Even I think so. Isn’t softgel just the outercover for medicine or is it something more. What is so special about it.

ROE has been continuously increasing and currently at 20%…

1 Like

Isnt there any benefits for Marksans under PLI scheme?

1 Like

The current margins don’t account for R&D expenditure, in future as they do R&D which is 10% of sales as the CEO said in AGM, the margins will significantly normalize to 17-20%, assuming the niche molecules revenue proportion doesn’t change

2 Likes

I am here providing some background about the company. It is a turnaround with very high profit margins around 25%, ROCE 30% and 200cr cash reserves in the balance sheet and 10th largest generic player from India in the USA also a significant player in regulated markets like the UK, Australia and Europe. They have a front end presence with medical representatives, also they do private labeling business for pharmacy chains. Now they are focusing more on niche softgel formulations in the crowded generic market, it is patent protected and complex to manufacture. At this point the R&D expense(3% revenue) is low because they are able to grow by acquiring product licences through inorganic routes. Once the proportion starts changing in the business mix with more of this niche formulations vs commoditized business margins may normalize(I dont have the complete clarity at this point how it will unfold). Considering their size and the problems they have solved by concentrating on formulations (sold their API business 8 years back) through scale I think it is a commendable job. Unlike other Indian companies focusing on the commodity APIs trying to be cost efficient they are positioned in a different way.

Considering their future plan to get into a few APIs where they have significant market share in the end product will be a good competitive advantage and more share in the value chain economics. Going forward the company has guided for higher R&D expenses(10% revenue) 2-3 years down the line. But with focus on soft gel formulations i don’t think it puts pressure on margins from the current 25% they are clocking(my estimate). The softgel space is 9bn $ and expanding as it offers a better drug delivery system when consumed. They have 6 product approvals pending alone in the USA.

Valuation:

It is undervalued and at a huge discount to healthcare sector valuation on a PE or EV/EBITDA basis. Assuming no growth with the current orderbook(100mn $ in USA alone and no growth from other economies) 1500 cr sales in FY21 (1020cr already in last 3 quarters) and 240 cr profit from next year and is available at 2200 cr Mkt Cap. Current capacity utilization is 70%, they have started a 200cr capex program over the next 3 years.

Also there are HNI investors too like Ashish Kacholia, Mukul Agarwal.

I see limited downside considering the equity valuations at index level currently.

16 Likes

Excellent analysis. Too many red flags

9 Likes

maybe this is the reason no research house is covering the stock

3 Likes

Some other items that could have been included in the above is that the same UK MHR in 2017 Feb completed inspection of the same goa plant without issuing any critical observations on the facility. The co also received an EIR from the USFDA for their Goa plant in June 2019. The FCCB issue is now resolved and the co is debt free. However, it is true that equity dilutions have been a drag. The net impact of the FCCB debacle is that the co came out of BIFR and has done everything since then to clean up the balance sheet.

On the price erosion, it was faced across the board by all export oriented pharma cos so that issue is not specific only to Marksan but a general issue for all cos in the sector in that period.

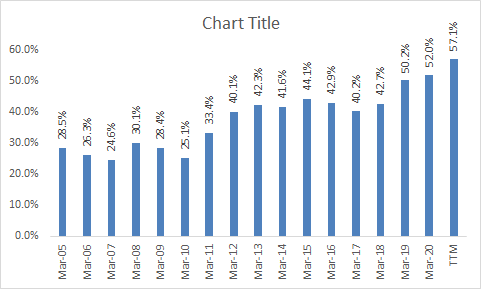

Another important aspect the above document overlooks is the continuous gross margin improvement that has taken place over the years. The TTM gross margin is in fact ~ 57% prompting the management to say that it may not be sustainable.

WC requirement has remained fairly stable since the last 3 years at 34%-36% of revenue and the co seems to have completely recovered from the past troubles.

Complex math like SSG rate and the like is not required to see that only investments in WC are required to grow and co had utilized only 38% of its fund limits as of 2020.

With due respect to the author of the article, I think that some important points that needed to be highlighted along with the points mentioned above could have made the stock story more balanced.

15 Likes

Fantastic Q-4 Results - FY21 Operating Revenue at Rs. 1,376.2Cr.; growth of 21.3% YoY EBITDA at Rs. 339.6Cr., growth of 76.6% YoY.

Business Highlights

US & North America Formulation business reported growth of 34.2% YoY to Rs.585.5 Cr.in FY21.

