Maruti Suzuki is poised to breakout of a mammoth 139 day triangle with a potential move of 1200 to 1300 points (which is the length of the base of this triangle)

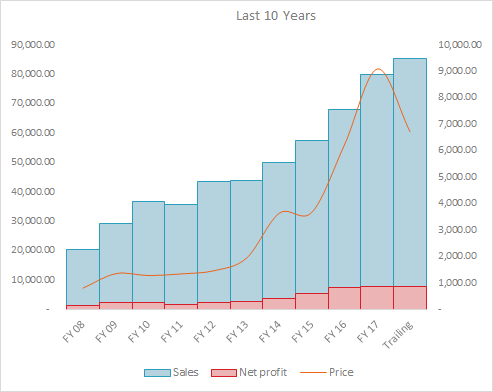

At a standalone level its TTM PE is ~28 . A 1200 point breakout upward would mean a PE re-rating to ~32 (at a standalone level ) and a break downward would mean a PE re-rating of ~23-24. I think given its balance sheet position Mr Market will re-rate it at ~32, this means an upside of about 20% from current levels in (hopefully) the next 139 days or 5 to 6 months. With an ROCE of 33% to 34%, exceptional OP margins of ~15%-16% & a great capital turnover ratios - Maruti has outstanding & numero uno numbers in the auto industry. The bull market we are in is in the mood of celebrating numbers this summer.

Disclosure - am accumulating with a short term view of ~ 6 months.

Please note - this is not based on any tested theory. This kind of analysis is speculative and hypothetical and unless convinced avoid it.

The triangle as drawn is not the bullish variety. At this stage of the movement it looks more like a rising wedge- which is actually a bearish pattern.

However, the conditions present and the attendant sentiment is not one of a rising wedge either. So one cannot take it as such a pattern despite the appearance of one.

Ergo, avoid the conclusion of a triangle and its implication.

ckn

Thanks for the inputs ckn. Much appreciated. Since i have taken a position will wait for it to play out. At worst it is a channel and prices will react off the upper trendline. I am still learning and perhaps experienced traders like yourself can guide us beginners!

I may be getting ahead of myself here but prices have reacted off the lower trendline and seem to be heading up. From an educational perspective this is shaping up to be a great case study on how prices behave in a triangle setup.

on a different note - there is no better example of a long term trendline than maruti. look at that trendline - it should be framed and kept in a museum. Its a 13 year masterpiece. Serious gravitational pull.

Some important lessons

You could have joined the party ANYTIME and still made money. Good businesses take good care of their shareholders regardless of the price.

The area just under the trend line is where the traders are active. Large deviations under are where the value investors are active. Needless to mention its the value investors who make the most money. Swimming in the shallows is no fun. The deep end of the ocean is where the gigantic creatures dwell!

Maruti has more than exceeded the 1300 projected move and still going strong. It also seems to be following an upsloping curved trendline which from what i have read is typical for stocks which are heading for a climax top.

GM’s India exit, and the possibility of other players exiting, would mean that more customers could stick to a solid incumbent like Maruti, allowing the company to improve its grip on a growing market.

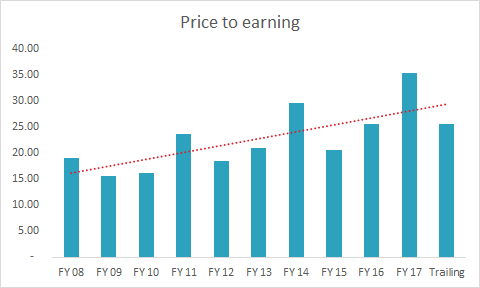

A quick check on the valuations of global auto companies reveals that Maruti is the most expensive auto stock in the world, at least among the top 30 companies by market capitalisation.

I don’t see a post on Maruti under investments. However I think this is a great company to explore. The NPM surge has been significant in the last few years. The capacity is still lagging demand and true potential of MSIL can be seen only when they are free to sell all variants with differential margins. For example, they stopped selling hatch back diesel (Ritz) to cabbies due to production constraints. They have to focus on higher margins and ignore selling lower margin cars.

