I did a deep dive to understand the Maruti Suzuki India Limited (MSIL). Here are the notes for everyone’s scrutiny-

About the Company

Incorporated in 1981, MSIL, which is the market leader in the domestic passenger car industry, was established in 1981. In 1982, a JV agreement was signed between the Government of India(GoI) and Suzuki Motor Corporation (SMC), Japan, whereby SMC acquired a 26% stake in the MSIL. The Company became a subsidiary of SMC, which currently holds 56.21% of its equity stake, in 2002. By September 2007, GoI had offloaded its equity to Indian financial institutions, including banks and mutual funds.

MSIL currently has 17 models with over 150 variants across segments and has a market share of 51%+ in India’s Passenger Car segment. The Products are:

1- Passenger Cars: Mini(Alto, S-Presso), Compact(Wagon-R, Swift, Celerio, Ignis, Baleno, Dzire. Tour S), Mid-Size (Ciaz)

2- Utility Vehicles (Gypsy, Ertiga, S-Cross, Vitara Brezza, XL6) & Vans (Omni, Eeco)

3- Light Commercial Vehicle (Super Carry)

The company has manufacturing facilities in Gurgaon (two plants) and Manesar (three plants). The manufacturing capacities of the company has evolved as below over the years:

In January 2014, the MSIL board approved a proposal from Suzuki Motor Corporation, Japan, (SMC) to implement the Gujarat expansion project through a 100 percent subsidiary of SMC. In Q4FY17, Suzuki Motor Gujarat Private Limited (SMG), a subsidiary of SMC, became operational in Hansalpur (Gujarat). Through this new facility, which is fully financed by Suzuki Japan, an additional annual production capacity of 0.5 million units has been made available, thereby taking the combined production capacity to a little over two million units. MSIL, which aspires to sell 2 million units in the near future, is responsible for the sales and distribution of units produced at the SMG and had set up a Sales & Distribution facility at Hansalpur, Gujarat, in FY17. As per latest RATING Report from CRISIL “Besides manufacturing vehicles at its own plants in Gurgaon and Manesar in Haryana, it sources vehicles from SMC’s wholly-owned subsidiary in Gujarat, Suzuki Motor Gujarat (SMG), under a contract manufacturing arrangement, wherein the vehicles will be sold to MSIL at cost. Plant I at Gujarat was completed and started commercial production from February 2017 with an annual capacity of 2.5 lac units. In January 2019, SMG completed the construction of Plant II and started production. Plant II also has an annual capacity of 2.5 lac units. Along with Plant II, the powertrain plant has also become operational. Construction of Plant III has already begun and the same is expected to come online in fiscal 2021, taking the capacity of the Gujarat plant to 7.5 lac units annually and cumulative installed capacity of MSIL plus SMG to 22.5 lac units.”

MSIL & SMC: Joined at the hip-

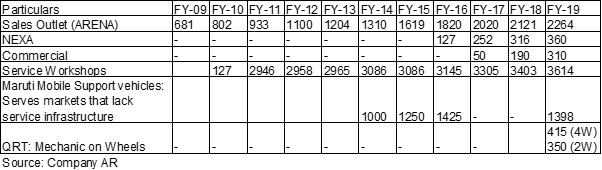

As MSIL is now SMC’s largest subsidiary in terms of production volume and sales, SMC will benefit immensely in keeping MSIL highly competitive and agile in manufacturing, technology, and market response. The SMG set-up seems to be a giant step in that direction. While the back office job of incremental manufacturing engagement is outsourced to a trusted partner, MSIL could provide more focus to strategic areas including R&D, new products, and infrastructure for marketing and sales. Due to the bandwidth created by this arrangement, MSIL has primarily focussed on front end key activities such as the creation of sales channel, established 350 outlets under NEXA channel and 310 outlets for LCV in a span of 3 Yrs, and acquisition of land parcels to expand the network, which ensures to provide the best value over the period of Vehicle ownership and the land is the most important resource for its fast-paced expansion. As shown in the below table, the company is laying the foundation in the form of network to achieve the sales to the tune of total available capacity of 2 million as and when demand rebounds:

What’s interesting?

