Over the past few weeks, I have been analyzing Manorama Industries. Sharing my notes below:

THE BUSINESS STORY

It all began with a woman making oils in her kitchen. In the 1940s, in a modest home in Raipur, a housewife named Manorama would crush groundnuts and other seeds by hand, extracting oil that her husband Janakilal Agarwal would sell door-to-door. It was a humble beginning, a bucket of oil and a bicycle, for what would eventually become a company supplying specialty fats to some of the world’s largest chocolate and cosmetics makers. This is the story of Manorama Industries.

The piston expeller that changed everything

Janakilal Agarwal was born into a family of modest means in what is now Chhattisgarh. As a young man in the 1940s, he watched his wife laboriously press seeds to extract their precious oils. He saw an opportunity. In 1955, he acquired a piston expeller, a mechanical device that could crush seeds far more efficiently than human hands and set up a small factory in Raipur. He named the business after his wife: Manorama.

But Janakilal wasn’t content to simply run a small-scale oil operation. He had a curious mind, and he wanted to understand the science behind his trade. In an era when few Indian businessmen pursued advanced education, Janakilal traveled to London to earn a PhD in fat chemistry. This decision would prove transformational.

In London, Janakilal studied the molecular structures of fats. He learned how different oils behaved at varying temperatures, how they crystallized, and how they could be blended to mimic more expensive fats. He discovered that oils from seemingly worthless sources (banana peels, mango kernels, sal seeds) had properties valuable in industrial applications. The seeds that tribal communities in central India had been ignoring or discarding for centuries contained fats that, properly processed, could substitute for far more expensive ingredients in chocolate and cosmetics.

The legendary trade fair story

What happened next has become company legend. Armed with his PhD and samples of his specialty fats, Janakilal traveled to international trade fairs in Germany and France in the 1970s, hoping to attract buyers from global food and cosmetics companies. But he had no money for elaborate booth displays or professional marketing materials.

His solution was audacious. Unable to afford display materials, Janakilal reportedly smeared his products (cocoa butter alternatives and cosmetic butters) all over his own body. He stood at the exhibition hall, his skin glistening with mango butter and sal fat, inviting potential customers to touch and feel the quality of his products. It was unconventional, to say the least, but it worked.

At one such trade fair, his unorthodox demonstration caught the attention of Ferrero, the Italian chocolate giant behind Ferrero Rocher. They were intrigued by this Indian entrepreneur covered in exotic butters, and more importantly, by the quality of his products. The cocoa butter equivalents he had developed from sal seeds and mango kernels could help stabilize chocolate, preventing the dreaded “bloom” that occurs when chocolate experiences temperature fluctuations. A partnership was born.

From waste to wealth: the business model takes shape

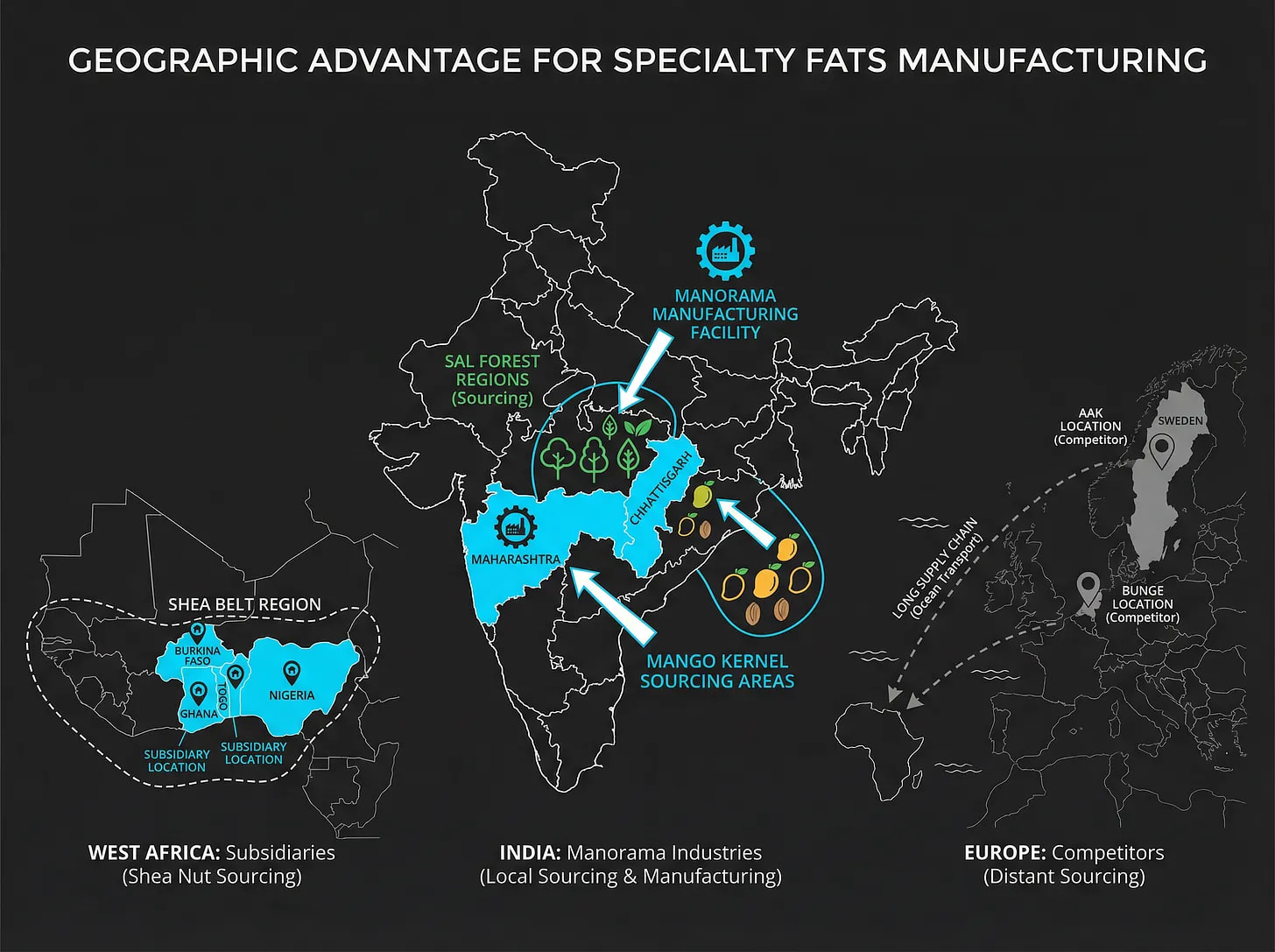

What made Manorama’s proposition uniquely compelling was the raw material sourcing. In the dense forests stretching across Chhattisgarh, Jharkhand, Odisha, and Madhya Pradesh, tribal communities had long collected sal seeds (from the Shorea robusta tree) and mango kernels during the monsoon season. For them, these were minor forest products, useful for making traditional soaps or oils, but largely overlooked as a commercial opportunity.

Janakilal realized that these discarded seeds, properly processed, could become cocoa butter equivalents (CBE). These fats mimic the crystallization properties of expensive cocoa butter but at a fraction of the cost. Cocoa butter, derived from cocoa beans grown primarily in West Africa, is essential for chocolate manufacturing but increasingly expensive and supply-constrained. Sal fat, in contrast, could be sourced abundantly from India’s forests.

The business model that emerged was genuinely innovative: buy “waste” seeds from tribal collectors, process them into high-value specialty fats, and sell to multinational food and cosmetics companies. It was “waste to wealth” before that phrase became fashionable. They turned what nobody wanted into ingredients for Ferrero Rocher chocolates and L’Oréal cosmetics.

