I recently wrote a blog post on very long term passive investments. I’d love to get your feedback on how I have done the research and what improvements I can make. If you want anything specific tested with the data I have, please let me know. I will try my best to do it.

I have only recently joined this community to bring a greater focus to my investments, despite being an investor for more than 20 years. I found your article very informative (a bit heavy on the maths for me personally - albeit necessarily!! ) I must confess that my own strategy has been absolutely the same: buy and forget. This has given me very good returns, and over long period, exactly as highlighted in your article.

I just wanted to ask as to the rationale for arbitrary weightage, and the criteria for selection of the weightage numbers. I found this part a bit difficult to understand and would be grateful for clarification.

The arbitrary weights is just to give more importance to the results given by that measure which has the lowest Skewness (P/E). 50-30-20 split is the rule of thumb. But I doubt the results will change at all even if you use something like 70-20-10 or anything else. The basic requirement is w(P/E) > w(P/B) > w(D/Y).

When we quote the celebrities saying that the markets cannot be timed, an authority bias kicks in. They mean something else, but we understand something entirely different.

They mean that one cannot consistently and correctly predict the markets. As in, no one can say for sure what level nifty is going to be on a particular date in the future making the markets unpredictable. They mean that, one cannot extract short term gain, by playing the markets like a casino.

However, we understand this advise wrongly. We interpret it as, we should keep investing at all levels… Pe 27 or 17, and it won’t matter… Because Peter Lynch says so.

This is completely wrong. He would never say that. These are long term value investors, Peter Lynch, WB etc. They buy when price is cheap, value is more. And get the hell out when this equation reverses.

Another bias I would like to bring to the fore front. It is adviced to invest for ten years. But I simply don’t see the practicalities of that statement.

Assuming that we are talking about only the companies that have it in them to maintain good fundamentals for a stretch of a decade. That brings us to only 5% of all the listed companies.

Even they, in fact especially only they, get exceedingly expensive to the point that there is no sense in staying invested.

For example… Since 2008 Infosys has given very dull returns. Going forward Maruti is likely to be a dud.

A portfolio has to be dynamic, but only as much as is necessary. It cannot be a legacy.

The data you have analysed suggests that one could buy an Index fund and remain invested in it for a longer stretch and it would be fine. Even then, one must react to the PE levels. Because a ten year stretch has two five year periods. If one only reacted to expensive and cheap PE levels good returns would be much better than simply holding.

Thanks for the clarification. Like I said, Maths is not my forte, but I think I have understood it intuitively. Which basically means that I believe that I have understood, but please do not ask me to explain!!! :)

Dinesh, can you do a similar exercise on BSE500 or NSE500 companies. It would actually show to a large extent brutal fall and recovery compared to Nifty index. thanks

@jamit05 No, Amit. Warren Buffet clearly says “You’d be making a terrible mistake if you stay out of a game you think is going to be very good over time because you think you can pick a better time to enter.”

Take the current NIFTY levels for example. What should the investors do? Stay out? What if Earnings recover more than expected in the next quarter? Then should the investors jump back in? There is your problem, you see. That’s what I meant when I said ‘you can’t time the market’. Nobody can. You are correct about selling a stock when it is overvalued (Based on some kind of intrinsic value calculation), but if you’re going to determine overvaluation or undervaluation based on P/E levels, that doesn’t make sense to me.

Regarding your second point, I specifically mentioned 10+ years. I was able to calculate 10-year returns only because the data for NIFTY 50 TRI was available only for 17 years. I could have calculated 10+ years’ returns, but the amount of data points that would generate will be very less for any kind of further research.

Edit: Forgot to add this. The blog post is actually about passive investments (Index fund or similar blue chip mutual fund investments). I have updated the headline.

I will consider it. I am hesitant because I doubt any index would be far different from a broad market index. There might be some deviations, but since we’re only looking at the big picture, I think it’ll stay the same. Let me try to download those data and regress it with the NIFTY 50 data I have. If the correlation is high, it would make no sense to research it again.

WB is an investor in individual stocks. He uses the words “game” and “Mr.Market” for his investments in those stocks… he is not talking about Nifty or any other Index.

Indices behave very differently than Individual stocks in many important ways.

We are talking about investing in the Index when we are discussing the PE levels and when extrapolating an investment strategy from the following table.