• Dividend Policy: Dividend pay-out ratio will be within the range of 18% to 40%

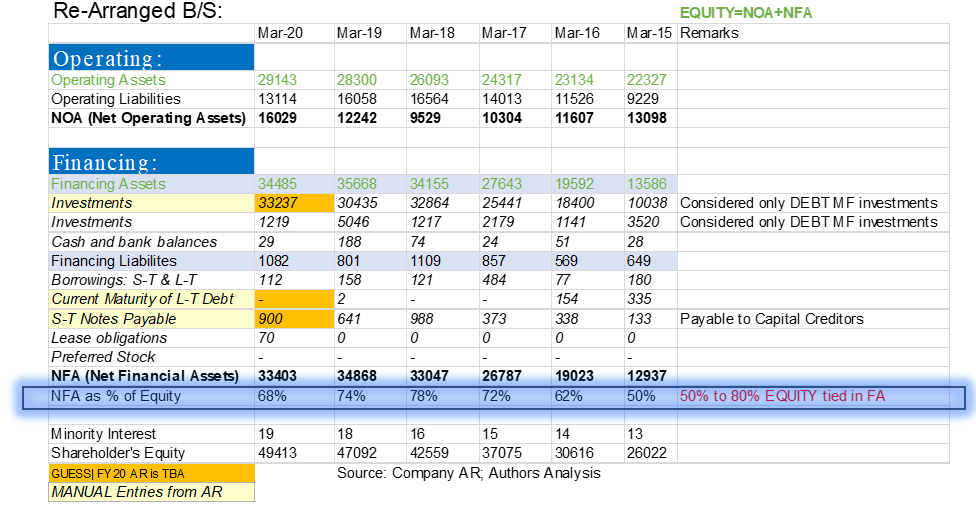

• Business has staying power due to a strong Balance sheet (B/S). As of FY20, B/S is almost debt-free & 59% of total assets consist of investments. Out of these investments, 30K+ Cr. is invested in Debt MF schemes.

• Building foundation to encash demand revival in the future by –

o Buying land parcels for sales and service outlets in order to better dealer viability & faster expansion.

o Production capacity at SMG is in place and can be expanded as and when the opportunity arises.

o The vast and expanding network of Sales and Service.

• Aspires to increase the share of vehicle dispatch, through rail mode, and has dispatched around 8% of the vehicles during FY19.

• Working on Electric Vehicle (EV) development. Till the time EVs gain prominence overcoming the lack of infrastructure and high costs, a more workable solution is in place as a business partnership b/w SMC and Toyota Motor Corporation to promote other powertrain options of clean energy based on hybrid technology.

• Lions share in the Domestic PV segment: Under the leadership of K.Ayukawa (MD & CEO), the market share of MSIL has improved from 39% (FY13) to 51% (FY20).