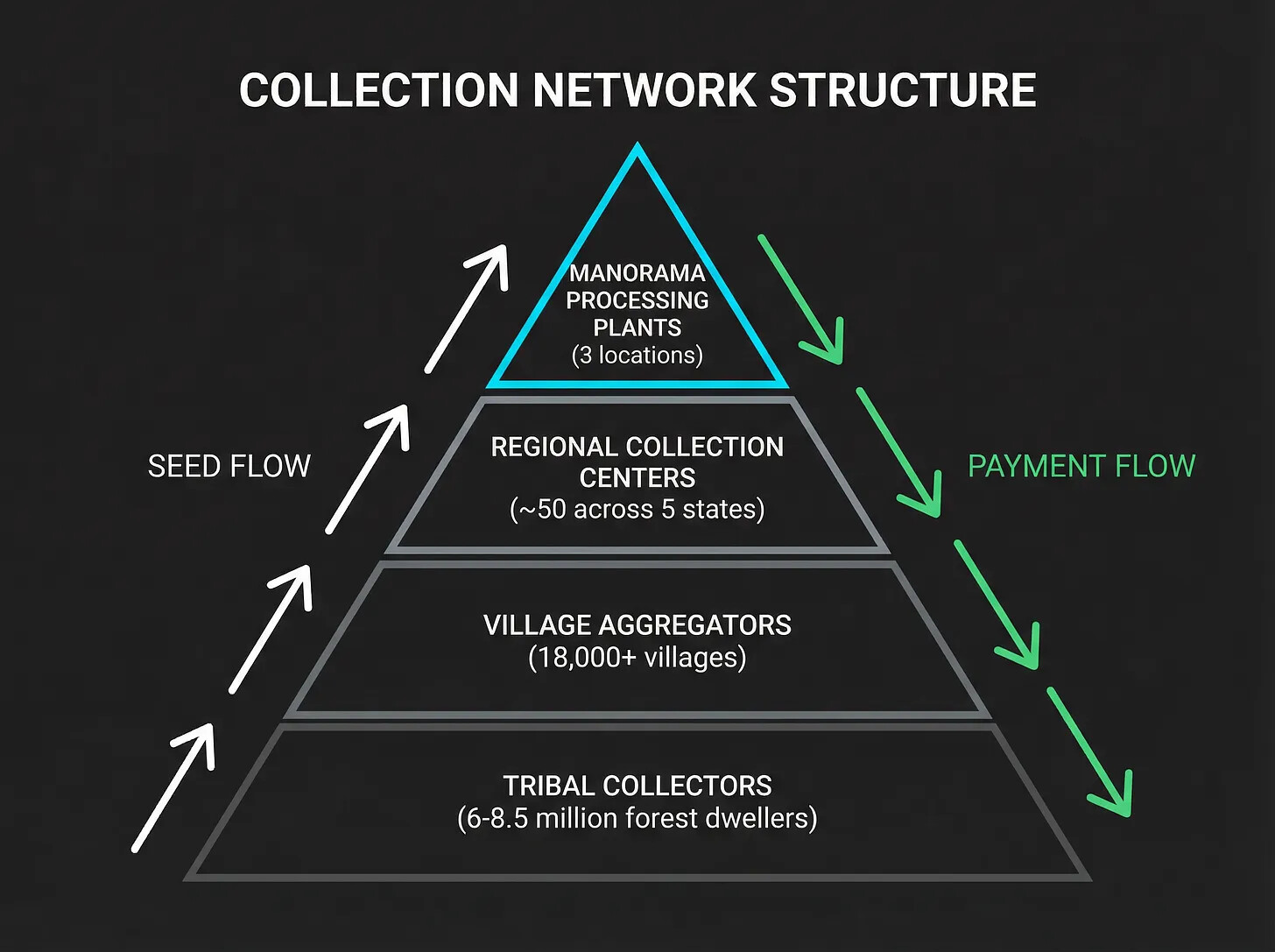

Over decades, Manorama built a procurement network spanning over 18,000 villages, engaging an estimated 6-8 million forest dwellers (predominantly tribal women) as suppliers. During the collection season (May-June for sal seeds, June-August for mango kernels), these women would gather seeds from forest floors, dry them, and sell them to Manorama’s collection agents at prices typically higher than what middlemen offered.

The next generation takes the helm

Janakilal Agarwal passed the torch to the next generation, and the company’s transformation from a trading operation to a sophisticated manufacturing enterprise would be led by his grandson Ashish Saraf and his wife Vinita.

Ashish Saraf, who has over 30 years of experience in the specialty fats sector, joined the family business and brought modern management practices while retaining the core relationships with tribal communities that his grandfather had built. In 2005, the family formally incorporated Manorama Industries Limited, signaling a new chapter of growth and professionalization.

Vinita Saraf, a commerce graduate from Mount Carmel College, Bangalore, joined her husband in building the business. Her entrepreneurial drive and operational focus complemented Ashish’s expertise in procurement and product development. Together, they transformed what had been a family trading business into a vertically integrated specialty fats manufacturer with global reach.

Going public: the 2018 IPO

By 2018, Manorama had established itself as a leading supplier of cocoa butter equivalents in India, with long-term contracts with global confectionery and cosmetics giants. The company decided to access capital markets, filing for an IPO on the BSE SME platform.

The October 2018 IPO raised ₹64 crore by issuing shares at ₹188 each. The primary use of funds: building a greenfield integrated manufacturing facility in Birkoni, Chhattisgarh, that would dramatically expand production capacity. Until then, Manorama had been heavily focused on procurement and primary processing, but the new plant would allow them to produce finished specialty fats meeting the exacting specifications of global food companies.

The IPO prospectus revealed the company’s customer list, a who’s who of global consumer goods giants. Ferrero, the maker of Ferrero Rocher and Nutella. L’Oréal, the cosmetics behemoth. The Body Shop, which used Manorama’s mango butter in its popular Mango Body Butter line. These relationships, built over decades, provided revenue stability and growth visibility.

Building the Birkoni plant

The Birkoni plant, commissioned in 2019-2020, represented Manorama’s transformation from a trading company to a full-fledged manufacturer. Located near Raipur in Chhattisgarh, the facility could process sal seeds and mango kernels into refined specialty fats, fractionated butters, and customized fat blends tailored to specific customer requirements.

The timing was challenging. Just as the plant was ramping up production, the COVID-19 pandemic struck. As Vinita Saraf noted in the company’s FY2021 annual report, the pandemic created “unprecedented challenges” in operations. Lockdowns disrupted both raw material collection (tribal communities couldn’t gather seeds as usual) and factory production.

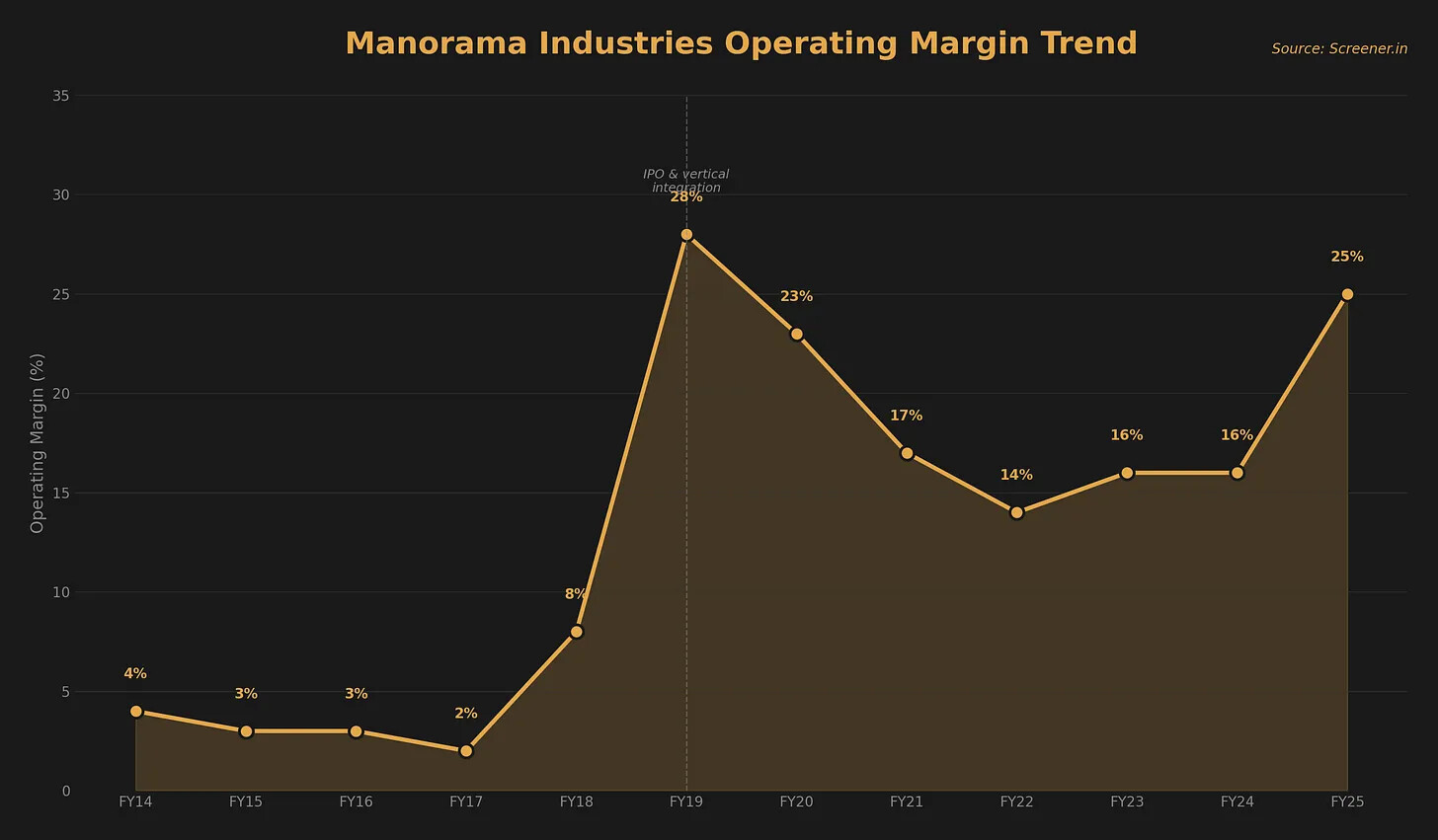

Yet the company persevered. By FY2022, the Birkoni plant was operating at fuller capacity, and Manorama was beginning to see the benefits of vertical integration. Margins improved as the company captured value previously flowing to third-party processors.

The African expansion

While building capacity in India, Manorama also looked outward. Shea nuts, another source of specialty fats widely used in cosmetics and chocolate, grow abundantly in West Africa’s “shea belt,” stretching from Senegal to Uganda. Unlike sal seeds, shea has a well-established global market, with European cosmetics companies sourcing shea butter for premium skincare products.

