Haven’t been active on this thread since I joined a family office as an analyst, and due to some regulatory or disclosure requirements, I have tried posting less just to be on the safer side.

But this post is less from the perspective of stocks and more about the change in portfolio construction as a whole.

Over the last four months of the bull market (October to January), the IRR for my portfolio jumped through the roof as some of the concentrated bets resulted in my portfolio almost 2.5x-ing in four months (heights of craze, I guess). But now, I’m trying to come back to my old roots. What do I mean by that? I’ll explain in the next write-up.

I have always been an old follower of Utpal Sheth sir and have felt that the depth of his work and knowledge is not something that can be grasped in one go.

I started thinking about the framework of Terminal Value Investing + Adaptable Challengers.

So what do I mean by that?

A company with a business model that is inherently so different that it is very, very hard to replicate, even if you give away all its secrets and business takeaways.

If anybody had done the modeling of such businesses, they would have known that the less capital-intensive the back end of a business is, the higher its terminal value will be. That made me lean toward businesses with lower capital intensity as they scale, leading to unbeatable cumulative value creation. With less capital reinvested and idle cash flows accumulated, shareholder value keeps compounding.

And what does Adaptable Challengers mean? These businesses aren’t market leaders, but they have the agility to shift with trends, giving them a first-mover advantage.

But isn’t this what everybody is looking for? Quite possibly, yes.

So what makes you different from most other investors? Differentiated insights about the business. (Again, borrowing the wording from Utpal sir.)

What is the unique insight you have that makes you stick with a business?

For every buyer (you), there are multiple sellers—that’s how the market works. But what’s the insight that gives you the conviction to stand against the tide without flinching?

Quite honestly, this is where the alpha lies.

As Jeff Bezos says, “Your margin is my business opportunity.” I’d say, “Your disbelief or counter-thesis is my alpha.” The stronger the market’s skepticism, the higher the alpha potential.

Portfolio Construction Based on This Thought Process

Let’s dive into some of the thought processes behind my portfolio construction, based on all three learnings: Terminal Value Investing + Adaptable Challengers + Differentiated Insights.

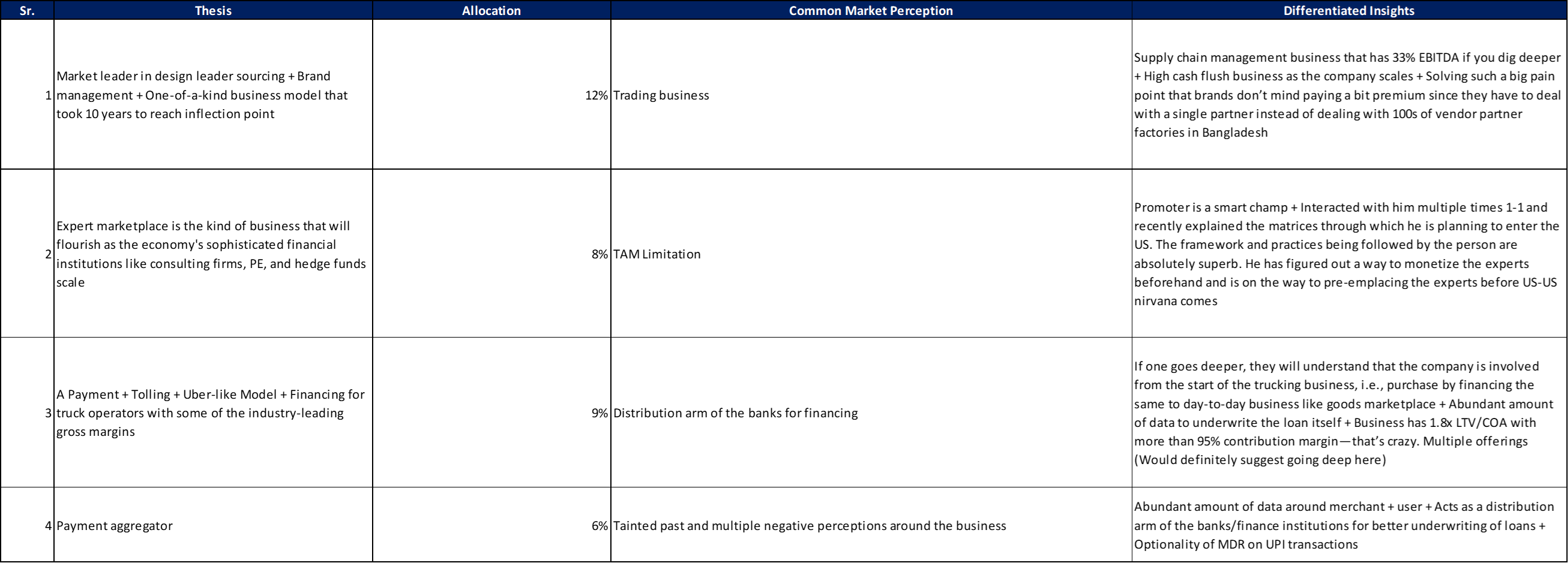

I have always been very intrigued by platform businesses (I own four in my portfolio and am planning to add a fifth). The dynamics of these businesses are different from traditional ones. Unlike manufacturing businesses, where demand is forecasted and supply is developed accordingly, platform businesses develop the supply side first.

