Reference to ConCall, i am requesting the management for a tour of their Care Home & AGEasy Health Studio in NCR.

Please let me know if anyone would like to join ? Would be better, if we can have a group of investors.

6 Likes

I get a feeling that the company is stretched too thin with too many items in parallel. They will need to fight competition in every aspect. Their only uniqueness seem to be that they are the only listed player who is doing all of these together in an integrated way.

The reviews of Antara are quite good. I would normally the company focusses more on Antara and scale it out. But, I might be wrong as the market opportunity could be in an integrated approach.

Disc: Tracking

4 Likes

Antara has senior living and care homes if I am not wrong. By Antara, which part of business you meant?

By Too many items, you are referring to which all businesses? Why I ask this is because of various things that happened with this group last few years, it is not clear to many what the listed Max India holds…so would be good if you elaborate more here…

I was referring to the first three items which seem to be the core of the business. MedCare and Phygital platform seem to be distractions.

Having 5 different lines of business is what I consider as too many, considering where the company is currently. It would spread out management bandwidth considerably.

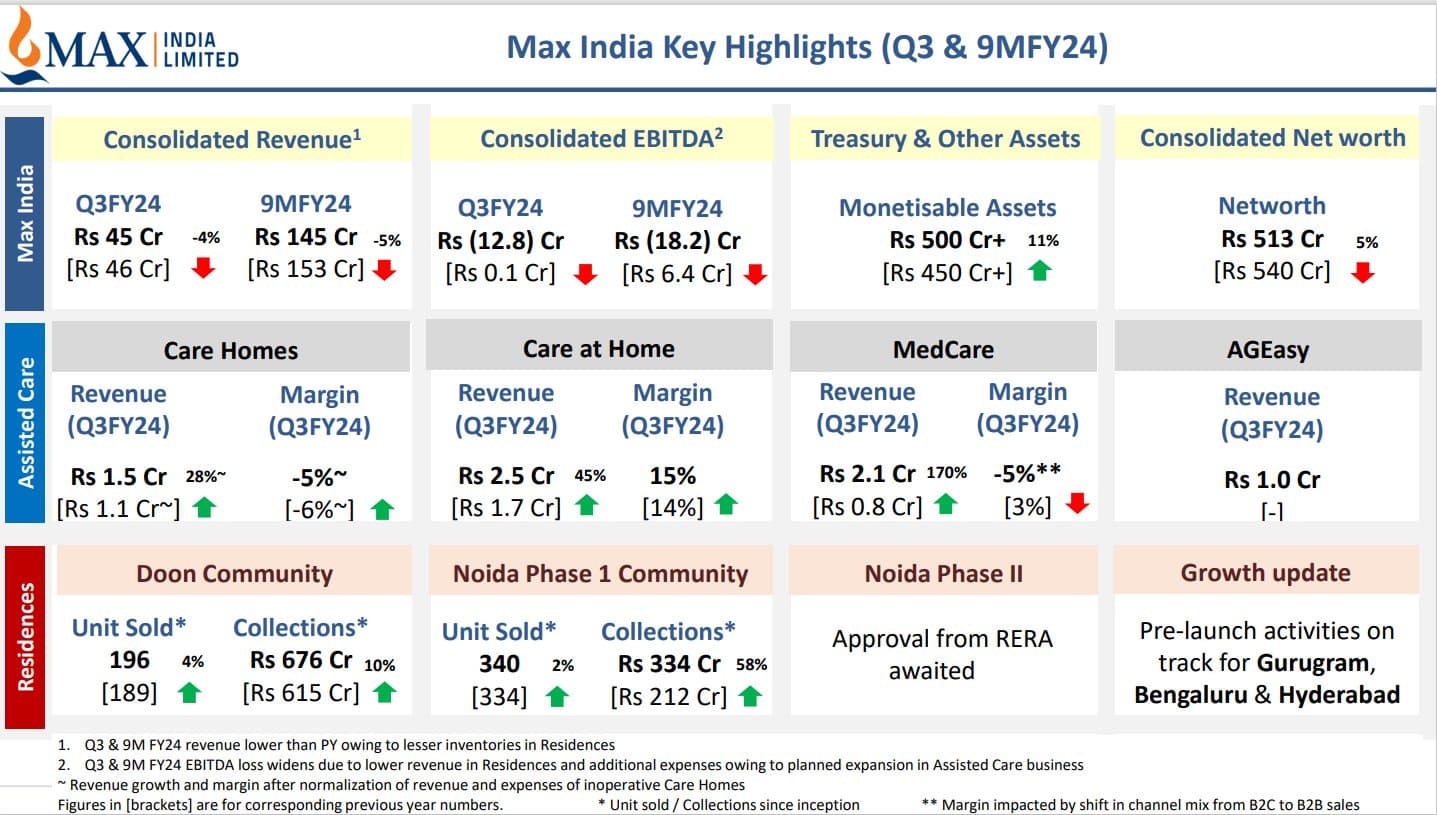

Rgd. MaxIndia’s business verticals, you can refer to the snippet from presentation:

1 Like

I agree with your thesis. However, remember that Max India has a proven track record in many areas. Doing it before gives them a higher probability of success since the learnings are already noted, and failures won’t be a negative surprise but a probabilistic bet.

-

Residence - this is new for the management. Dehradun took many years to sell. If I am not mistaken, it started in 2013 and sold out in 2021. They learned many things which they have mentioned during the council. End-result is a unique project where the resale value is almost 2x the original price.

-

Care home - they have experience in healthcare and hospitality. Replicating while keeping in mind the specifics is the key which they are aware of.

-

Care at Home - same as 2. My view is that this will not make much money bc. of the competition and non-sticky nature of the game - but is rather for the captive audience for 1 and 2.

-

Medcare - very appealing for the audience in 1 and 2. They are partnering and white-labelling, not many ways to go wrong here.

-

AGEasy - this won’t make money. just a distribution channel to sell 2,3,4

3 Likes

Customer service and design seem to be poor.

1 Like

I have come across this co recently and i was trying to decipher the projections they have made in their annual reports because of the multiple verticals that the co is into. Can anyone explain how much revenue the company is planning to achieve?

1 Like

But this is Max India forum, not healthcare.

1 Like

My apologies, but the Title is the old one when Max Healthcare was in the fold.

I did request the moderator in the last line, if this was not noticed. Refer to my older post on Max healthcare, reason why i end up here of that company. Max India - Demerger, Will sum of parts be greater than single entity - #94 by ashwind

Below average numbers as expected. They did not have much in inventory to sell the residences. Other business such as Care Homes and Care at homes are still small to make any impact in the overall performance.

Quarterly result link:

2 Likes

Hi @ashwind , If possible, could you please make a separate thread for max healthcare. Looking forward to it.

Anyone attended the con call today? If yes, please share the main points.

This is Max India forum, not the Max healthcare.

2 Likes