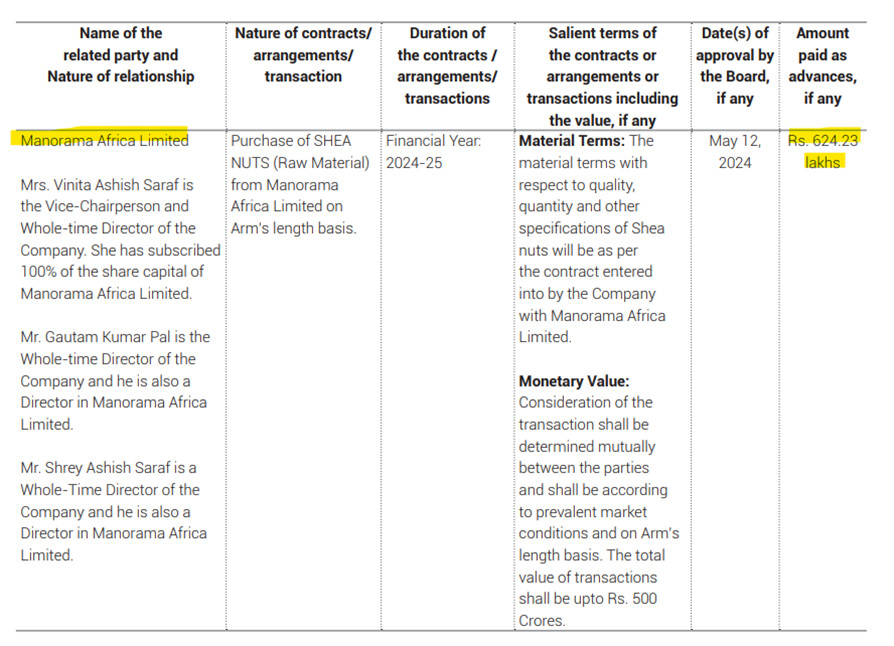

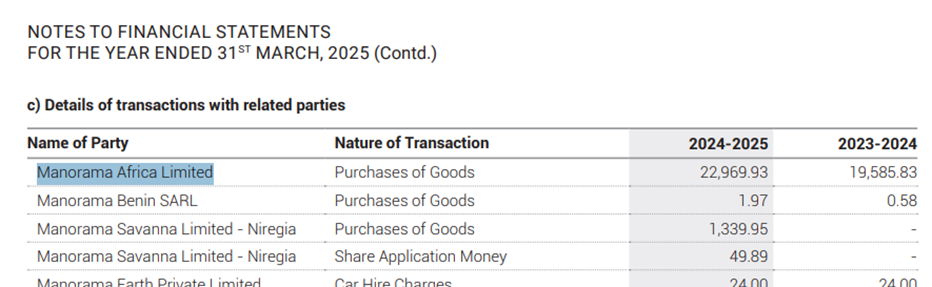

In 2017, Manorama established Manorama Africa Ltd, a subsidiary focused on sourcing and processing shea nuts from West African countries including Ghana, Burkina Faso, Nigeria, and Togo. The strategy mirrored what the company had done in India: build relationships with local communities (again, predominantly women who collect shea nuts), establish collection centers, and process the raw materials into high-value ingredients.

By 2024, Manorama had established wholly-owned subsidiaries across multiple West African countries: Manorama Savanna Nigeria, Manorama Savanna Togo, Manorama Savanna Ghana, and Manorama Savanna Burkina Faso. This sourcing network reduced dependence on Indian raw materials while tapping into a $300+ million global shea market.

Explosive growth: 2022-2025

The years 2022-2025 marked an inflection point for Manorama. Several factors converged:

Cocoa prices surged. Global cocoa prices hit multi-decade highs due to supply constraints in West Africa (climate change, aging trees, disease). This made cocoa butter equivalents, Manorama’s specialty - increasingly attractive to chocolate manufacturers looking to manage costs.

Capacity expansion completed. The Birkoni plant reached full operation, and in April 2024, Manorama commissioned an additional fractionation plant with 25,000 tonnes per annum capacity, bringing total fractionation capacity to 40,000 TPA.

Product mix improved. Manorama shifted from selling basic fats to higher-value customized products like MILCOA (their branded cocoa butter equivalent) and MilcoSpread (for spreads and fillings), commanding better margins.

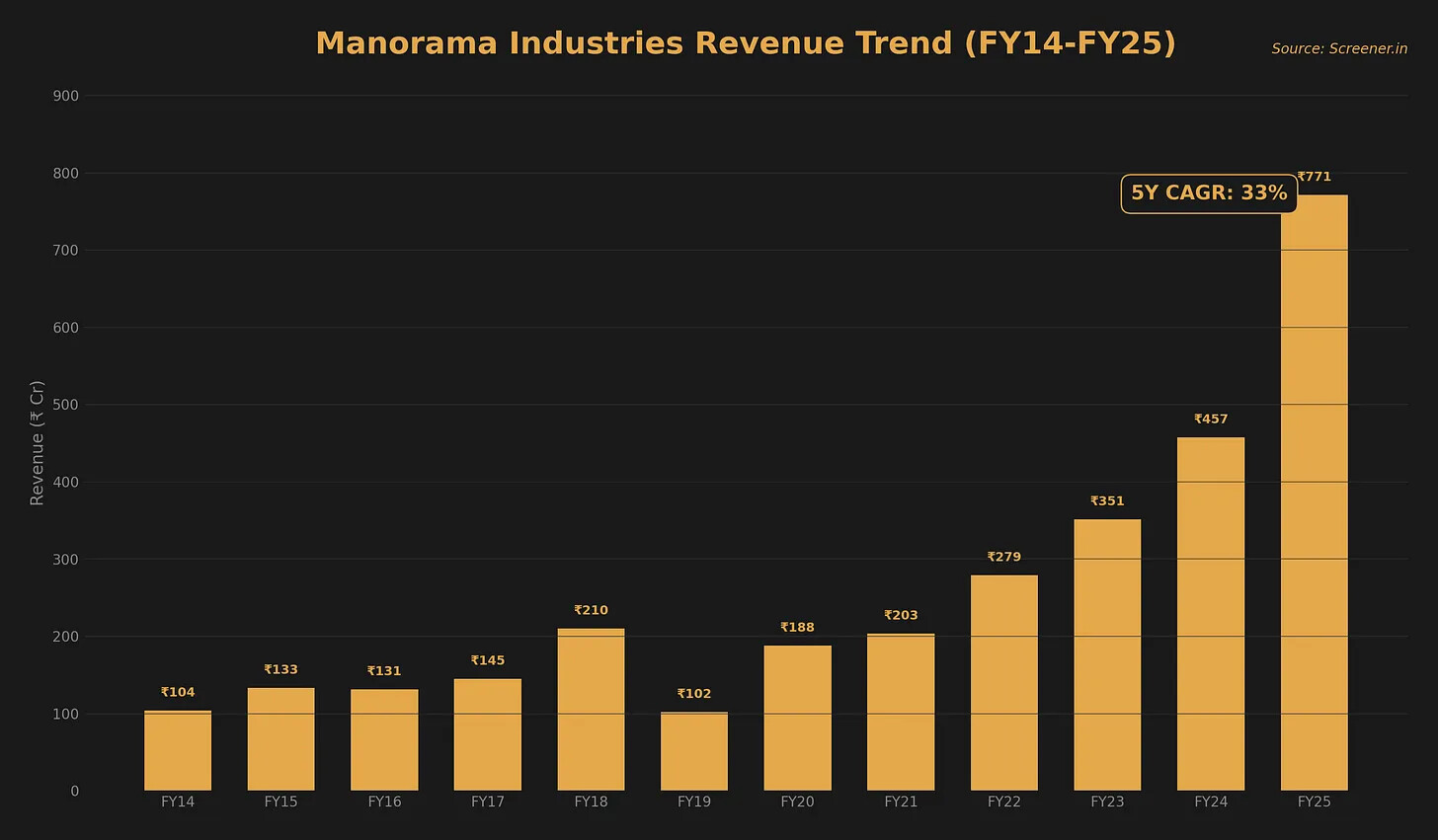

Revenue nearly tripled from FY2023 to FY2025. Profits exploded from ₹30 crore in FY2023 to ₹112 crore in FY2025, nearly a 4x increase. Operating margins, which had compressed during the capacity-building years, expanded back toward historical highs as scale benefits and premiumisation took hold.

The tribal connection: sustainability as strategy

Throughout its growth, Manorama has maintained its unique sourcing model. This model has become increasingly valuable as global consumers and corporations demand supply chain sustainability.

The company works with an estimated 100,000+ tribal collectors across Central India, predominantly women from Gond, Baiga, and other indigenous communities. During sal seed season, these women walk into the forests surrounding their villages, gather fallen seeds, dry them, and sell them to Manorama’s collection network. The company has established approximately 18,000 collection centers to facilitate this process.

The economics work for all parties. Tribal families earn income during the lean agricultural season (May-July), supplementing their farming income. Manorama gets reliable raw material supply at predictable costs. And the company’s products can be marketed as sustainably sourced, an increasingly important differentiator in pitching to multinational cosmetics and food companies with ESG commitments.

In 2017, Manorama signed a Memorandum of Understanding with the Chhattisgarh government to formalize its tribal engagement, and the company has won multiple awards for fair trade and sustainable sourcing practices. The company is a member of the UN Global Compact, aligning its operations with global sustainability development goals.

INDUSTRY CONTEXT

The specialty fats industry exists because of a fundamental tension in the chocolate world. Cocoa butter, the fat that gives chocolate its silky texture and snap, is expensive, volatile in supply, and difficult to source sustainably. For decades, confectioners and cosmetic manufacturers searched for alternatives that could replicate cocoa butter’s unique properties: a melting point just below human body temperature, solid at room temperature but liquid in the mouth, and stable during storage. The answer came from an unlikely source: seeds that fall from trees in Indian forests, collected by tribal women for generations as a supplementary source of income.