US & North America Formulation business reported growth of 34.2% YoY to Rs.585.5 Cr.in FY21.

Company achieved revenue of Rs.582.0 Cr. from Europe, UK Formulation business in FY21 as compared

to Rs. 510.0 Cr. achieved during last year same period registering growth of 14.1%.

o Launched 5 new products in UK in FY21.

R&D expense for the year FY21 is at Rs.18.9 crores.

Generated strong Cash from Operations and Free Cash Flow of Rs. 178.7 crores and Rs. 132.3 crores

respectively

Strong balance sheet with Cash and Cash equivalents of Rs. 212.3 Cr.

Product Pipeline:

o Plan to file 12 ANDAs in US and over 20 MA’s in UK and Australia in the next two years

o Plan to file 7 DMFs over next 2 years for API business

Capacity expansion at US facility completed with addition of packaging and manufacturing lines

Company plans to incur capex of Rs. 200.0 Cr. over 2 years for both Formulations and API business

Currently undergoing capacity expansion for softgel capsules in Goa

10 Likes

meeting of the board will be held on June 15th to consider convertible warrants on a preferential basis worth Rs 372 Cr

Co to issue warrants worth Rs 365 cr to PE OrbiMed Asia Mauritius

Co to issue warrants worth Rs 7.4 cr to Promoter Mark Saldanha

Issue Price Rs 74.

As the co is debt free my assumption is that this funds will be utilized for growth.

Disc: invested

2 Likes

I think after recent Con call where many fund houses were present and probing Mr. Saldanha. This news is a positive as another fund is investing through warrants. Amount is also quite big.

We will have to see how market take this news from tomorrow onwards. But clearly Mr. Saldanha is slowly by solidly building the company. Not in a hurry but with great fundamentals.

Thanks

4 Likes

Yes, I think that the funds will most probably used to foray into the API space (backward integration).

In the last Con-call Mark said that they will use internal accruals and maybe debt to invest into the API space but I think with these new funds, the co would not have to take a lot of new debt or maybe not take on debt at all.

Lets see what happens tho. Market seems to be taking this Orbimed fund news positively as the shares are locked in 20% Upper Circuit today.

Disc. Invested at lower levels

1 Like

The company has more than enough cash on the BS + will generate enough cash flows over the next one year to meet it’s capex needs. Why dilute equity at this point? Seems it’s to build credibility. A lot of investors do not want to touch it (it’s the cheapest generic pharma name) coz of it’s GDR issues.

1 Like

Screener shows that Marksans has Cash equivalents of 212 crores as of March 2021 which would have been enough for the 200 cr capex over the next 12-18 months as guided by the management. Now they want to issue Convertible warrants to a top fund, the purpose of this remains unclear and I feel it’s more of a promotional thing. The fund will have an option to convert those warrants to equity at a fixed price in the future if the company performs well and if the company fails to deliver they will still receive the interest payment; so the fund has nothing to lose.

2 Likes

Can you explain a little more about GDR issue or give a pointer, where one can read about the issue?

Google search about the issue returns nothing useful.

Thanks.

When they issue a warrant with 18 months time frame for conversion and collect only 25 percent at time of allocation and dilute the equity by 5 cr when the total value is 375 cr u get only 125 cr now any seniors can throw some light is this some kind of corporate governance issue

1 Like

Most of the warrant issues follow the same route as taken by Marksans. I don’t see any corporate governance issues here. Can you point towards more specific issues with the issue?

1 Like

Sorry not GDR’s but the FCCB’s they issued.

https://www.drvijaymalik.com/analysis-marksans-pharma-ltd/ Read the section about “Yalegove Limited”

I don’t think that an issue as old as 2011 will have any bearing on how company is operating now!

Company is now debt free and generating enough cash to fund it’s expansion. When market undervalue’s a stock it gives opportunity to participants to make some money.

Disclaimer - Invested therefore views could be biased.

1 Like

You are right it’s not an issue due to BS position. It just exhibits promoter’s character (ie whether they are Minority Investor friendly or not). To extend the argument it’s possible promoter has realized that he doesn’t need to engage in past behaviour as well.

Also I have questions around why did the UK business start doing so well over the past couple of years? To the extent, I understand one of their closest comps pulled out of the pharmacies (due to supply chain issues) and Marksans took their spot. Question is will the comps come back as supply chains resume or the pharmacies will just prefer to continue with Marksans?

I don’t know how these things play out but I would watch this one closely.

3 Likes