MSIL has given volume growth guidance of 4-8% for FY20 in their concall for Q4 FY19 concall . With these growth for petrol and diesel total growth rate comes out to be 5.3%. (Remember that in FY19, industry grew by 2.7% & MSIL ~6%)

The calculation is done to show the upper cap, even at FY20 PE of 24 with all these sales the stock’s current price is expensive

So 6500-7500 is the most optimistic price range for MSIL for FY20 is what you can say

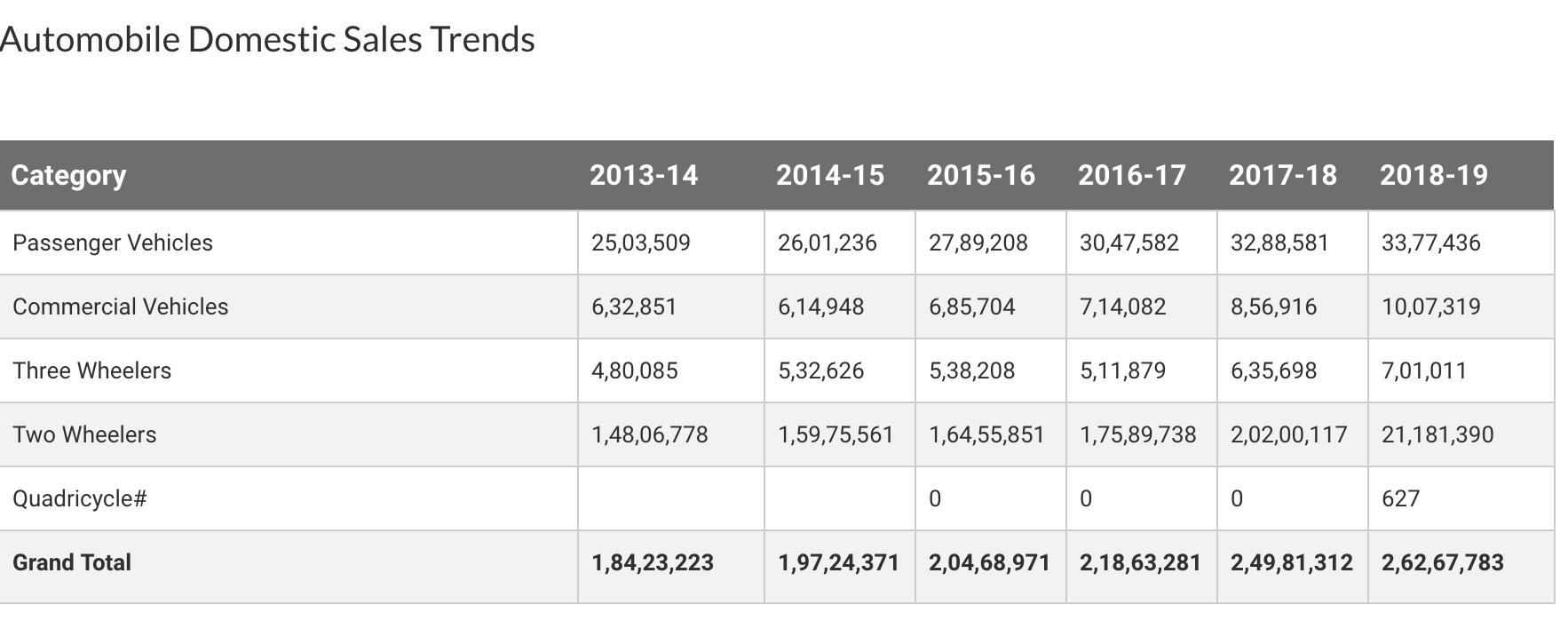

This is from SIAM website. So in the past 6 years total passenger vehicles sold is around 1.76 crores and total 2 wheelers sold is around 10.62 crores. Assuming around 25 crores household in india and those who will have income to afford cars in india will probably we around 5 crore (or throw some other figure) I think lot of household have a car. With pathetic condition of roads, accidents, parking, urban mobility … growth in AUTO may be slow and unlike witnessed in earlier decade.