Cocoa Butter Equivalents (CBE) emerged as a distinct product category when European chocolate regulations in 2000 permitted up to 5% vegetable fats other than cocoa butter in chocolate products. This regulatory shift transformed what had been a niche product into a legitimate industry. CBEs are specialty fats engineered to match cocoa butter’s triglyceride profile, allowing chocolate manufacturers to reduce costs while maintaining product quality. The key to CBE production lies in the fatty acid composition, specifically the symmetric triglycerides POS, SOS, and POP (palmitic-oleic-stearic, stearic-oleic-stearic, and palmitic-oleic-palmitic), which give cocoa butter its distinctive crystallization behavior.

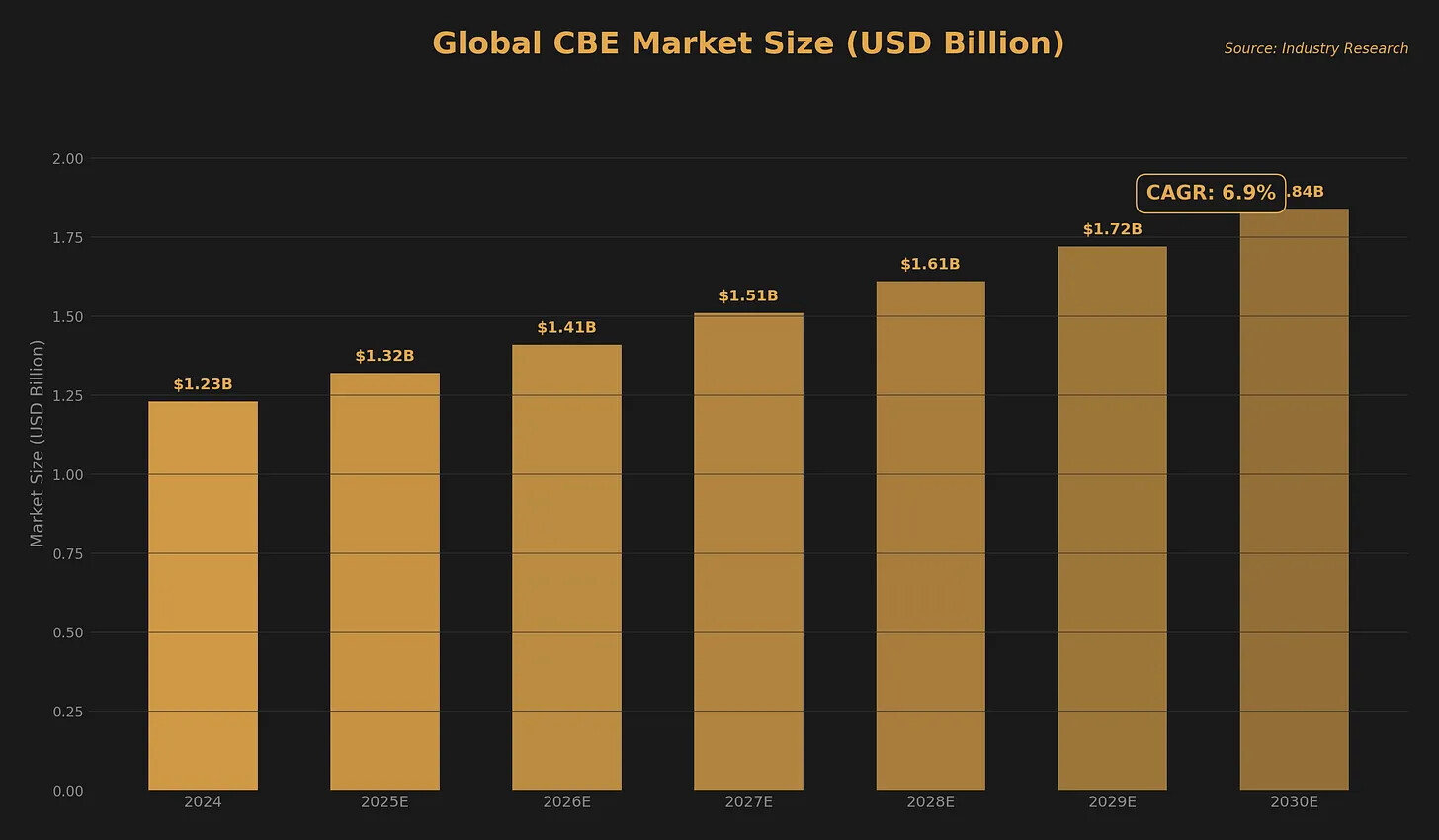

The global CBE market was valued at approximately USD 1.23 billion in 2024 and is projected to grow at a CAGR of 6.9%, reaching USD 1.84 billion by 2030. The broader specialty fats and oils market, which includes CBEs alongside other functional fats for bakery, dairy, and cosmetic applications, reached USD 14.12 billion in 2023 and is expected to grow at 7.4% CAGR through 2030. Within this landscape, the Asia-Pacific region, particularly India, has emerged as both a major production hub and a rapidly growing consumption market.

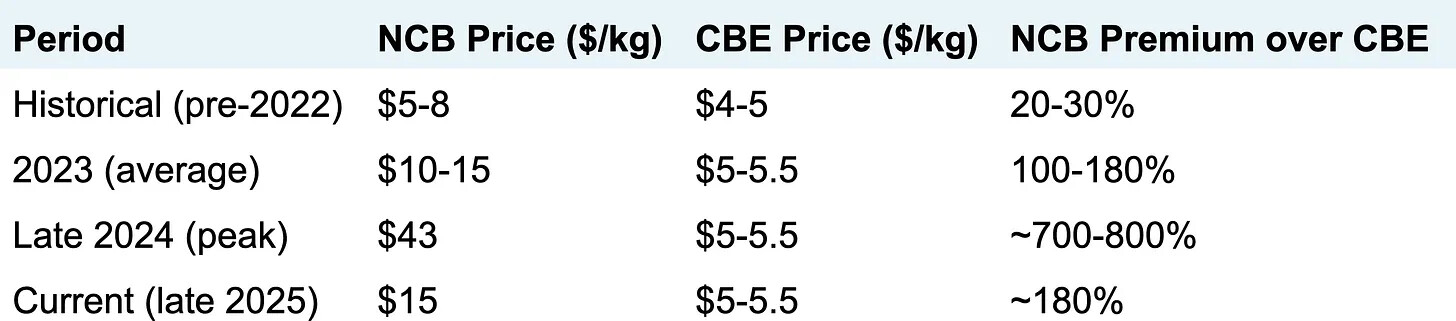

The NCB-CBE Price Gap: A Structural Tailwind

The relationship between Natural Cocoa Butter (NCB) prices and CBE prices is the single most important industry dynamic driving Manorama’s growth. Historically, NCB prices traded at a modest 20-30% premium to CBE prices. However, this relationship has become dramatically more volatile:

Major cocoa-producing countries in West Africa, mainly Côte d’Ivoire and Ghana (accounting for about 70% of global cocoa production), suffered 11-14% production declines. The causes: Cocoa Swollen Shoot Virus, climate impacts, and aging tree stocks. Even after partial price corrections, NCB remains 2-3x the price of CBE, making substitution economically compelling for chocolate manufacturers operating within the EU’s 5% CBE allowance.

While CBE offers cost savings and stability for mass-market products, natural cocoa butter remains essential for the rich, nuanced flavor in gourmet and premium chocolates. This creates a stable bifurcation: premium chocolate uses 100% cocoa butter as a selling point, while mass-market and industrial chocolate maximizes CBE usage within regulatory limits.

What makes India’s position in this industry unique is the availability of raw materials that cannot be cultivated. They must be collected from the wild. Sal trees (Shorea robusta) cover approximately 14% of India’s forest area, concentrated in Chhattisgarh, Jharkhand, Odisha, Madhya Pradesh, and West Bengal. The seeds, which fall from these trees during monsoon season, were traditionally collected by tribal communities for centuries but held little commercial value beyond local oil production. Similarly, mango kernels (the seeds inside mango pits) were considered agricultural waste until specialty fat manufacturers recognized their potential.

The chemistry is what matters. Sal fat contains 40-47% stearic acid and specific triglyceride profiles that, when refined and fractionated, produce a fat with crystallization properties remarkably similar to cocoa butter. Mango butter shares these characteristics. Shea butter from West Africa completes the trinity of raw materials used for CBE production, though shea’s supply chains have been more developed due to longer European engagement with African sources.

India’s tribal belt spanning central and eastern states hosts an estimated 6-8.5 million forest dwellers who participate in Minor Forest Produce (MFP) collection. This collection network operates through roughly 18,000 villages with established aggregation points, creating an informal but extensive supply chain. The government’s Minimum Support Price (MSP) scheme for MFP, including sal seeds, has provided price floors that support collector incomes while ensuring supply security for processors.

The regulatory environment shapes market structure significantly. The European Union’s Chocolate Directive (2000/36/EC) permits vegetable fats up to 5% in chocolate products, creating the primary end market for CBEs.

However, regulations require clear labeling when CBEs are used, and pure chocolate producers often market “100% cocoa butter” as a premium distinction. In India, FSSAI regulations govern food-grade specialty fats, while the cosmetic-grade market follows separate quality standards. The specialty fats industry benefits from government initiatives promoting agro-processing and export-oriented manufacturing, with Manorama holding “Star Export House” status.

