Wondering if there are any other listed names in this space other than “Max India Ltd” for further study and comparative analysis.

Thanks.

Disc: Not yet invested.

Wondering if there are any other listed names in this space other than “Max India Ltd” for further study and comparative analysis.

Thanks.

Disc: Not yet invested.

Ashiana Housing has been present in senior living housing for more than a decade now, they also launched Care Homes recently.

")

Thanks Harsh for sharing this… You reminded me this Real sector stock which was once highlighted by Prof. Sanjay Bakshi also. This was a forgotten name for me.

Thanks for sharing, will check their Annual reports, ppts, transcript for better understanding on senior care sector.

Any other name, you would like to suggest for reference, please.

Future looks bright for senior care sector in India as the ageing population will increase in the next 10 to 20 years. Below is an extract from Q2 concall;

“And in terms of a long-term aspiration to become a INR 1,000 crores plus top line over the next 5 years, again, these are forward looking statements. Really depend but that’s the aspiration with a healthy PAT of 15-20% in 5 years’ time and a break even perhaps in FY '27/ FY '28. So, we are keeping that vision in front of us all the time and marching towards that.”

Max group with their proven track record in Healthcare, hospitality and real estate sector can create huge wealth for shareholders. At current mcap of ~ 1100cr, there is a huge growth runway to unfold.

Currently they have 300 care home beds, aiming for 600 beds by March 2025 and scaling up to 2000 beds by 2029. Need to watch out the margins vs occupancy rates.

Latest investor ppt: https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=722e7a3d-d99d-470f-80b7-b8e54fdec1f2.pdf

D: Invested from lower levels, Biased.

Future is unpredictable and the care service is a new offering in India. It will take time for numbers to show up. Market might be discounting this factor for now.

Max India Limited’s subsidiary, Antara Senior Living, has partnered with Dr. Lal PathLabs to enhance geriatric care services. The collaboration aims to provide accessible and accurate diagnostic services for seniors, offering specialized packages and ensuring timely results. This strategic alliance reinforces their commitment to improving healthcare services for elderly patients in India.

good news again.Antara Senior Care partners with Wellbeing Nutrition for senior health products.

boAt partners with Antara to enhance senior care technology.

Poor show?

In Q2FY25, They planned to add 130 beds in Antara Care Homes. Now in Q3, they have reduced it to 80. Is there traction in Bangalore for Care Homes? What are the challenges they are facing.

I am not sure if they did any downward revision in Q3. But as per management commentary, they will acheive their target of 600 CH beds operational by March 2025.

During last concall Bangalore CHs were just operational. Q3 concall can throw some clarity around traction in Bangalore CHs.

From Q3 investor slide

Gurugram CH at 18% margins vs 53% occupancy level and breakeven happening at 45% occupancy. I reckon these are above the management expectations.

So CHs might start showing profits in 6 to 8 quarters from their opening if they acheive above occupancy levels.

Anyway it is too early to make any solid estimates. Let us wait and watch how this unfolds.

Regarding rights issue

Planning to raise 219 cr via rights issue in FY 25/26 in tranches. Also they are selling Max towers for ~ 110cr to fund expansion.

I don’t know if it is the right time to dilute equity when Mcap is at just 1000cr. Can’t they wait for some more time and dilute equity at a higher valuation ? If someone has views on this, please comment.

D: Biased as I am invested, I have done transaction in last 30 days.

Q3 investor ppt: https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=6aa8f055-1c0c-4d84-8d80-f57e5067342c.pdf

“Q3 FY25 Earnings concall summary”

“Expected equity dilution mainly at the holding company level to support growth, with possible additional funding at the subsidiary level.”

Having been a Max shareholder since times of original Max India and sold all three subsidiaries at precisely wrong times (Max Healthcare, Max Financial & Max Ventured) - Above is the piece I am most scared of…probably not because of any harm to business but such things would keep testing my patience and question conviction.

Top investors would invest at subsidiary levels while at holding company level, we will face dilution. Also in future any of these maybe demerged, sold, exited or strategic partners…how all that would pan out and how much patience would be tested, which part should I buy more if demerged, which to exit, how long will it take for strategic investors etc etc. Its like same old story might repeat.

