Went to website of GTropy Systems (latest acquisition) and it was surely not what I expected.

The website is full of dead-links (Link which don’t have linked pages).

Any of the solutions listed doesn’t have a page, case study page has UI issues, Products page show asset tracking and personal tracking products as blank, even their Career page take you back to the same page if you try to apply. Handouts - Brochure - Page not found.

None among the below link (except requesting demo / become partner) works in this section. I thought we may find it’s reason in FAQ but that don’t work either. Linked-in and twitter link at the bottom - Nah !

https://gtropy.com/ - Please somebody check, in-case this is just specific to my chrome browser.

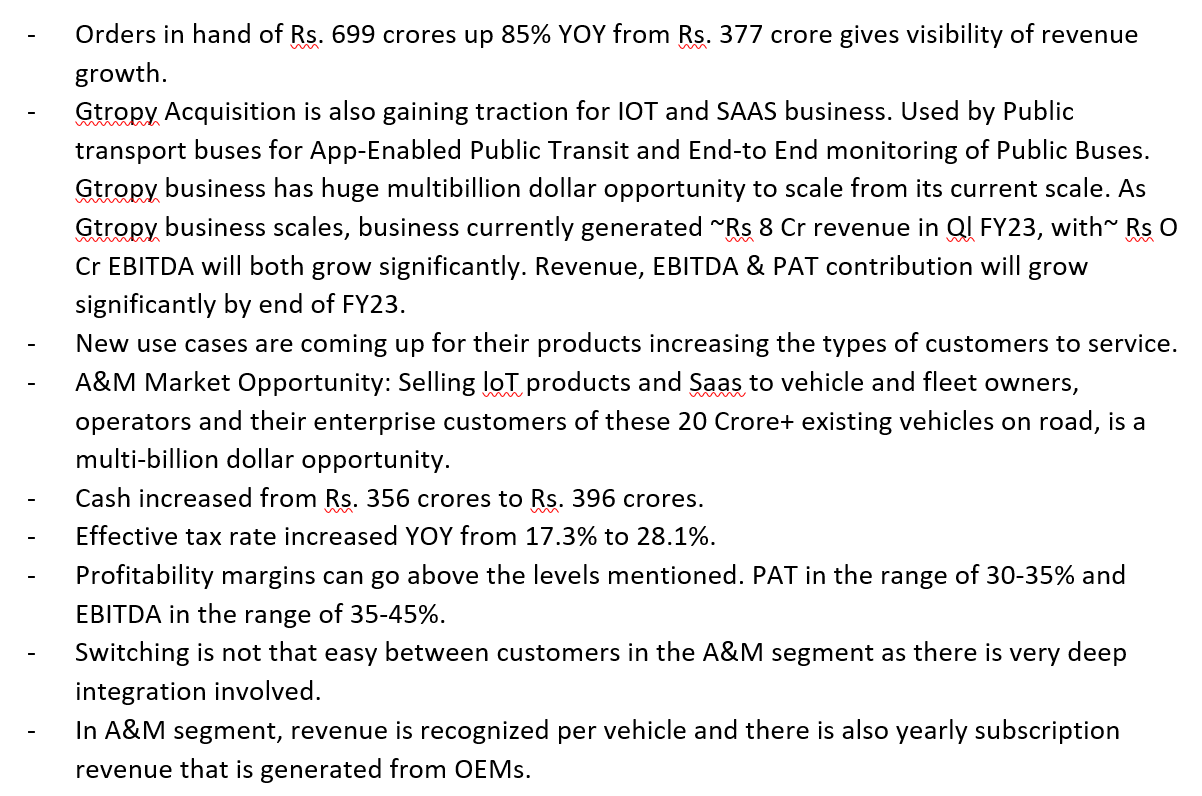

Nevertheless, As mentioned in the circular by MMI, Sales for Gtropy in FY19 was 0.04 Cr, Hence one can presume company is founded in FY19 or before. However, Linked-in profile of both the founders says otherwise. Both Founders (as per linked-in profile) started GTropy in Jan 20.

Both of them were also founders of Axestrack Software Solutions Pvt. Ltd before Jan 20, which is doing same business as GTropy.

Coming to Products, It seems they sell GPS Vehicle Devices and One App (named the locate - the great app) that shows the location of that device. They mention 1Lac App downloads on site, however google play store is showing 10k Downloads (probably a typo  )

)

They have got clients such as TVS Logistics, Pernod Ricard, Suzuki, Honda, Diageo, Hathi Cement, Baroda Freight Carrier, Wonder Cement, DGFC

I am not sure what is the basis for this acquisition. I don’t see this as value accretive or any skill as MMI already has these products and such software ( I believe a better one) and also access to most of these clients.

One thing that I could think of is may be this will give MMI a foot in the door for some of the GTropy clients like cement and pernod.

| Disclaimer - Still have a tracking position. These are just observations and opinions. Might Sell. Views could be biased.