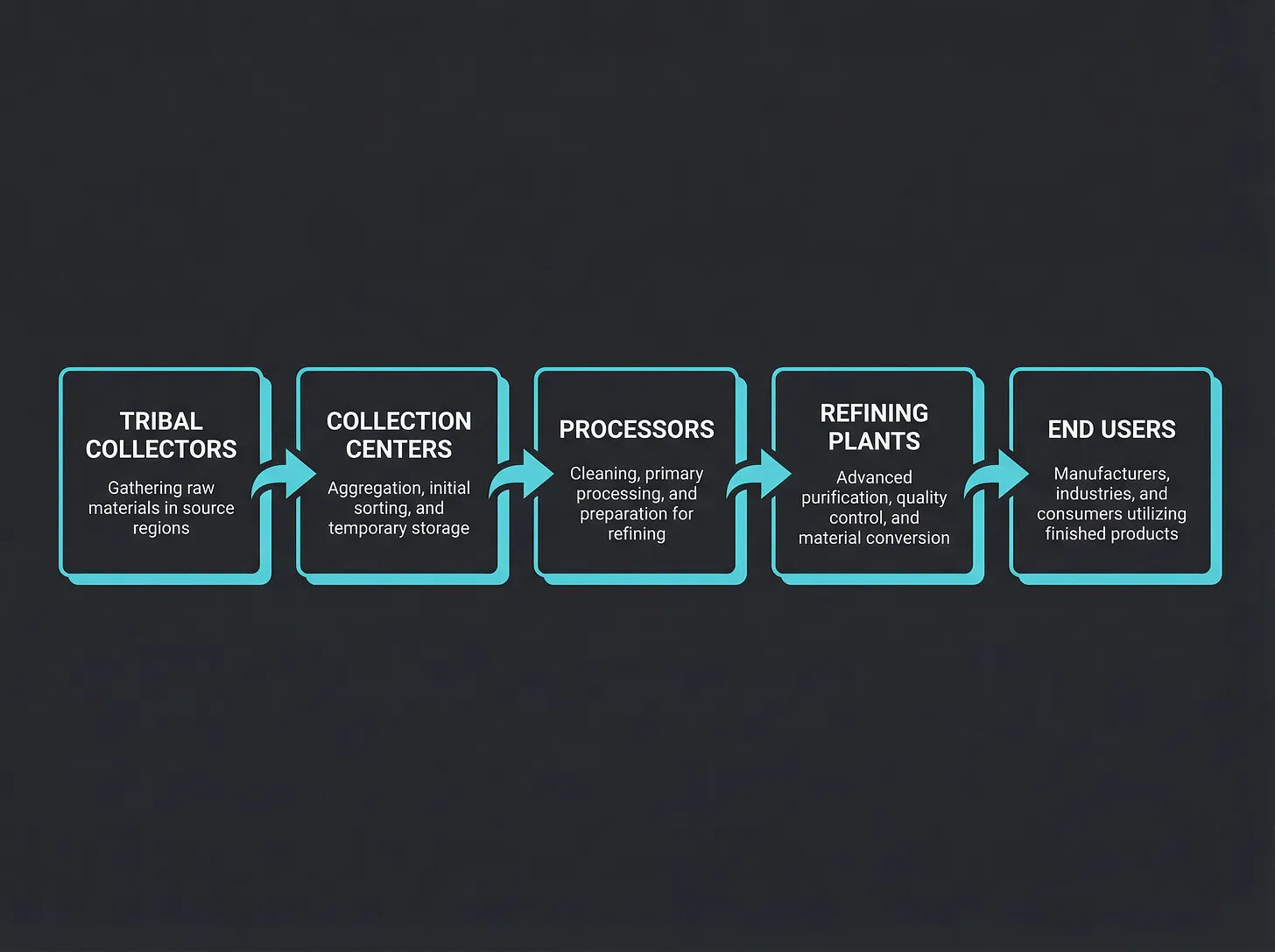

CBE Value Chain Flowchart

Climate and seasonality create operational challenges. Sal seeds have a concentrated harvest window of approximately 60-90 days during and after monsoon season, requiring processors to build significant inventory to maintain year-round production. Storage of oilseeds without quality degradation demands controlled environments and working capital. Mango kernel collection follows different seasonality, coinciding with the summer mango processing season, allowing some diversification in procurement timing.

The industry’s tailwinds are compelling. Global chocolate confectionery consumption continues rising, particularly in emerging markets where per-capita chocolate consumption remains a fraction of European levels. India’s chocolate market, though small by global standards, has grown at double-digit rates as urbanization increases and Western consumption patterns spread. Rising cocoa butter prices (driven by supply constraints from West African political instability, climate change impacts on cocoa yields, and growing demand) make CBEs increasingly attractive to cost-conscious manufacturers. CBE pricing typically runs at 50-60% of cocoa butter costs, offering meaningful savings for large-scale chocolate producers.

Headwinds include consumer preferences in premium chocolate segments for “pure” cocoa butter formulations, though this matters less in compound chocolate, coatings, and confectionery fillings where CBEs predominate. Sustainability scrutiny has intensified around palm oil-based specialty fats, creating differentiation opportunities for manufacturers using forest-sourced or certified sustainable inputs.

COMPETITIVE LANDSCAPE

Manorama’s Global Position

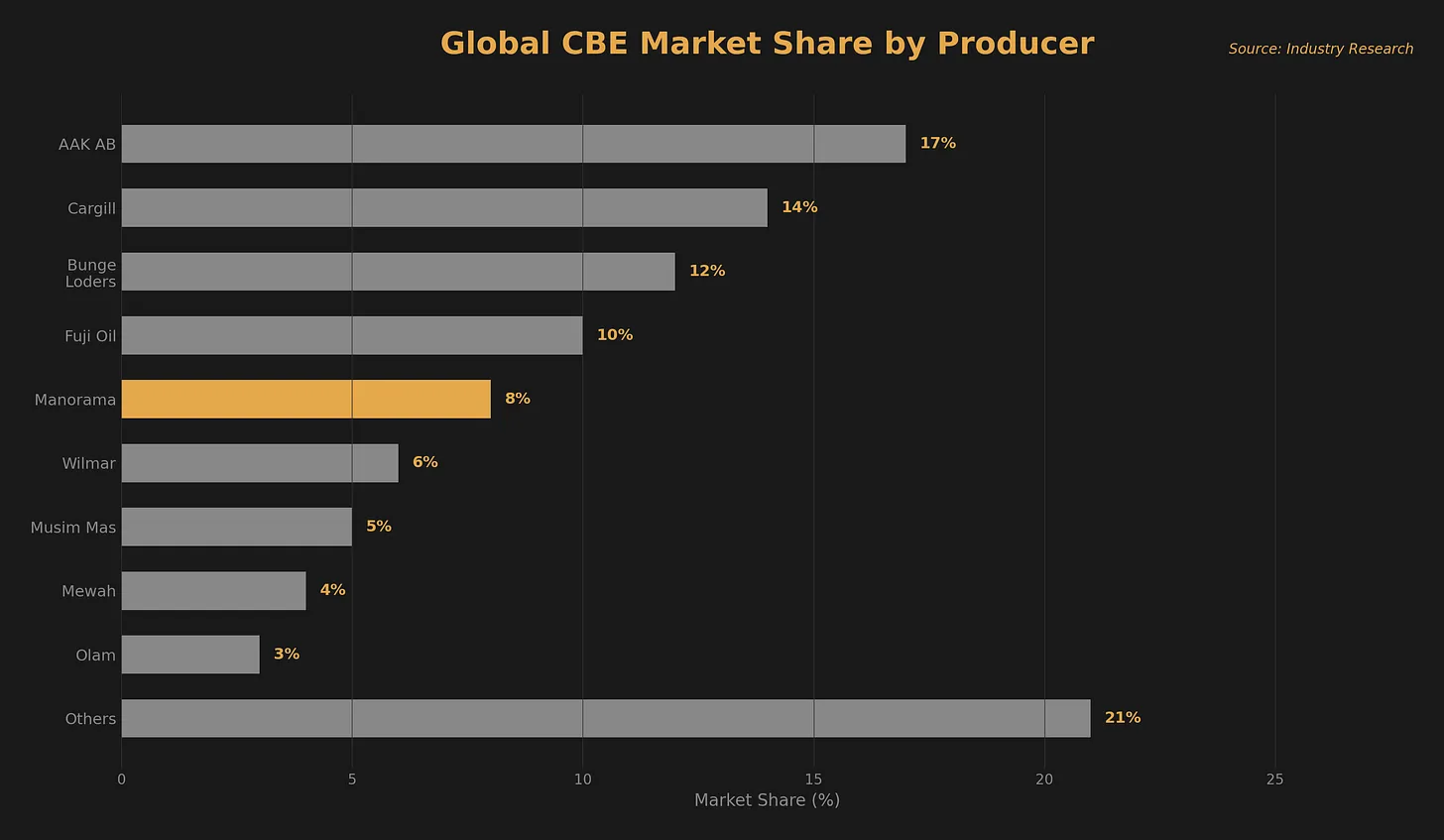

Manorama Industries is the only company globally to offer specialty oil/fat from a basket of exotic seeds (sal, mango, kokum, mahua, shea), and the largest in India to supply CBE to the world. The company is ranked among the top 3-4 global players in the Cocoa Butter Equivalents and exotic fats space, commanding approximately 8% of the global CBE market. This positioning makes Manorama a strategic supplier rather than a commodity producer. the company’s unique raw material access and processing capabilities have embedded it into the supply chains of Fortune 500 food and cosmetics companies.

