Maruti is the only car company in India to have lithium batteries added to existing ICE cars. The cost of the lithium battery is absorbed partially by Maruti. They already invested in battery production along with Denso and Toshiba. Suzuki has failed in USA and China. Japan is shrinking. For Suzuki, India is the only viable booming market. In my opinion, they will be the leader in EV for segments below 10 lakhs. Only time will tell but the steps taken are brilliant.

The lithium batteries are currently imported and added to limited cars in the Maruti stable. Once production starts in India, the cost will reduce from 50k a battery to less than 25k with a run size of 1 lakh cars a month.

Just an observation: since a year suddenly EV has become a massive threat for Maruti. When the price was 10k last year, not a single person spoke about the EV threat. Somehow people feel the need to (rightly or wrongly) justify each stock price fall. In my own opinion, It will be so so long before EVs make any difference to the landscape of india auto industry. No matter how low a battery price, I don’t see any way that an EV will be produced in rs 3 lakhs within the next 5-7 years atleast by when this slowdown would probably be over and Maruti would be back in its path of growth, which is finally when people will once again stop talking about EVs

There are reports by both investors and analysts that there is an auto slowdown. However let’s look at real numbers. In statistics, we always ignore the outliers. 2018 was an outlier. The sales volume grew over 50% last year on certain months and that was abnormal growth. We have never had such growth in the past. It makes sense to look at annual numbers or values over a decade instead of monthly numbers. Just because auto companies report monthly numbers, we don’t need to be shortsighted.

Let’s look at how we grew. 2011 sales was 992k. By 2016, we were at 1390k. That is a a cagr of less than 7%. Let’s extrapolate 7% growth between 2017 and 2019. At 7% growth, we must have a sales of 1591k by 2018 and 1702k by 2019.

By 2018 we were at 1725 (vs expected 1591). 2019 half year sales is at 783k. The festival months are yet to come and we may reach the target of 1702k. Even if we don’t reach it, we may marginally miss the target. We have seen 0% growth between 2012 and 2013. This annual growth of 0% is not new.

I agree with most of what u have said. First half of last year was really exceptional.

The 7 pc annualized CAGR comparison that u have done makes sense…at least for the natural bulls ( i m one ).

But, just to get an even better perspective, can u throw some light on their 10 year volumes CAGR form say 2008-18. Their sales CAGR over this period has been around 16 pc. Just to get a better grip on the situation, wanted to know of their volumes CAGR.

Year ending Mar 08 sales volume for MSIL were - 7.64 lakh cars and CVs ( domestic + exports )

Year ending Mar 19 sales volume for MSIL were- 18.62 lakh cars and CVs ( domestic + exports )

That is aprox 9 pc cagr volumes increase in last 11 yrs.

Last 11 yrs profit growth has been aprox 14 pc…up from 1731 cr in Mar 08 to 7502 cr in Mar 19.

First qtr and the begining of the second qtr this yr have been bad. Hoping for a recovery in the third and fourth qtr. Plus the high base effect of last year would also be out of the way in the 3rd and 4th qtr.

Lets see how it goes.

Hoping for the best.

Fingers crossed.

I am not saying Maruti will grow at 7% in the future. All I wanted to say is about the evaluation criteria of month to month sales. The monthly data and even annual data is highly variable with lots of ups and downs. In fact the sales volume alone is not a great metric as the type of car sold and the variant will determine the earnings. A lose talk on auto slowdown is not warranted unless the pattern is observed for few years.

Disclosure:

I hold MSIL in core portfolio for a long time and don’t plan to sell unless there is a slowdown for Maruti (instead of industry) due to issues within Maruti.

It is not a cake walk …lot more safety features need to be brought in… don’t think EV to replace conventional car if people are not finding it reliable…

Not aware of this specific case involving Kona, hence no comments on this specific case.

But in general whenever a new model is launched by any manufacturer, there are several media reports of vehicle catching fire, bad accident images, etc. A simple google search will show you many images for many newly launched models across various time horizons. Not sure if such incidences catch fancy of media only because the model is new or these are the stories planted by competing rivals to bring bad name to newly launched model.