One needs to look at the first car buyer %. It is currently at 53% and rising. When it declines below 20%, we may have to see lower growth rates. One also needs to understand that a car is a luxury item in India and hence it will be a slow and steady growth if we ignore seasonality and cyclical nature of it. We have seen a growth of around 3% cagr in the last decade and that seems to be possible for next decade too.

[ OPINION ] What could be the impact of MG-Hector on current market leaders?

Even before its formal entry into the market, The MG Hector (rebadged Baojun 530) by SAIC Motors has already heated-up the LMV/SUV space with its jaw-dropping specifications. The MG Hector has already drawn enough attention in the Indian market through its features and claims of being India’s first internet-connected car.

Doesn’t matter, whether you like Chinese brands or not - you definitely can’t ignore this feature loaded car in 12L-15L segment.

If you remember, few years ago, Micromax was growing exponentially. Its Gurugram office was said to be at par with the likes of Google. With the arrival of Chinese mobile companies in the Indian market, Micromax is now operating out of a single floor in a common office complex in Gurugram. Home-grown smartphone brands such as Micromax, Lava, and Intex once cornered nearly 54% of the market share. The same brands have a less than 10% market share today. (source: livemint)

The ‘Baojun 530’ is a product of SAIC-GM-Wuling joint venture.

It was introduced in Colombia and Thailand as the second generation Chevrolet Captiva in November 2018.

It has already been launched in Indonesia on 27 Feb 2019; being marketed under the Wuling brand with the name Almaz (means ‘Diamond’ in Arabic).

Now, it has been introduced in the Indian market by SAIC motors as MG Hector.

Though it is hard to calculate its true impact on current market leaders at this stage. It definitely seems to have potential of eating-up market share of existing companies.

June car sales shrink by double digits for the third month in a row; commercial vehicles skid too; numbers may raise pressure on Centre to loosen purse strings in Budget to spur lending & growth

: Passenger car sales shrank by double digits for the third straight month in June as buyers continued to be put off by higher interest costs following the nonbank lending crisis and by rising automobile prices.

The end of election uncertainty in May did not revive Motown’s spirits and the numbers could increase pressure on the Narendra Modi-led NDA government to open the purse strings in this week’s budget to spur lending and growth. Finance minister Nirmala Sitharaman will present her first budget and the Modi government’s seventh on Friday amid a sharp consumption slowdown.

The motor industry estimates that passenger vehicle sales fell by about 19% to 222,000 units in June, the third straight month of double-digit declines. Vehicle sales had fallen 17% in April and 20.5% in May.