The top 10 global CBE producers command approximately 80% of the market, making it a highly concentrated industry. Manorama’s position as a top-5 player globally, and the only significant Indian producer, provides both competitive insulation and strategic importance to customers seeking supply chain diversification.

The global specialty fats industry is dominated by a handful of multinational corporations that have built integrated supply chains spanning tropical regions. AAK AB, the Swedish-Danish specialty oils and fats company formed from the 2005 merger of Aarhus United and Karlshamns, stands as the industry leader with annual revenues exceeding EUR 4 billion. AAK operates refineries across Europe, the Americas, and Asia, maintaining direct sourcing relationships in West Africa for shea butter and Southeast Asia for palm-based inputs. Their strategy emphasizes customer co-development: working with chocolate manufacturers to create customized fat solutions rather than selling commoditized products. AAK India, with manufacturing facilities and a presence across 25+ states, represents their regional platform.

Bunge Loders Croklaan, part of Bunge Limited’s global oilseed processing network, competes directly in the CBE segment with manufacturing facilities in the Netherlands, Malaysia, and the United States. Their advantage lies in integration with Bunge’s crushing and refining infrastructure, providing cost advantages in palm kernel oil processing. The company has invested heavily in sustainability certification and traceability systems, responding to European customer demands.

Fuji Oil Holdings, the Japanese specialty fats producer, brings strong technical capabilities in fat modification and crystallization science. Their CBS (cocoa butter substitutes) and CBE products serve major Asian chocolate manufacturers, and the company has expanded globally through acquisitions including Blommer Chocolate Company in 2019 (though subsequently divested in 2022). Fuji Oil’s strength lies in formulation expertise for compound chocolate and confectionery coatings rather than pure CBE production.

Wilmar International, the Singapore-based agricultural commodities group, maintains the largest palm oil plantation and processing operations globally. While CBE represents a small portion of their portfolio, Wilmar’s scale in palm kernel oil provides cost advantages in CBS production. Their challenge in the Indian market lies in competing with forest-sourced alternatives that carry sustainability narratives palm oil cannot match.

Olam Food Ingredients operates cocoa and specialty fats businesses with particular strength in African sourcing networks. Cargill’s cocoa and chocolate business includes specialty fats operations, though the company has been more selective in this segment compared to their core commodities trading.

Within this global landscape, Manorama Industries occupies a distinctive position as the only significant processor globally using sal and mango-based raw materials. The company’s origins trace to the 1950s when founder Janakilal Agarwal began a seed-crushing operation in Raipur, Chhattisgarh. What began as a local oil producer transformed when Agarwal pursued fat chemistry studies in London during the 1960s, returning with knowledge of triglyceride modification and European market requirements. The breakthrough came through persistence and product development. They demonstrated to Ferrero in the 1990s that Indian sal-based fats could enhance chocolate stability in tropical climates, leading to a partnership that continues today.

Manorama’s competitive moat derives from supply chain control rather than manufacturing sophistication. The company’s network of 18,000 collection centers across tribal areas represents decades of relationship building that would be nearly impossible to replicate. These aren’t commercial arrangements that can be renegotiated. They’re embedded community relationships where Manorama representatives have become trusted aggregators for forest produce. The company employs over 6 million forest dwellers in its collection network, predominantly tribal women who supplement agricultural income through seasonal seed gathering.

The global CBE market has three tiers of competitors. Tier 1 comprises the multinationals (AAK, Bunge Loders Croklaan) with integrated global supply chains, multiple raw material sources, and extensive customer relationships. These companies can blend shea, palm kernel, and illipe-based fats to optimize cost and supply security. Tier 2 includes focused regional players and diversified commodity companies like Wilmar and Olam that participate opportunistically. Tier 3 encompasses specialized producers like Manorama that compete on unique raw materials and niche positioning.

What competitors say about this space is revealing. AAK’s India operations explicitly market sal-based fats as part of their sustainable sourcing narrative, highlighting work with women farmers. This validation from the industry leader confirms the raw material’s viability while intensifying competition in Manorama’s home market. However, AAK’s sal sourcing scale appears modest compared to their global shea and palm kernel volumes. It’s a product line rather than a strategic focus.

Manufacturing specialty fats requires fractionation and refining equipment costing tens of crores, along with quality systems meeting food-grade and often customer-specific certifications. These capital requirements screen out small entrants. However, the larger barrier is raw material access. New entrants cannot simply enter tribal areas and begin purchasing seeds. The collection network requires years of community engagement, government permissions for MFP trading, and established aggregation infrastructure.

Manorama’s expansion strategy addresses both capacity and geographic diversification. The company commissioned a new fractionation plant in Raipur in 2024, increasing total capacity to 40,000 tonnes per annum. The company has also established subsidiaries in West Africa (for shea sourcing) and the UAE (for trading), signaling ambitions beyond India-centric operations. This geographic expansion hedges raw material risk while accessing shea supplies closer to source.

Manorama supplies major global brands including Ferrero, Mondelez, and Nestlé in confectionery, plus L’Oréal and The Body Shop in cosmetics. The long-term supply agreement with The Body Shop for mango butter, announced in 2023, demonstrates the company’s value in sustainable sourcing narratives that premium cosmetic brands seek. These relationships have been built over decades (Ferrero’s partnership dates to the 1990s) and represent switching costs that protect Manorama’s position.

Competition in India’s specialty fats market has intensified as domestic chocolate consumption grows. AAK India, with modern facilities and global parent company support, represents the most capable domestic competitor. However, the market appears to accommodate multiple players given distinct raw material bases and customer segments. Manorama’s focus on sal and mango-based products doesn’t directly compete with palm-based CBS manufacturers serving different quality tiers and applications.

Proximity Advantage Over European Competitors

A critical but underappreciated competitive advantage is Manorama’s geographic proximity to raw material sources. European and American CBE manufacturers (AAK in Sweden, Bunge Loders in Netherlands, Cargill in the USA) are located far from both the Indian tribal forests that produce sal and mango kernels and the West African shea belt. This distance translates into higher logistics costs, longer supply chain lead times, and reduced ability to manage raw material quality from source.

Manorama’s facilities in Chhattisgarh sit within the heart of India’s sal seed production zone, while the company’s African subsidiaries operate directly in shea-producing countries. This dual positioning enables procurement cost advantages that European competitors cannot replicate even with superior manufacturing scale. Notably, even competitors like AAK, Mewah, Olam, and Cargill purchase CBE and stearin from Manorama due to the company’s cost effectiveness and unique product specifications. This is a remarkable validation of Manorama’s competitive position.

The competitive landscape appears set for consolidation and vertical integration. Global players will likely seek to secure raw material access in India, potentially through partnerships or acquisitions. Manorama’s scale and relationships make it an attractive partner or target, while its family ownership and community relationships complicate any transaction. The company’s listing in 2018 provided growth capital while maintaining promoter control at approximately 54%, suggesting the founding family intends to pursue independent growth rather than sale.

HOW THE BUSINESS ACTUALLY WORKS

Understanding Manorama requires tracing money through the system, from forest floor to Ferrero Rocher. The elegance lies in transforming near-zero-value raw materials into premium specialty fats through a series of value-adding steps, each protected by distinct competitive advantages.

Step 1: Collection Network Activation (The Foundation)

When sal trees flower and fruit during monsoon season (June-August), seeds fall to the forest floor across central India’s tribal belt. Manorama’s collection infrastructure activates through a three-tier pyramid: village-level collectors (predominantly women from scheduled tribes), local aggregators who consolidate from multiple villages, and regional collection centers with basic storage and transport.

The economics here matter. Tribal collectors earn ₹10-25 per kg of sal seeds gathered. This supplementary income often exceeds their agricultural earnings during collection season. Manorama’s aggregators typically pay ₹30-50/kg depending on quality and moisture content. Government Minimum Support Price for sal seeds (under the MFP scheme) provides a floor price, protecting both collectors and processors from market volatility.

This network wasn’t built overnight. Ashish Saraf and his predecessors spent decades establishing trust in tribal communities, often providing advance payments during harvest season when families need cash most. These relationships cannot be replicated through capital expenditure. They require cultural understanding, local language capability, and generational continuity. The company leverages a long-standing network of over 1,000 tribal collectors, self-help groups (SHGs), and forest communities, which it has nurtured over decades.

Raw Material Supply Security

The scale of natural production significantly exceeds Manorama’s procurement needs, providing headroom for continued growth:

Sal seeds contain 13-14% butter content and are collected primarily during the May to July season. Shea nuts have a significantly higher butter content of 45-50% and contain symmetrical triglycerides, making them a critical raw material for CBE formulation after fractionation.

Step 2: Seed Processing to Crude Fat

Seeds arrive at Manorama’s facilities in Raipur with varying moisture content and quality. Initial processing involves:

1. Cleaning and grading: Removing foreign matter, sorting by quality

2. Drying: Reducing moisture to prevent degradation during storage

3. Dehulling/Decortication: Separating the oil-bearing kernel from outer shell

4. Oil extraction: Using mechanical pressing (expeller) followed by solvent extraction to maximize yield

Sal kernels yield approximately 35-42% fat content, while mango kernels yield 10-15%. This extraction step is relatively commoditized, the equipment and processes are standard in the oilseed industry. Manorama’s advantage here lies in consistent raw material supply rather than processing superiority.