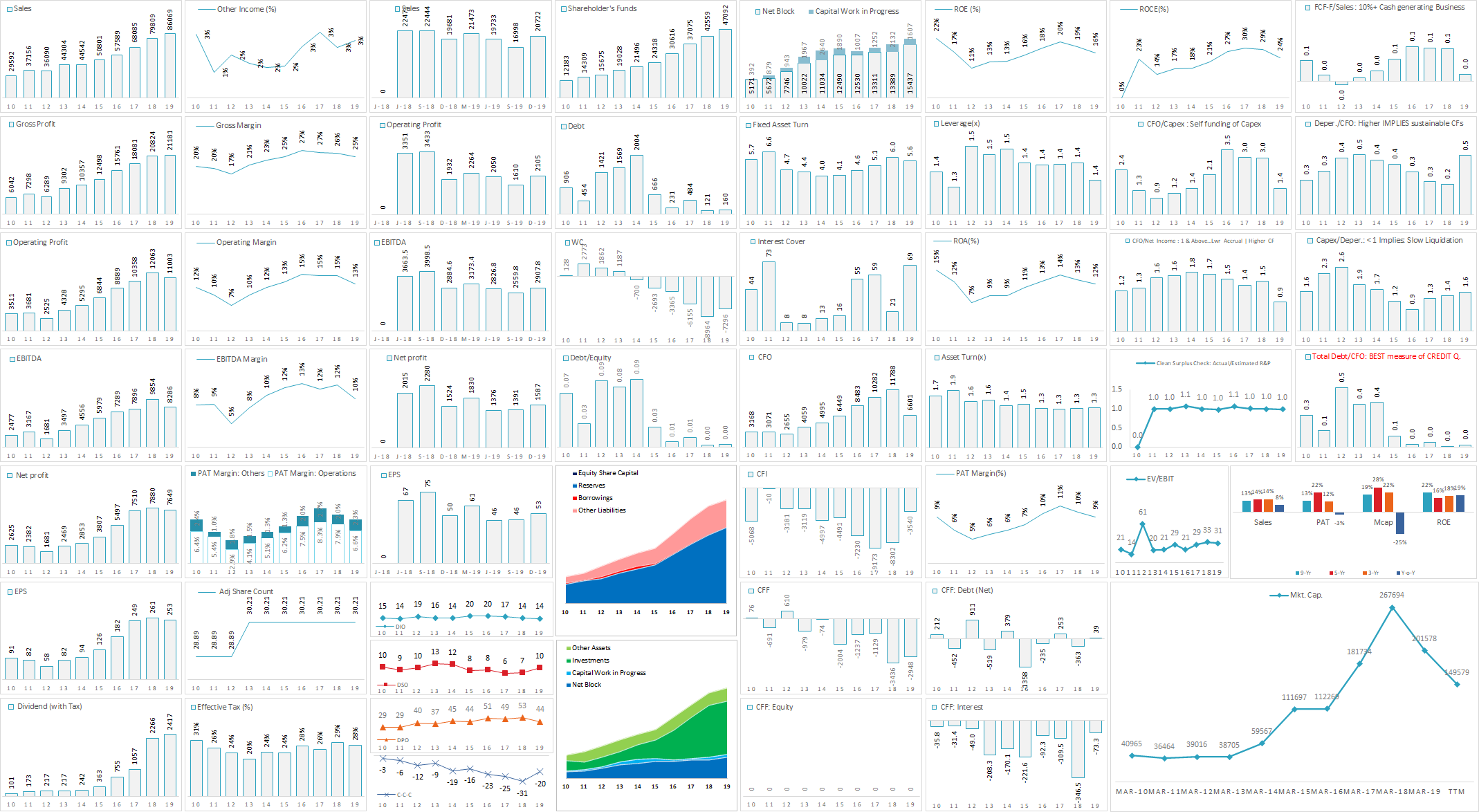

• Excellent efficiency to convert Sales to Cash:

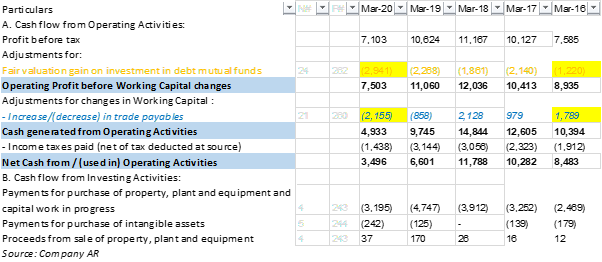

• Both Cash flow from Operations and Free Cash flow are positive for the company in the last 5 years:

The huge dip in FCF of FY-20 as compared to FY-16, compared these two years as their PBT is in ballpark range, seems reasonable as it’s contributed by 2 items majorly - highlighted in yellow in the below snapshot:

• Improved profitability and cash flow have resulted in a ballooning Investment book (amount in Cr.) as shown below. The majority of these investments (~93%) are in Debt MF.

What’s not so pleasant?

• Due to the cyclical nature of the industry, the profitability of MSIL may be stressed during downcycle as it’s a volume player (~50% of the domestic market) with fixed committed cost in terms of own as well as SMG plants. However, a challenging business environment should be an opportunity for the company to improve its market share by supporting business partners by harnessing the strength of the pristine balance sheet.

• Hyper competitive market that allows new entrants who are lured by India’s PV market potential due to extremely low car penetration rates.

• Stringent regulatory changes in the future will lead to an increase in product prices, a key factor for Indians to buy the entry-level vehicle, or postpone the purchase, of entry-level cars.