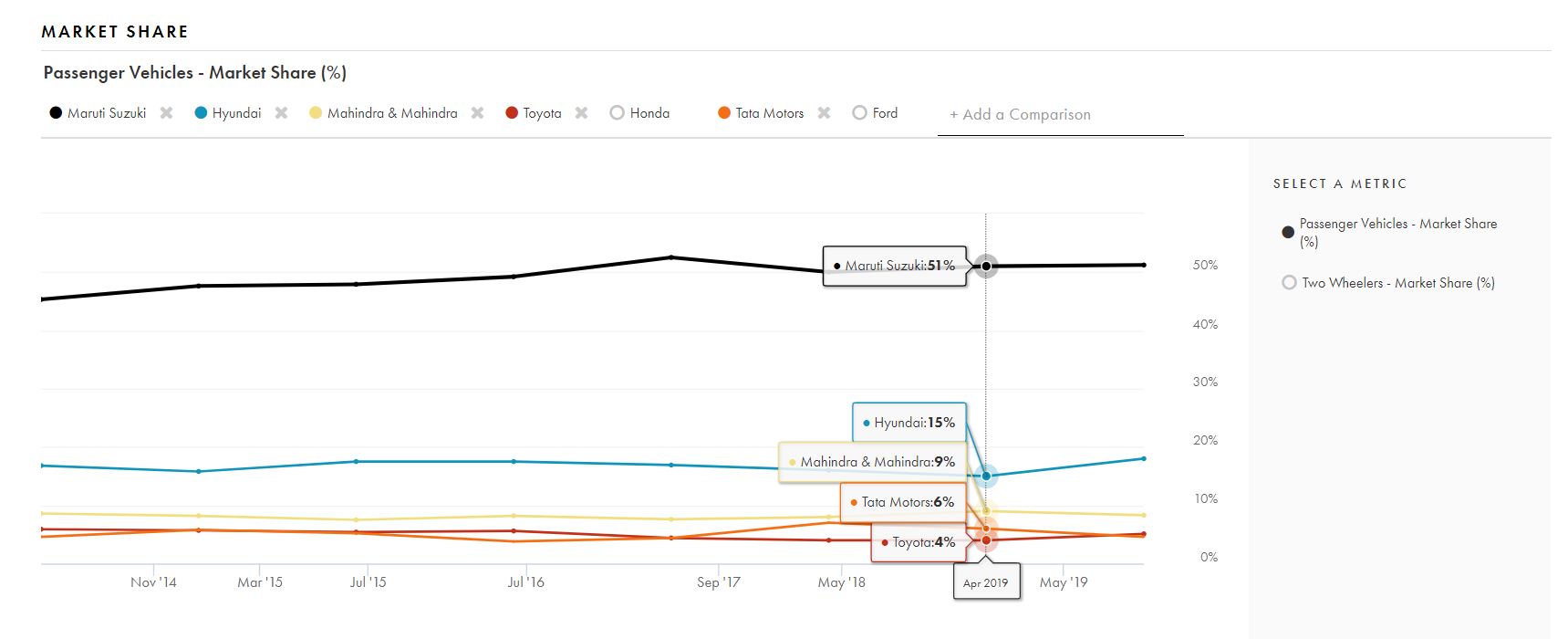

Market leaders Maruti Suzuki and Hyundai Motor India led the drop, with wholesale volumes declining by 17% to 111,014 units and by 7.3% to 42,007 units, respectively.

“The elections got over towards the end of May. Demand cannot revive overnight. The budget, new policies are yet to be announced by the government,” Maruti Suzuki chairman RC Bhargava told ET. “That said, wholesale numbers do not reflect the demand on ground. If we look at retail data on a month-on-month basis, it will give a better picture of consumer sentiments.”

Data with the Society of Indian Automobile Manufacturers (SIAM) shows retail sales of passenger vehicles declined by 1.28% to 264,035 units in April and by 1.46% to 270,048 units in May. The retail data for June is yet to be announced.

Auto’s are in bearish phase, and it is time to accumulate. Whether one likes it or not, passenger vehicles and commercial vehicles are just going to keep growing until everyone has 2-3 of these vehicles of some kind in the family.

Own it in SIP mode, since these are fallen angles and they also will one day prop up, and that day is not too far away in 2020-21-22. When the mad rush is out there, getting Maruti at 6000-7000 is going to be a dream.

Think Maggie…Think Pesticides…Think 5000 rupees for the stock, and now after all the Maggie pull back, reintroduction, and stock is MORE than double. Is that crazy or what?

The opinion now is that people will use cars as a service. That means a family may own 0 or 1 car. For this to happen, we may need excellent public transport along with a good private feeder network (ola/ Uber).

Even Singapore is yet to satisfy my needs for excellent end to end transportation. It is supposed to have the best transport network. However if I don’t take my car for shopping, it sometimes becomes very difficult. Imagine buying a truck load of bags from Mustafa and try to get a taxi during a rainy day. Taxi drivers should not ask where we want to go but they do ask and when I say that I need to go to Marymount, they decline and leave me in the rain. Next best option is to walk for 10 minutes to a bus stand or metro station, carrying 20 kg groceries. If situation in Singapore is not yet perfect, we can imagine when we can expect it in India.

Another issue is cost of transportation. Uber and Ola are expected to replace a car. However today it costs Rs. 600 per day to pickup and drop my kid in school if I take Ola or Uber pool. If I take my car, I will have to spend 150 on fuel.

Ola and Uber are not yet profitable, For them to be profitable they will slowly but surely raise the prises and we as Indian customers are prise sensitive. To top it off Ola/Uber have surge prising during peak hours and cost you almost double the prise during normal hours.

In tier 2 and tier 3 cities Ola/Uber has still not penetrated and people will definitely not pay the higher amount as the earning potential is slightly lower in those cities. Considering all these aspects plus above mentioned by Vijay and Patel there should be some revival in the sector. The only question is how long the pain is going to endure and once the revival happens in the economy all the CV, PV segments would pick up.