The crude fat at this stage has limited value, it contains impurities, free fatty acids, and compounds that affect color, odor, and stability. Selling crude fat would position Manorama as a commoditized raw material supplier, subject to price competition and margin compression.

Step 3: Refining, Bleaching, Deodorizing (RBD)

The RBD process transforms crude fat into a food-grade ingredient:

• Degumming and Neutralization: Removing phospholipids and free fatty acids through alkali treatment

• Bleaching: Using activated earth/clay to remove color pigments and oxidation products

• Deodorization: Steam distillation at high temperature and vacuum to remove volatile compounds that create off-flavors

This is where quality differentiation begins. Food-grade fats must meet strict specifications for free fatty acid content (typically <0.1%), color (measured on Lovibond scale), and peroxide value (indicating oxidation). Cosmetic-grade products face even tighter specifications. Manorama’s quality systems, certified to FSSC 22000 and multiple customer-specific audits, enable sales to premium customers who won’t accept substandard inputs.

Step 4: Fractionation (The Value Multiplier)

This is the critical step that transforms generic vegetable fat into Cocoa Butter Equivalent. Fractionation separates fat into components with different melting points through controlled crystallization:

1. Fat is melted and slowly cooled under precise temperature control

2. Higher-melting-point fractions (stearin) crystallize first

3. Liquid fraction (olein) is separated through filtration

4. Multiple passes produce narrow melting-point fractions matching cocoa butter specifications

The stearin fraction from sal fat (the hard component melting around 34-36°C) mimics cocoa butter’s behavior almost perfectly. This fraction commands premium pricing because it enables chocolate that snaps at room temperature but melts smoothly in the mouth. Stearin typically accounts for approximately 50% yield from exotic seeds like sal, shea, and mango, with the remaining 50% being olein (the liquid fraction).

Stearin: The Strategic Intermediate

Stearin serves a dual role in Manorama’s business model. It can be sold as a standalone product for applications in bakery shortenings, margarines, confectionery coatings, cosmetics (creams, soaps, candles), and industrial oleochemicals. However, its most valuable use is as the critical building block for CBE production, approximately 90% of Manorama’s stearin volumes are channeled into confectionery applications through CBE blending.

The company also produces enzymatic stearin, a premium variant that undergoes enzyme-based interesterification to achieve tailored melting profiles and higher functionality. Enzymatic stearin commands realizations up to 3.5x higher than base olein, underscoring its margin-accretive nature. This premium product represents Manorama’s move up the value chain from bulk specialty fats toward higher-margin, customized solutions.

The CBE production process blends stearin with Palm Mid-Fraction (PMF) to replicate the functional properties of natural cocoa butter. A typical CBE formulation requires 500-600 grams of stearin combined with 400-500 grams of PMF to produce 1 kg of CBE. This blending expertise (achieving specific triglyceride profiles that match customer specifications) represents accumulated know-how that differentiates Manorama from commodity fat processors.

Manorama’s fractionation capacity expansion from 15,000 TPA to 40,000 TPA represents the company’s strategic bet. Each additional tonne of fractionation capacity enables converting lower-value crude fat into higher-value CBE. The 25,000 TPA brownfield expansion commissioned in July 2024 cost approximately ₹80-100 crores, capital deployed specifically to capture value-added production. The expanded capacity reached 70% utilization by Q1 FY26, demonstrating strong demand pull from global customers.

Step 5: Product Customization and Customer Co-Development

Major chocolate manufacturers don’t buy generic CBE, they specify exact triglyceride profiles matching their chocolate formulations. Ferrero’s requirements for a Ferrero Rocher hazelnut-chocolate shell differ from Mondelez’s specifications for a Dairy Milk coating.

Manorama’s R&D team (led by founders with decades of fat chemistry expertise) works with customer technical teams to develop:

• Specific melting point ranges (±0.5°C tolerance)

• Triglyceride composition matching customer specifications

• Compatibility testing with customers’ cocoa butter sources

• Shelf stability validation under various storage conditions

This co-development creates switching costs. Once a customer’s production line is calibrated for Manorama’s CBE specifications, changing suppliers requires reformulation and revalidation. That’s a 6-12 month process that production managers avoid unless necessary.

Revenue Recognition and Cash Flow Timing

Understanding seasonality is critical:

• Q2 (July-September): Peak sal seed collection. High working capital deployment for inventory build

• Q3-Q4 (October-March): Production and delivery ramp. Revenue recognition accelerates

• Q1 (April-June): Lower sal collection. Mango kernel season begins. Capacity for shea processing

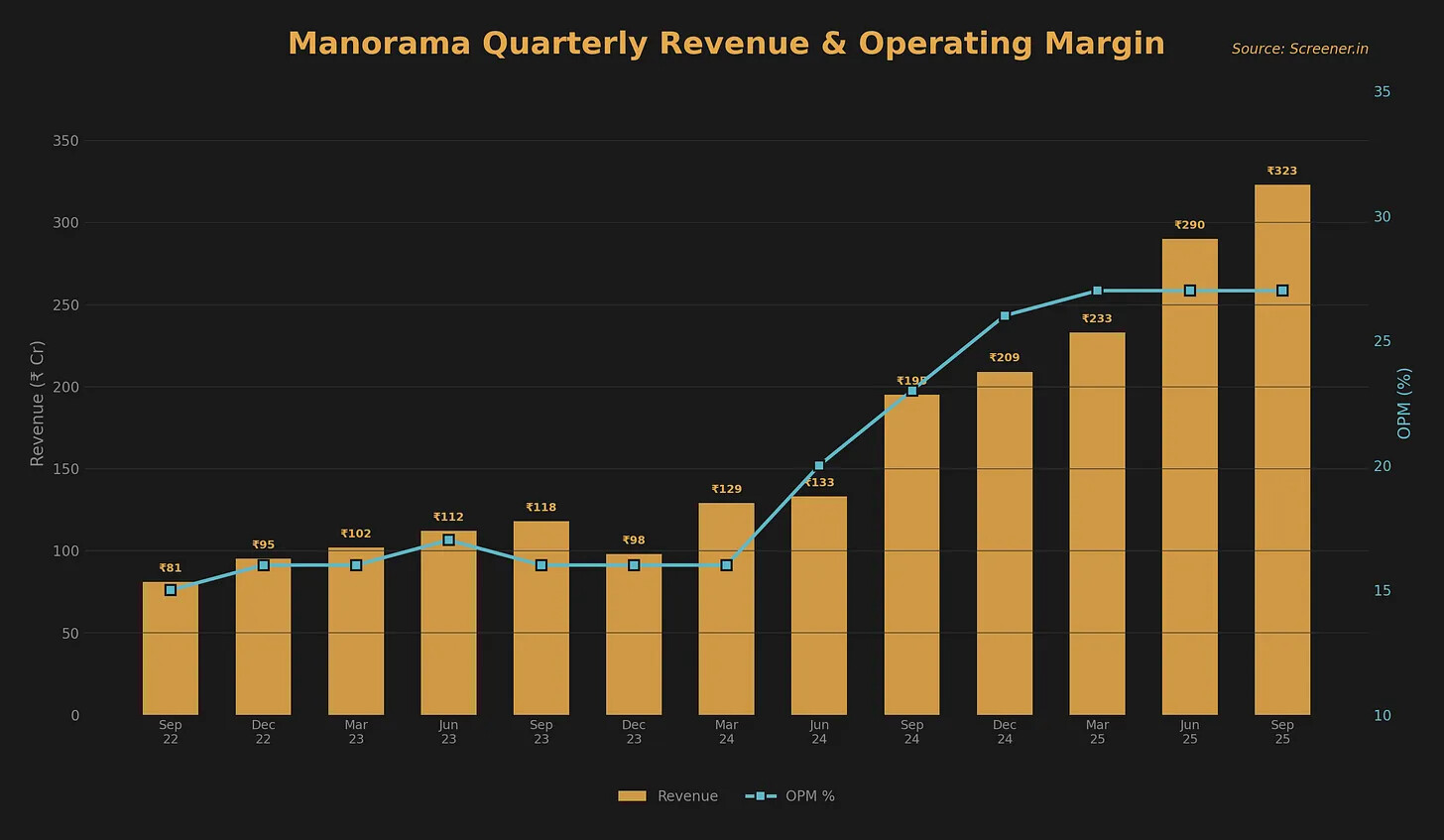

This seasonality creates cash conversion cycle patterns where working capital peaks in Q2, converts to receivables in Q3-Q4, and cash collection catches up by Q4/Q1. Investors watching quarterly results should expect margin variations tied to production timing rather than business deterioration.

UNIT ECONOMICS: WHY THIS BUSINESS PRINTS MONEY

The economic logic of Manorama’s business becomes clear when examining margins at each stage and the structural advantages driving profitability.

