software by 1st Jan, else their will be acute short term pain in this counter.

The market is factoring in a 40-50 Cr hit for Q3. Its a known event and in the price. Few brokerages have assumed between 35-40% licese fee increase next Q. in H1 23 Crs was paid to 63 moons.