A close look at their market share growth and sustinance would be very helpful. What is more interesting is the pipeline of competition. Barring a few models from Hyundai and Tata, Maruti continues to have a free hand. At current valuation, one can look at estimating EPS when capacity > demand.

Disclosure: Invested for a long time and views may be biased.

Overall market share would be more than 50%. And market share in entry level segment would be approximately 70%. The strength of entry level segment is huge itself.

Parent holding is 56.21% only. Probable buyback candidate.

They are again expanding in Gujarat. If market reports are to be believed, Gurgaon plant is valued at 12000 crores. A possible sell in next 3-5 years.

Negligible debt of below 500 crores. Reserves stood at 37000 crores. Quoted investments worth 27000 crores.

There was a change in choice in entry level segment few years back. Due to lack of service availability, resale value etc they are shifting to Maruti once again.

It would be interesting to know how entry of China’s SAIC - MG motors (English) affect the market share of Maruti Suzuki in the long term.

Based on the article they would be entering with the SUV segment.

"I can tell you that we would be in the forefront of greener solutions in India… we are doing that homework very seriously,” Chaba said.

Disc.: Tracking from 4000 Level, bought at 5800 and then added again at 7800 levels.

Did some profit booking to avail tax free LTCG.

There are a host of negative views on Maruti and the auto sector . But practically it is clear that neither EV nor Uber can force people to shift completely. I find this exciting time to buy at current valuation. The growth in revenue and bottomline will be there if we consider a 5 year timeline imho.

Disclosure: Adding heavily at current price and already own 30% of portfolio in MSIL

Long term chart is solid. YOY quarterly is flat to decreasing. PE is less than historical average. PEG of 1.03 is also fine. Considering good ROCE , No debt, Market leader and fairly OK with new product launches, Maruti looks like a good value buy at current level. However headwinds like USD, Insurance price increase, fuel price etc essentially putting margin pressure has to moderate for numbers to improve, so will stock price.

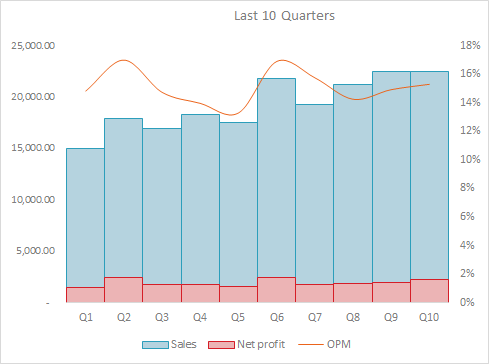

The November sales number were out and Maruti has had respectable sales. From a 48.3% market share in Oct it has grown to 54.6% in Nov. No manufacturer in the top 10 from Oct to Nov grew their sales number other than Maruti at 5.8%. Overall PV sales dropped for the industry by 6.2%.

Apart from this YoY the PV sales dipped by 3.1% but for Maruti the dip was 0.3%. Oct+Nov sales in 2018 have been the maximum since 2016 (though only marginally higher in 2018 over 2017).

Lets see how MSIL tackles the significant evolution coming our way.

The article in livemint talks about Suzuki directly manufacturing cars without going through Maruti Suzuki. Also it talks about Suzuki paying only cost price for cars sourced by Suzuki from Maruti Suzuki. All this seems to be cannibalizing from Maruti Suzuki and depriving what is due to Maruti Suzuki shareholders. The return on equity of Maruti is not so good due to a lot of funds lying as investment, which the management is complacent about utilisation. How can they utilise this investment, when they want to develop Suzuki, having withdrawn from US and Chinese markets. How long can they hold their 50% share? What about competition? All this makes me circumspect and hinder me from being an investor in this otherwise fabulous company.

Don’t find Suzuki minority share holder friendly. From high royalty, importing key components from Suzuki Japan, direct Suzuki investment in manufacturing of cars, Suzuki investment in EV. Steps look like depriving Maruti of future profits.