The Zero-Waste Production Model

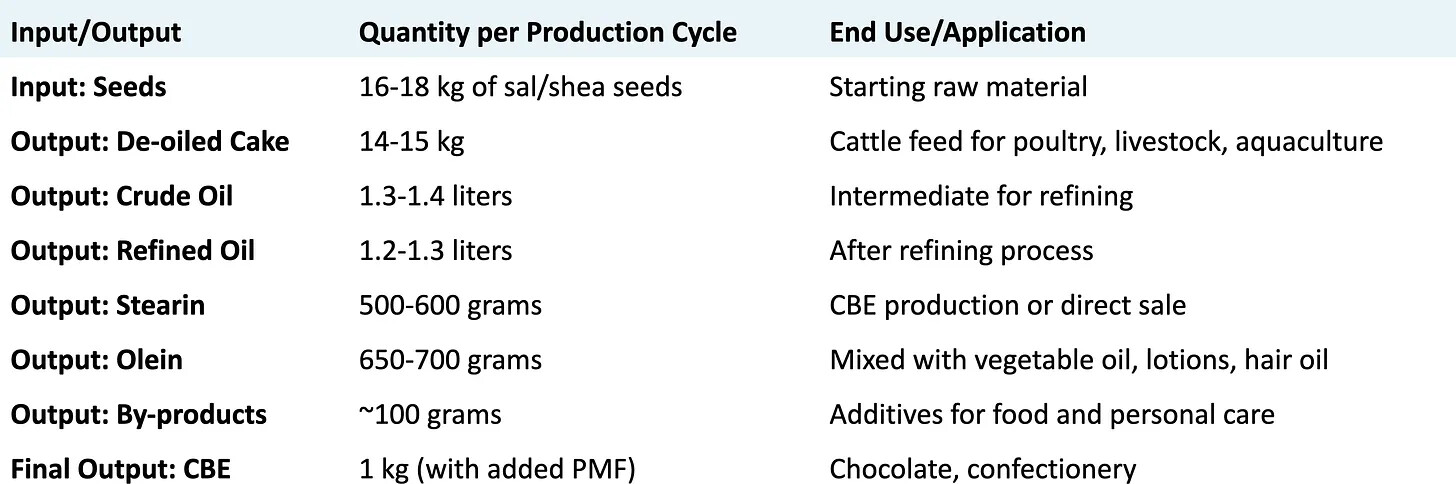

Manorama operates a fully sustainable, zero-waste production process where every fraction of raw material is commercially monetized. A typical production run illustrates this efficiency:

This zero-waste model provides multiple revenue streams from a single procurement cost. De-oiled cakes, refinery residues, and olein are all sold for various applications, enhancing the company’s ESG profile while extracting maximum economic value from each kilogram of seeds procured.

Raw Material Cost Advantage

The foundational advantage is raw material cost, forest-sourced seeds cost a fraction of alternatives:

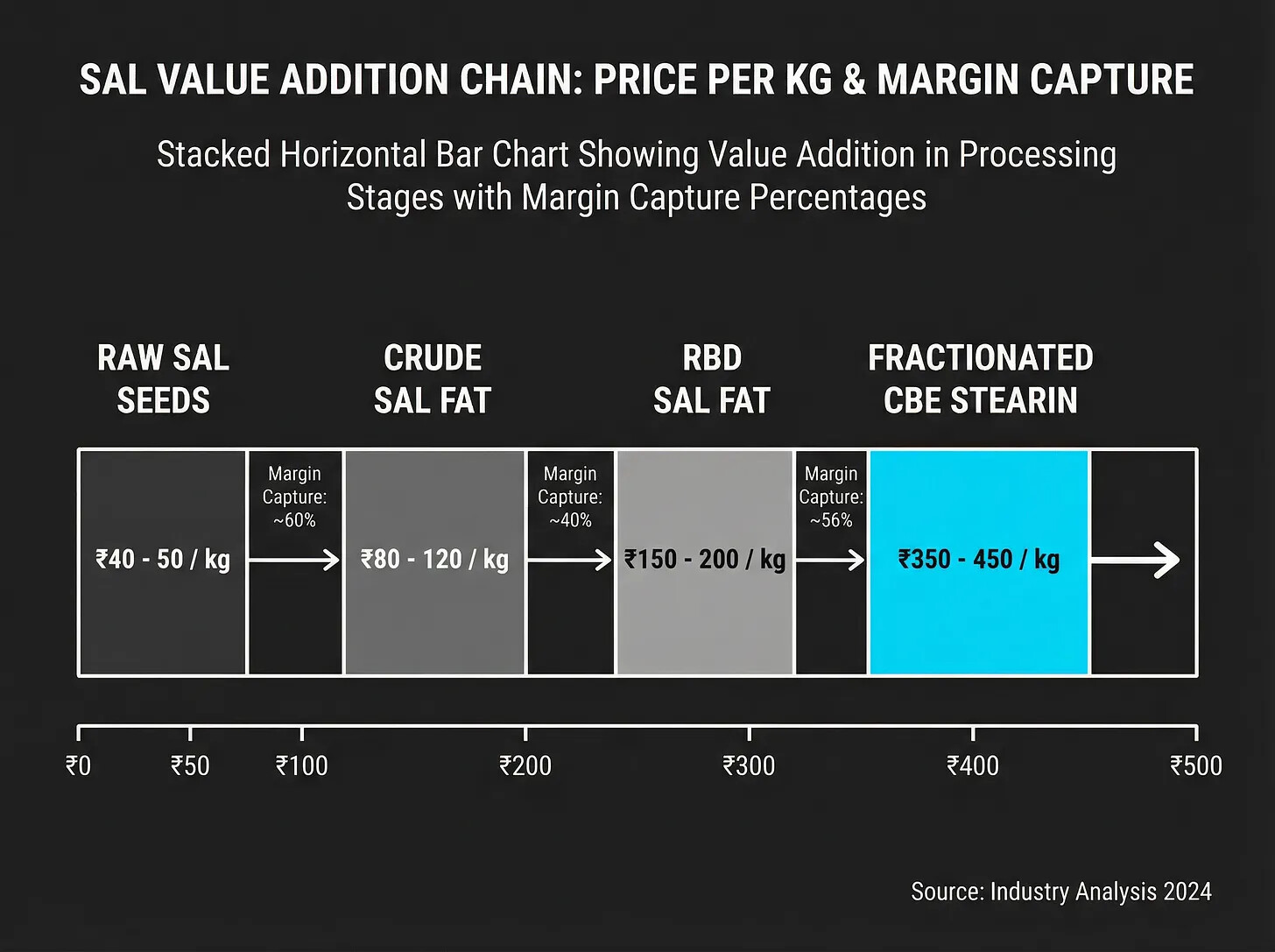

Even accounting for processing costs, CBE from forest seeds costs ₹350-500/kg versus cocoa butter at ₹1,500-3,000+/kg. This structural cost advantage persists regardless of market conditions, it’s embedded in the nature of raw materials.

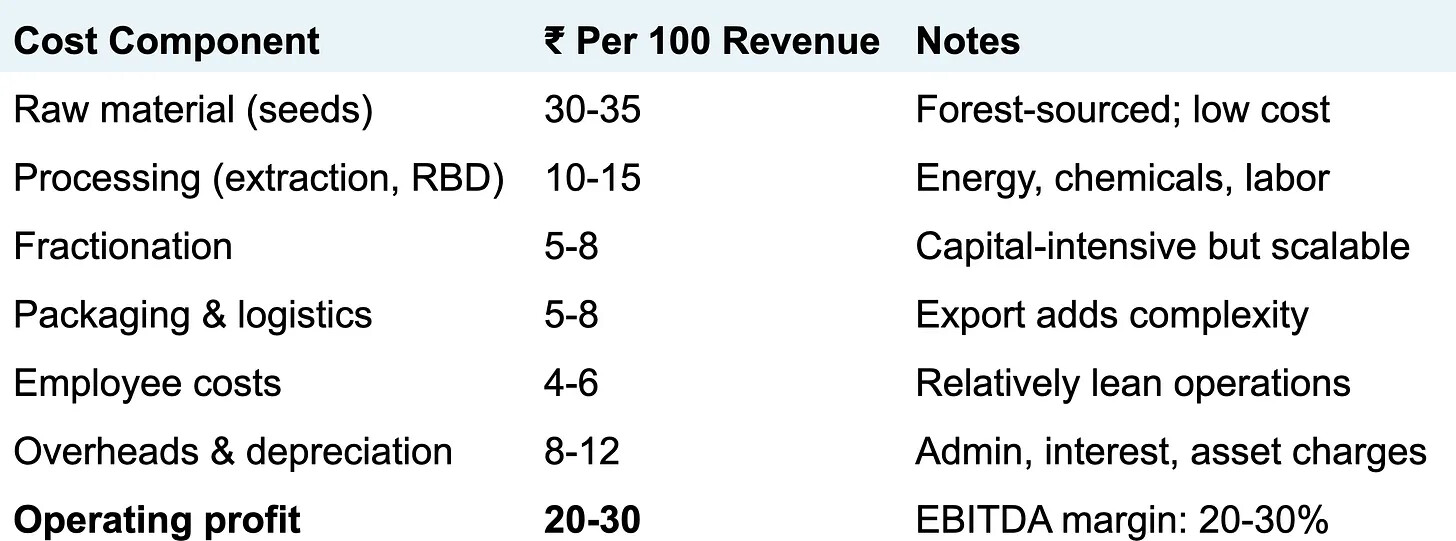

Processing Margin Breakdown

For every ₹100 of CBE revenue (selling at approximately ₹400/kg for premium fractionated product):

Disclaimer: I am not a registered analyst. I’m just a student trying to study different businesses/sectors. Don’t take my word for it; try to study the business independently. I might have positions in the securities discussed. (Last time i wrote a writeup this long, it didn’t end well for that company, so please don’t take my work as investment advice).

Will Try to cover growth triggers, risks and valuations in next part.