For example, take Amazon.

If you were building an e-commerce giant in 1995 amid the tech boom, could you have predicted the total addressable market (TAM) that Amazon has today? Especially considering how much of it comes from AWS rather than e-commerce? Not really.

Even within e-commerce, Amazon started with books—not with a full-fledged product portfolio. Over time, it scaled up to more than 100K SKUs.

One major takeaway from studying such businesses: Supply-side strength is the moat for platform businesses. Building a strong portfolio of supply early on allows these businesses to achieve high Lifetime Value (LTV) to Customer Acquisition Cost (CAC) ratios.

For example, if a business acquires a customer for one service, but over five years sells them five different services, the customer’s lifetime value increases dramatically.

Hence, before onboarding customers, it’s crucial to build the supply side first. Early monetization of some part of this supply can also help cushion cash burn while developing other services.

Again, look at Amazon. While developing its e-commerce platform, it started with books—not a full-fledged product range. Slow monetization of this single category helped reduce cash burn for expanding into other services.

Financially, what makes platform businesses unique?

Most of their costs are fixed—employees, software development, UX/UI, data collection, data interpretation & monetization, and the cost of developing new offerings.

Because a large portion of costs are fixed, scaling becomes highly profitable over time. This aligns with the concept of high terminal value investing—low capital intensity leading to long-term scalability.

Adaptable Challengers: Agility in Market Cycles

This is more of a bottom-up approach, analyzing how a company adapts to changing cycles.

Some companies are able to pivot and capture new opportunities faster than others, giving them a significant edge. These companies don’t necessarily dominate their industry but thrive in shifting environments.

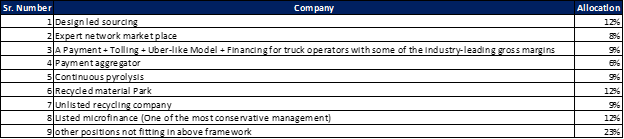

I’ve made such companies a big part of my portfolio—around 35-40% across four ideas—because they fit this framework perfectly.

Independent Theme: Recycling – A High Terminal Value Play for the Next 5-7 Years

Beyond platform businesses, I believe recycling is a long-term theme with strong potential.

Most recycling businesses are highly capital-intensive, with payback periods of 5-6 years and ROICs of 15-17%. That’s good—but not compelling enough for a high-quality framework.

I wasn’t willing to compromise on my framework until I found a company that fit perfectly.

This company has:

- A 3-4 year payback period instead of 5-6 years.

- A much lower capital requirement compared to competitors.

- A superior ROIC of 22-25% (not as high as platform businesses, but still great).

The competitive advantage? Its technology is developed by its parent firm and provided at cost.

Why This Got Me Excited

This company is in tyre recycling.

After evaluating multiple recycling sub-sectors, I found that only tyre recycling is economically viable, while many other recycling processes struggle because the price of recycled material is lower than virgin material.

India is full of batch pyrolysis tyre recycling plants, especially in the north. But batch pyrolysis is highly polluting. Continuous pyrolysis, on the other hand, is far more efficient and sustainable.

The Pollution Control Board (PCB) is now cracking down on batch pyrolysis plants, and I believe continuous pyrolysis will dominate going forward.

This company is ahead of the curve, positioning itself as a future leader in the space.

Portfolio Allocation

Though this is a recent buy, I’ve made a 9% allocation in my portfolio, believing that its current top line could become its bottom line in five years—a massive value creation opportunity.

Another Opprtunity here are Theme parks made with recycled materials with the Infinite ROCE and ROE and PBP from the 1st day in terms of capital and in terms of WC in 5-6 months (Still crazy and has the opportunity to do excute the same outside of India + multiple aveneus in terms of the Cross seling If the same materializes the TV can be at very end of the spectrum

Conclusion: Investing with a Long-Term, High-Terminal-Value Mindset

To sum it up, my focus is on:

- High Terminal Value – Businesses that scale with minimal reinvestment.

- Agility & Adaptability – Companies that can pivot quickly.

- Differentiated Insights – Finding overlooked opportunities where the market is wrong.

I am not chasing front-end returns but building a resilient, scalable, and high-quality portfolio that can generate sustainable wealth over time.

Final PF allocation:

Will try to move the allocations in the companies fitting the framework

Nothing discussed above is recomendation above note is just for my future references