Electric vehicles are here to stay and with passage of time, technology will only improve and become cheaper. Maruti itself is making significant investments in electric vehicle technology and I think will emerge victorious even in electric game.

I was discussing ubereconomics with an investor. I thought it may be good to share it here in VP. The Uber revolution has changed the taxi cost system. In the past , taxi fare was shared between 1) Fuel 2) Driver 3) cab / fleet owner. When Uber entered the indian market, they did not modify this structure and took 0% share. However after sometime , they took the 4th slice. So we have 4 slices now.

This means, in a country like India, where we can never have autonomous cars for 2 decades, we cannot eliminate the driver. Wealth distribution in India has ensured the need for a fleet operator if Uber needs to scale.

This means cars as a service can never become cheaper than owning a car. Already quality of cars are so good that we spend very less for maintenance. With EV, this may reduce further.

Bottom line imo we may never see Uber taking over Indian roads, except for certain cities where traffic makes it so miserable that we can ignore cost metrics.

To be Maruti specific, an interesting development on small cars:

US auto companies never felt the need for developing small cars. From next year EU will phase out small cars from mass market due to falling margins. This leaves Japanese and Korean auto companies apart from home grown Indian companies to fight for the mass market small cars. As long as 4m rule is present in India, Maruti may have the upper hand, be it electric or hydrogen or ICE.

I think you must include depreciation, interest costs, maintenance (which is no way cheap, if your annual mileage is low), insurance, parking costs, capacity utilization as well into the equation and you will notice what the brain intuitively notices.

Car as a service is certainly not for me (I own two) but I can certainly see why it is appealing for a lot of my friends.

They certainly can do with a 2 wheeler. We can just take the current population of car owners who do 10k+ km a year.

When I talk about cost, it includes everything from service to even opportunity cost.

If you use the 4 part rule as stated above, a 10k km ride with a price of RS 12/km would be a total of 1.2 lakhs. This will give a potential savings of 60k a year (savings from Uber and driver expense) which must be the cost of individual ownership. The 60k is after all expenses (includes feet operator cost and fuel) that both a cab and personal car would incur. You may add special expenses like opportunity cost, etc.

Most people will break even before 10k km. Personally my break even was at 4k km. However it may differ based on aspirations and cost of car.