Disclosure: I have vested interest in Maruti .Please consult your financial advisors for any kind of recomendations

The world of all of us not owning cars, and AV will come to our home driven by Google and Apple technology even for USA is around 2025 to 2030. So, until then, we will be going from 1 vehicle in Indian families to 2 to 3 to 4 depending on number of earners, and how many live (where). So, parents might not have retired, and the son, and his wife is working, and they are not in a city with good public transportation.

So, Maruti, Bajaj Auto, TataM, Hero and others will do well, after this NBFC / Credits will improve in 2020. Borrowing will open up once Liquidity will start to open and the bad debts are paid off. Budgets might address the liquidity issue ‘somewhat’ but yet, the demand for transportation will come back like it has in the past.

I am getting into this sector slowly and diversifying well, so that I can earn more than 15% to 50% in some of these entities over the next 1-2-3-4-5 years.

The Poor Metro infrastructure , The Car Pool apps,Shuttle services, New Metro lines, will the trajectory of growth be same what it was for last decade ?

I take this analogy to compare it with a cloud (subscription based) vs the traditional on-premise model(where you buy the servers,storage etc and have to manage everything out of your own).

The research says that beyond 4 to 5 yrs, it makes sense to go for a traditional on-premise model compared to cloud because the TCO analysis favors on-premise model.

In India, people on an average keep the cars for more than 5 years, thus the premise that ola/uber are preventing people from buying cars is completely wrong in my view.Not to forget the exorbitant fares of late being charged by them, peak charges,dynamic fares etc.

Uber and Ola experiences are just pathetic. Huge waiting time. Unprofessional drivers. Surge charges. It can’t replace household cars until majority of the drivers behave professionally which is highly unlikely.

The whole problem is their association with unprofessional drivers for the sake of rapid revenue growth.

First of all, their business model is unproven yet. Not sure if they will even exist after a few years. At current prices, they have no profits. At higher prices, they have no revenues.

Going by porter’s analysis: They have threat of substitutes. Poor bargaining power with customers. Poor bargaining power with drivers. Negligible competitive advantage against each other. Only threat of new entrant is not there.

Also car is a status symbol in India. Visiting a wedding by a car vs a cab creates a lot of perception difference among typical Indians.

A first car purchase is almost 50% of PV sold today and that means the impact of ride sharing platform is going to be on the remaining 50% of market. It makes sense to have 1 car parked for emergency and occasional use. Recent statement from Maruti on rural growth seems significant and we should see that first time car buyers stay at 50% with less impact from ride share platforms.

i sold my existing car in early 2018. currently without a car and planning to buy one soon.

so here is my 2 bits :.

a family who can afford a car WILL buy a car. it gives status symbol, comfort and convenience.

ola, uber etc can never ever replace the convenience of a own car.

i have used self driven car n number of times since last year as an alternative of owning a car. Again, it is too much of hassles and robs away the fun and comfort that ones own car gives in.

for everyday office goers, there is a alternative of car pooling which is picking up nicely in metros. but again, is a car only for routine office going ? i feel much of the demand comes from tier 2 and tier 3 cities and the demand will only increase with increase in disposable income and standards of living.

So in all practicality, i doubt if the current sales drop will sustain for a long time.

i feel, we suffer from “recency bias” and try to rationalise everything that happens in the market.

But then again, i hold Maruti stock, so i may have some “ownership bias” too

While demand will come back at some point of time but other thing which Investors should keep in mind is PE expansion/contraction. Maruti and many other auto companies had great performance over last many years and in the process several of these companies got PE re-rating. Will these companies get the same high PE when the demand comes back ? Pharma companies are still growing but market is not giving them the same valuation as in 2014/15 period. There are many other examples of PE contraction of the whole sector when it loses market interest and it can take several years to reach the old glory. Lot of money is made and lost in PE re-rating and de-rating so just highlighting above based on my experience from other sectors otherwise I have no holding in Maruti or any other Auto company.

