Dear community members,

I’ve not been able to find the concall link for Q4’23 would be great if anyone can share it with me.

Now coming to what I’ve understood from the management interview and the investor presentation:

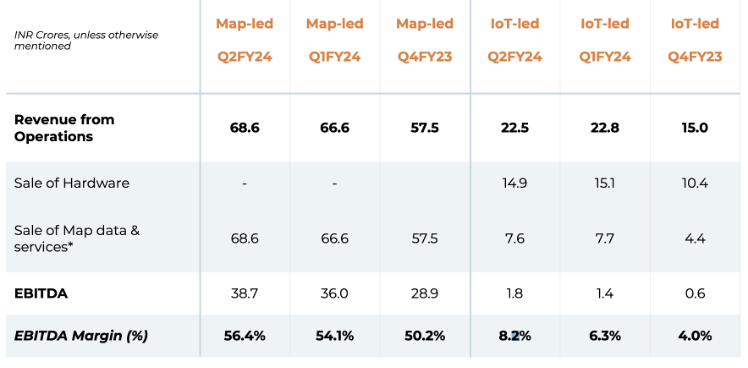

Value of Business w/o IoT

| FY2022 | FY’23 | Growth |

|---|---|---|

| 175.4 | 223 | 27% |

| 85 | 117 | 37% |

| 48.46% | 52.40% |

Assumption: Since the share of services in the IoT was higher in last FY, I’ve assumed the EBITDA number to be same as this year.

Takeaway: Company has always maintained that its core business has very high contribution margins. This is reflected in the EBITDA expansion. Operating leverage is evident in these numbers.

Value of IoT Business:

| FY2022 | FY’23 | |

|---|---|---|

| Hardware | 16.5 | 42.2 |

| Service | 8.1 | 16.8 |

| EBITDA | 1 | 1 |

| EBITDA % | 4.07% | 1.69% |

Takeaways:

Hardware business has grown on the low base. Still growth has been good.

Services have doubled, as per the management guidance/commentary the services growth will follow hardware sales with a lag.

On the business vertical side:

With revenue of 152crs vs 113crs A&M Business saw a growth of 34%. (this is higher than the industry growth). This was also impacted due to shortage of semiconductors.

C&E Business witnessed a growth of 48% with revenue going up from 87.4crs to 130crs in FY’23

| A&M | C&E | A&M | C&E | A&M | C&E | A&M | C&E |

|---|---|---|---|---|---|---|---|

| Q1’2023 | Q1’2023 | Q2’2023 | Q2’2023 | Q3’2023 | Q3’2023 | Q4’2023 | Q4’2023 |

| 33.2 | 31.9 | 38.9 | 37.3 | 40.1 | 27.5 | 39.5 | 32.9 |

| 65% | 37% | 47% | 24% | 45% | 76% | 2% | 80% |

| Q1’2022 | Q1’2022 | Q2’2022 | Q2’2022 | Q3’2022 | Q3’2022 | Q4’2022 | Q4’2022 |

| 20.1 | 23.3 | 26.4 | 30.2 | 27.7 | 15.6 | 38.7 | 18.3 |

If we look at the sales product wise then we can see that the platform business posted a growth of 45% and the maps business posted a growth of 34.5%

| Map & Data | Platform & IoT | Map & Data | Platform & IoT | Map & Data | Platform & IoT | Map & Data | Platform & IoT |

|---|---|---|---|---|---|---|---|

| Q1’2023 | Q1’2023 | Q2’2023 | Q2’2023 | Q3’2023 | Q3’2023 | Q4’2023 | Q4’2023 |

| 27.2 | 37.8 | 32.2 | 44.1 | 13.4 | 54.3 | 39 | 33.5 |

| 54% | 47% | 18% | 50% | 79% | 51% | 27% | 28% |

| Q1’2022 | Q1’2022 | Q2’2022 | Q2’2022 | Q3’2022 | Q3’2022 | Q4’2022 | Q4’2022 |

| 17.7 | 25.7 | 27.2 | 29.4 | 7.5 | 35.9 | 30.7 | 26.2 |

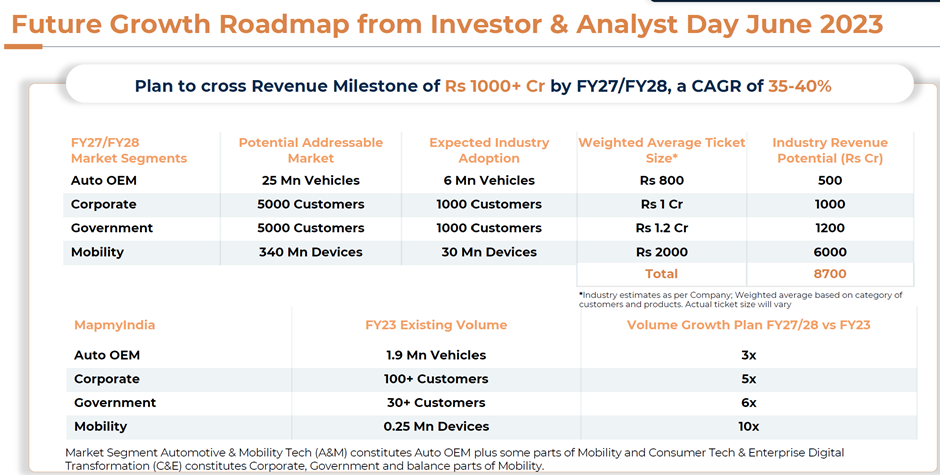

for the next year company is guiding for the following:

- Growth will be higher than current year.

- Services revenue from GTropy business will start contributing.

- Look at inorganic route (Rolta)

- Higher adoption of ADAS will aid the growth in A&E segment.

- Company is focusing on Drones as the future of growth

- Will look to acquire more customers for its Mappls app.

- Looking to expand company’s hardware offerings. (Navigation assistant etc)

- EBITDA Margin will remain in the 35-45% band.

My take here:

- All the segments that the company is focusing are growing at a very healthy rate and will continue to do so in the coming future.

- As the company adds more services revenue the profit growth will accelerate at rate > revenue growth.

- Company is enhancing its offering by bolt on acquisitions

- Drones can be a big play in the future