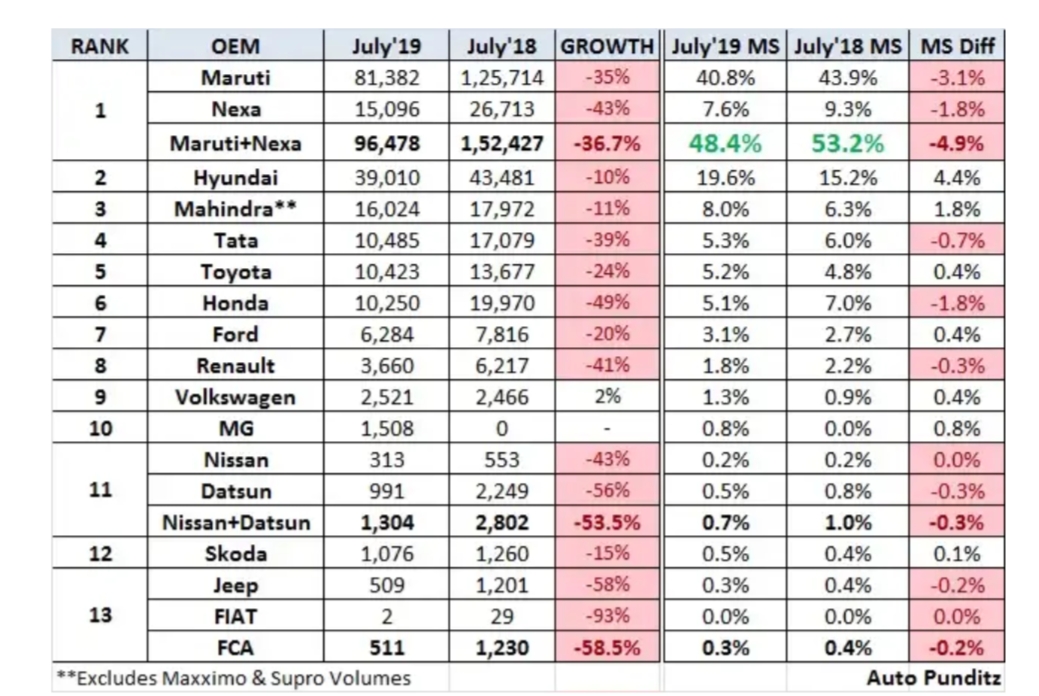

The biggest risk for Maruti may actually be due to competition getting better and reliable. As Indians climb up the value chain, Hyundai may be able to satisfy customers due to their bigger R&D budget and portfolio of premium products. One may need to monitor the market share of Hyundai and see if they are able to capture the C segment from Maruti/Nexa.

In the last decade, Hyundai has kept the 15 to 18% market share and has been consistent in defending it.

July 2019 sales shows 4% market share shifted from Maruti to Hyundai. New launches has helped Hyundai.

I guess the thesis was always around drastic improvement in asset efficiency. Uber added a 4th slice, but they have the potential to reduce the idle time of cabs. If each cab does many more trips per day than it used to, then the per-trip cost of depreciation comes down significantly. That is also the reason Uber could cost you less than owning a car. Uber just turns that asset over so much that it more than covers all the other slices!

Currently that may not be the case. But I would not argue that it could never be the case.

I was a big fan of Uber in it’s early days and almost junked my own car. However I am back to using personal car. Most Uber drivers are now becoming similar to old yellow / black taxi drivers… they refuse destination regularly, car quality is going down (experience it when you get allotted an Indica in Pune), and some of the drivers have pathetic attitude. Once I was dropped mid way while going from Bangalore airport to Whitefield by a driver for a simple reason that traffic was very high due to rains and he was fed up after driving long hours. At 10 PM, under heavy rains, I had to wait for 1 hour to get another ride and reach home.

By the way, fares are not cheap anymore specially for short distances. Yes, not finding parking is a big convenience when we use Uber but overall own car has it’s own merit and can’t be scrapped completely.

As I said earlier, I am comparing users who fall under the sweet spot in usage pattern. If someone does 10k km per year or more, their maintenance expense falls under the Goldilocks range. When a cab driver does more rides, he is increasing usage and helps in reducing depreciation cost (accelerated depreciation) of car. The maintenance expense does not differ much between personal use vs cab when inside the Goldilocks range. When calculating the savings, I took away 2 slices (Uber and driver expense) but never removed the fleet owner expense (which is the same as personal car user). A fleet owner may depreciate his car in 4 years while a personal car might depreciate over 10 years or more. The lifetime of car is fixed and a personal user may have to hold on to it for a longer time while a cab has to be replaced early. As I said, this leaves us with opportunity cost difference between a 4 year depreciation (of a fleet owner) vs 10 year depreciation of personal car. For a person who falls in the Goldilocks range, Uber will always be expensive.

Slowdown notwithstanding, Maruti Suzuki to go ahead with doubling of capacity at Gujarat

Maruti has plants in Manesar and Gurgaon also with combined capacity of 1.5 million units a year

This comes as a reassurance from the company that they know what is going on and the current slow-down is cyclical in nature.

We may need to take any word from management with a pinch of salt. They are known to make statements which may not turn out to be true. We saw that with the diesel announcement earlier this year. However they may consider it to be strategic to keep the competition guessing by releasing confusing statements.

The capacity utilisation is about 75% in India. So who knows if Maruti increases its capacity the utilisation will come down. Anyway I will never trust overly optimistic managements. I still remember AM Naik coming on TV sometime in late 2000s and saying they will grow 25-35% for a long time because India’s infrastructure is still primitive. We know it turned out to be wrong by a distance.

Just put head down and work, increase sales, increase productivity and profitability.

Toyota has give their Hybrid patents for free to all OEMs. My guess is that Suzuki probably might soon be running Toyota India as they would have expected more than the freebies to give away Baleno. We might see new launches from Toyota to be rebranded Suzuki. This can help increase utilization. Thereby increase bottom line.