In spite, of knowing that in the past nifty has given negative returns in the year after going above PE 23, and still we want to remain invested due to the Authority Bias (thinking WB says so) then it will be a serious folly.

My point, is why worry about short term returns when the long term returns in PV terms are almost identical regardless of P/E levels (Worst case scenario, long term returns are 2% lesser for higher P/Es)? The convergence to mean would ideally be even stronger for even longer term returns. I wish I could research longer term returns (Ex: 25+ years) and I am positive then I could prove that returns in PV terms actually converge to the mean regardless of P/E, P/B or D/Y levels.

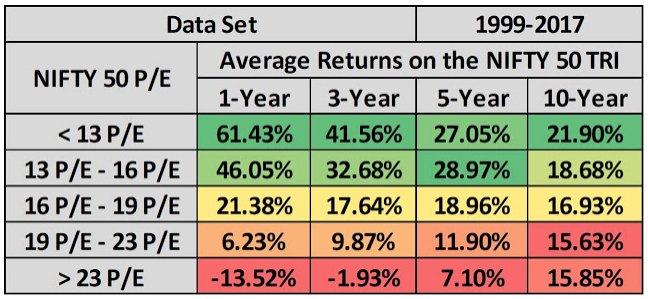

Meawhile, I think you are mistaken about this picture:

These are not absolute returns. These are reported on a CAGR basis. I specifically mention this in the blog post. All I’m trying to say is, if (1.219)^10/(1.07294)^10 > 1.6143/1.07294, then why bother looking at short term returns at all? (Here, 7.294% is the Risk-free Rate in India and I am using it to account for time value of money).

A very good read for case for long term investment.

But what if you bought AMEX the day before the scandal came to light? You would’ve thought you were a dummy. But your investment returns over time would’ve been close to Buffett’s. So close, “it’s not worth arguing about,” Gayner said. “You would’ve compounded your capital at high double-digit rates.”

Again, I would like to ask you to look at it from a more realistic point of view.

We are bound to strategize because there is a significant advantage we can extract.

Consider this.

We know that 10 yr return is 15.85 but 3 yr return is negative. This is because after reaching PE 23, market corrects in the short term, giving us a buying opportunity.

Point being, I don’t suggest that we start predicting. But, only start reacting. When PE goes above 23 we simply stop investing, and wait for the correction. Which will surely come because we are dealing with an Index and not a stock.

An index has a very low EPS growth, as compared to a stock. Therefore, for a stock a PE of 23 becomes PE of 16 without a correction in price, because EPS may increase quickly due to various efficiencies of the underlying business. But not for an Index.

To normalize a PE of 26, an Index EPS cannot do it alone. EPS may show growth, but it is usually sluggish. As a result the price also must correct hence taking PE of 23 to 16.

This is what has happened all the time in the past.

Think about it this way. The money that you would use to invest at PE > 23, you are simply keeping it in FD and using all of it to invest at PE < 20; Your buying power at lower prices will drastically increase.

PS: Of course these are CAGR returns. Doesn’t make any investment sense to make a total 15.85% in ten years.

“I have never known anyone who could consistently time the market. In fact, I have never known someone who knows anyone who was able to consistently time the market.” - Burton Malkiel.

“I can’t recall ever once having seen the name of a market timer on Forbes’ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions doing it.” - Peter Lynch.

Have taken both these quotes from your article. I feel they are misplaced.

Both the authors are saying that short term trading (day trading, BTST etc) do not work over a large set of trades.

However, they support the idea of value investing. Buying when stocks are cheap, and holding till they are good expensive enough to be sold.

Actually we don’t buy index we buy stocks… those companies that were leader of last bull run have either not recovered till now (real estate companies) or performance returns has been negligible computed from peak of last bull run.

I think one should safeguard his portfolio and not rest in disguise of long term index returns.

If you buy many companies and try to mimic the index, weed out underperformers every now and then and add new stocks/ buy more of the performers, you will in all honestly beat many fund managers haha! Heavy weights in strong performing cos and youre set haha!

) I must confess that my own strategy has been absolutely the same: buy and forget. This has given me very good returns, and over long period, exactly as highlighted in your article.

) I must confess that my own strategy has been absolutely the same: buy and forget. This has given me very good returns, and over long period, exactly as highlighted in your article.