Above can be my bias but seing equity dilution at listed company level and possible strategic investment at subsidiary trigerred all this. I maybe wrong and overthinking…

Disc: Invested (currently little over 1% of portfolio) with transactions this week also, hence critical amd biased. Not a buy/sell recommendation. Not eligible for any advice. Post only for learning and I can be wrong in all my assessments.

Thanks for sharing your views.

I was also an investor in the original Max India in 2016 and sold at the wrong time. I never expected that “complicated” demerger would lead to value unlocking and wealth creation. The sum valuations of demerged cos were way more than the original parent company.

This group is well known for these kind of demergers and selling stakes in subsidiaries, but eventually who ever stay put has created wealth. I agree it is bit difficult to stay strong with patience, focus & conviction during these kind of situations.

Management walking the talk and their clarity in communication QoQ basis is something which is helping me to stay put. At least good that they are not IPO ing subsidiaries like how many other cos did (Eg. Biocon/Syngene).

I think they will bring strategic partners in subsidiaries (AGEasy or Assisted care) during next level of fund raise and in the long run may be demerge them once they are mature enough to run as standalone entities. They are expecting AGEasy to hit 500 cr revenue run rate in less than 5 years. And 1000cr revenue on consolidated level by ~2029 with 15-20% margins.

I have sent an email to investor relations team expressing my concern about diluting holding co at an early stage / at lower valuations. I know nothing is going to happen, but just expressed my concern.

If one watch the fund raising activity in senior Care space, lot of big investors and PEs cos are investing heavily since last 2 years. I think all these cos may IPO may be in next 5 to 6 years and this space will become a hot sector, leading to better valuations and early investors reaping good returns.

Disclaimer - Invested and biased. Sharing for learning purpose. Please don’t treat as an investment advice or Buy-Sell recommendation. All my assessments can get wrong.

I have just started researching about this company. There is some discrepancy in data points which I am not able to understand

The company plans to do 1.5mn sqft every year which should translate into 1500cr of pre-sales every year (assuming 10000/sqft), but at the same time company has guided for just 1000cr revenue by FY30.

Also in this 1000cr revenue, ~500cr should be from AG easy and ~100cr should be from carehome.

Also, management has mentioned in the closing remarks of lastest concall that they are planning to have 8-10 communities with 250cr topline with healthy EBITDA margin. Again this 250cr data is not adding up with 1.5mn sqft every year.

Can anyone help me understand on what am I missing?

Max India 125Cr rights issue announced.

https://nsearchives.nseindia.com/corporate/MAXIND_23042025204953_RECORDDATE23042025.pdf

I’m sharing a detailed substack post on Max India

I hope you find it useful.

Invested and Biased

dr.vikas

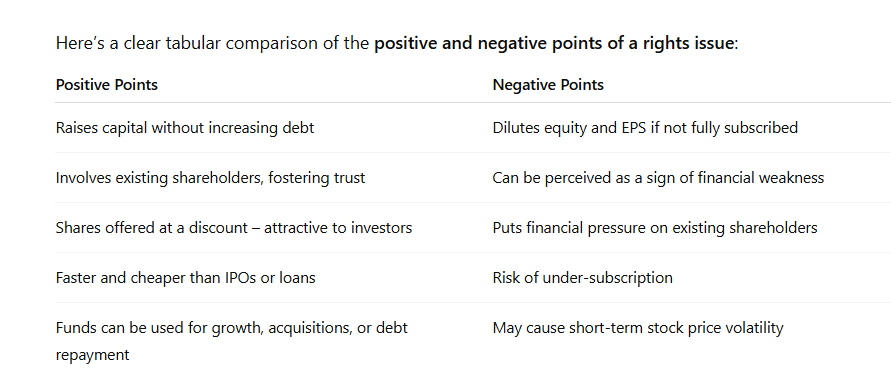

Any opinion regarding rights issues Dr Vikas

I asked it to Chat GTP and here is the answer

Now we have to apply this to Max India and decide for ourselves.

dr.vikas

Technical question as I never Participated in rights issues. My demat account showed price at Rs 23 so today I bought but how to pay difference in amount of price of rights issues vs this rs 23. I revoked my POA long time back.

You have to apply through ASBA facility under your NetBanking during the rights period. If you failed to apply through ASBA those rights shares will expire.