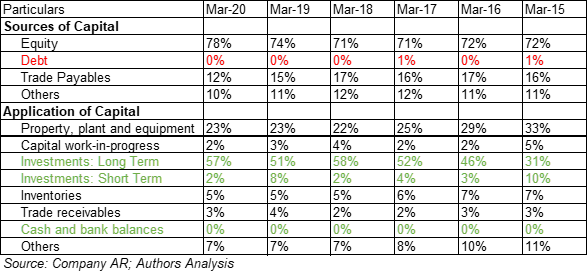

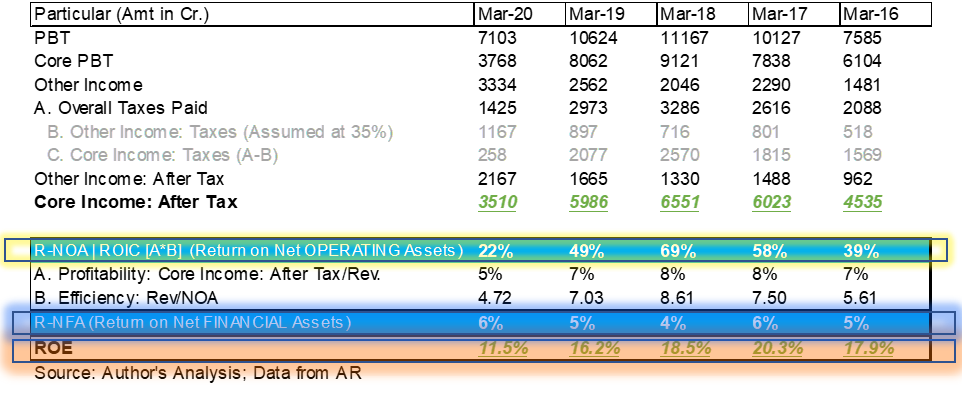

• Suppressed ROE as ~70% of EQUITY (Refer NFA as % of Equity in Image 1) is tied in financial assets that earn post-tax returns of about 6% (Refer R-NFA in Image 2). What’s the plan to utilize the Financial Asset? I have no idea yet but it remains a key item to track in the future. In image 2, ROE for FY-20 is 11.5% but the return on Operating Assets (RNOA), which is hidden in numbers, is 22%. Overall calculations are as shown below:

IMAGE-1:

IMAGE-2:

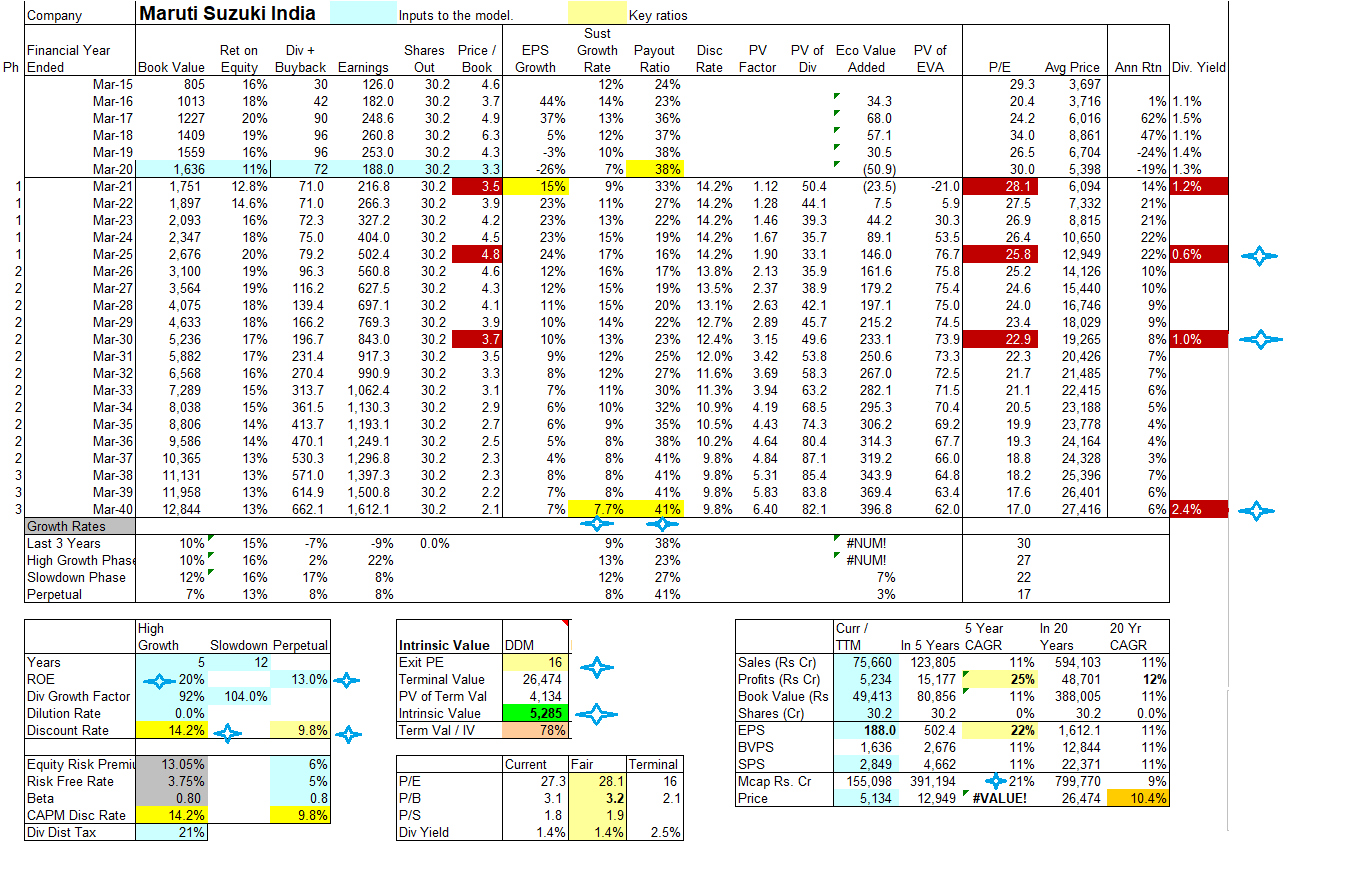

Valuation:

The key characteristic of the business:

It’s a cyclical business whose basics are new products, productivity, cost, quality, and customer service.

A correlation b/w the growth of the company and either the GDP or industry’s growth could not be established but it’s evident that compounded revenue growth stands in the range of 10~15% depending upon what period one opts among 10Yr, 7 Yr, 5Yr or 3 Yr keeping FY-09 as the base year. Data for the past period is as shown below –

How much to Pay? Here are the past numbers as charts from our beloved screener.in:

Although it’s homework for all of us ![]() , I am sharing mine using the wonderful template/model provided by @Yogesh_s @ Spreadsheet Model for Valuation of a Company

, I am sharing mine using the wonderful template/model provided by @Yogesh_s @ Spreadsheet Model for Valuation of a Company

Note: Star marked entries are subjective. I inverted the DCF by assuming that the market price reflects the true value of the company in order to understand the baked expectations,

Critical Risks:

• Regulatory Changes (Vehicle Fuel Economy, Emissions, and Safety):

Impact: Increases the price of Vehicles and may affect customer demand.

Mitigation: Continuous technical support from Suzuki Japan; VA-VE and Localization by India R&D center to devise economical alternatives.

• Labour relations for smooth manufacturing operations (Manesar plant incident in July 2012)

Impact: Emotional and financial impact that leads to bad press/goodwill among the stakeholders.

Mitigation: Focus on EMPLOYEE WELLBEING- Besides medical insurance, the Company also facilitates a housing scheme for workers to enable them to own a home. Subsidized meals are provided to regular staff, while free meals are served to contractual staff. Active efforts to improve INDUSTRIAL RELATIONS- The Managing Director has monthly meetings with the unions and the senior management has regular meetings with unions, associates, and supervisors.

• Exposure to Forex Risk | Japanese Yen:

Impact: TBD.

Mitigation: TBD.

• Exposure to commodity prices:

Impact: TBD.

Mitigation: TBD.

• EV:

Impact: TBD.

Mitigation: TBD.

Disclosure: This note is created to improve my understanding of the business and shared for others feedback/learning and the same should not be used as investment advice. I am not an investment advisor and do not own the stock.