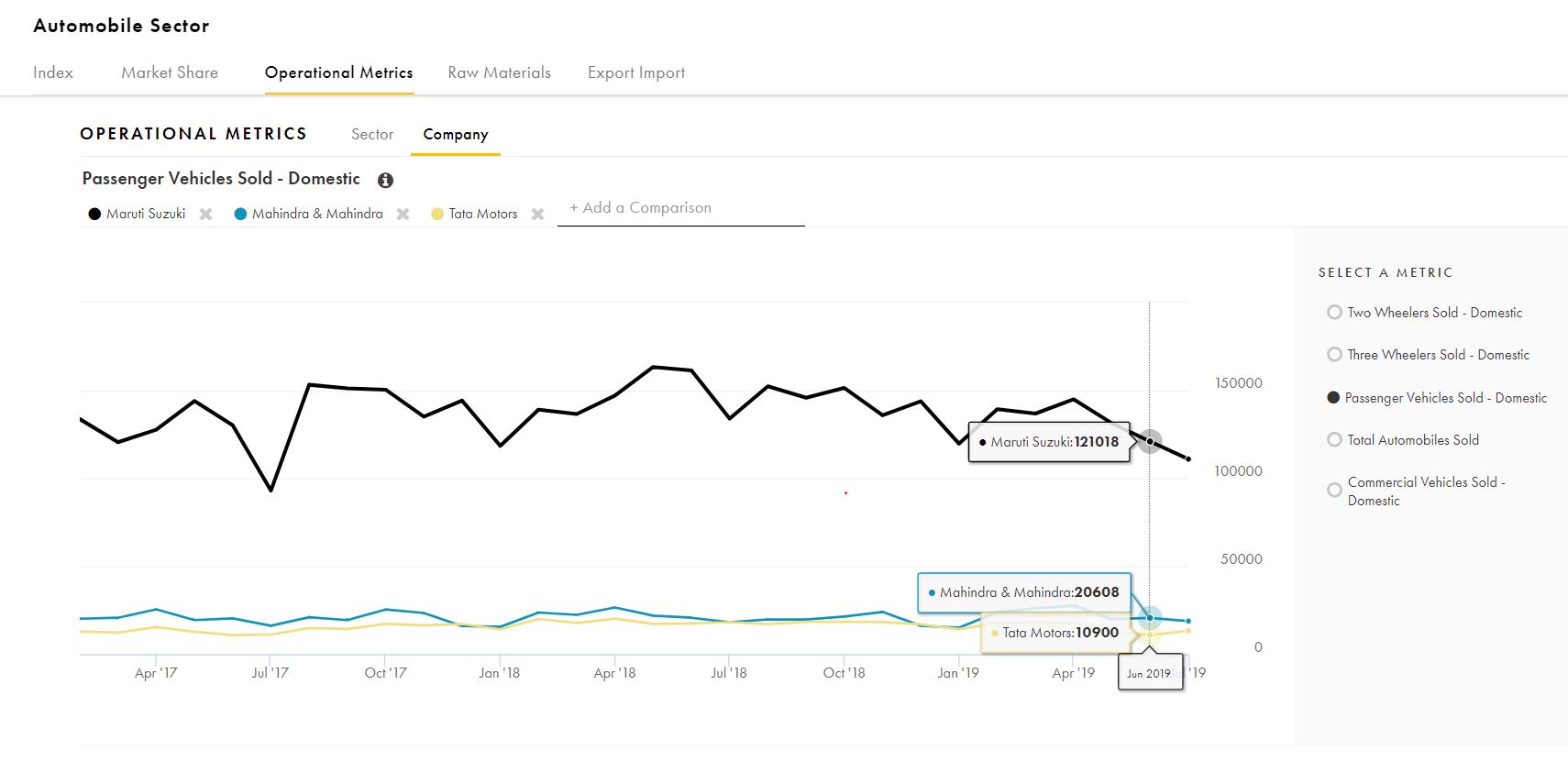

Just updated the auto sector screens with the latest sales figures as well as the market share info of the key players (including some unlisted companies). This data will be updated every month going forward.

Most sites like auto punditz have data points for last 10 years. If you want to stand out of the crowd, compile data for last 15 years. We can clearly see that auto sector growth is as slow as a snail and also market share of Maruti has taken big rollercoaster.

In my opinion any long term investor in Maruti should take note of EV (Electric Vehicle) disruption that is about to come in a big way in next 4 to 5 years. The ability Maruti to withstand itself in the new EV environment will be the key to valuation.

Till that time I think high valuation will be a constrain on the stock.