Hello everyone,

I’m Mann, A CA Final Student who is currently working in Valuation Domain in a MNC

I’ve been actively Investing since completion of 10th Standard (5 Years now)

I’ve recently Joined Valuepickr

and I’ll Be sharing Here My Portfolio and thesis and Risks behind the same

All the Views are welcomed

I think Concentrated Portfolio is a way to go to enhance the return while you have high Risk taking capacity, Since I’m Quite Young (20YO). I think i have Quite a good amount of time and risk taking capacity.

Below is my Portfolio

| Name of the Company | Exposure |

|---|---|

| Creative Newtech Ltd | 27.61% |

| Brand Concepts Ltd | 14.75% |

| Cantabil Retail | 19.96% |

| SKP Bearings | 37.69% |

Thesis Behind all of the above

Creative Newtech – Brand Licensing Business nearest to contract Manufacturing opportunity in EMS Space

Creative Newtech holds Honeywell License to design, manufacture and sell the products of Honeywell, Where Honeywell Charges certain amount of Royalty Which is Minimum Guaranteed Royalty or Percentage of Sales Which Every is higher

Gross margin in Honeywell Business is very High (north of 40% gross and 15-20% EBITDA margins) current share of Honeywell products in total sales is near to 10% of overall Revenue

Management intends to Increase the share to 20-25% of revenue in Next 2 Years

Other Business contains of enterprise Business which is low Margin Business (almost Paper thin) but is Working capital less business, it involves back-to-back trading of electronic components

Ckart is their B2B Marketplace which isn’t yet commercialized but has helped them to make almost 400 crores of Revenue for Creative

They Inted to commercialize the same in medium term where Ckart will make transaction fees as income, Since the Matrix is Quite different for success of market place model, they would have to Fund the business Model, which can be in 2 Ways

- They Fund the same out of Creative newtech’s Bottom line up to 10% of Bottom Line

- Bring in the The Investor who has knowledge about market place business model and help them shape the Company

The Company has good hold under FMEG and FMCT Goods But the same is to be phased out since they don’t contribute very much to the business’s Revenue

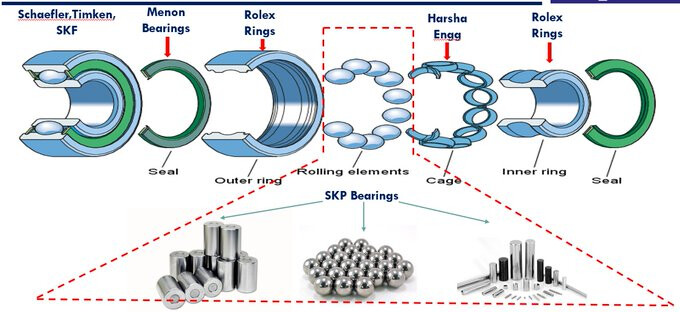

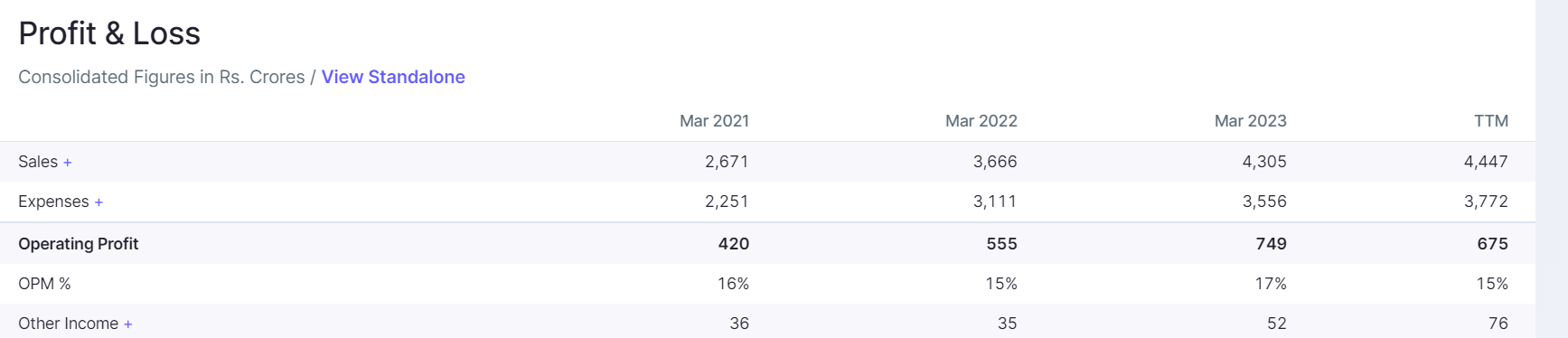

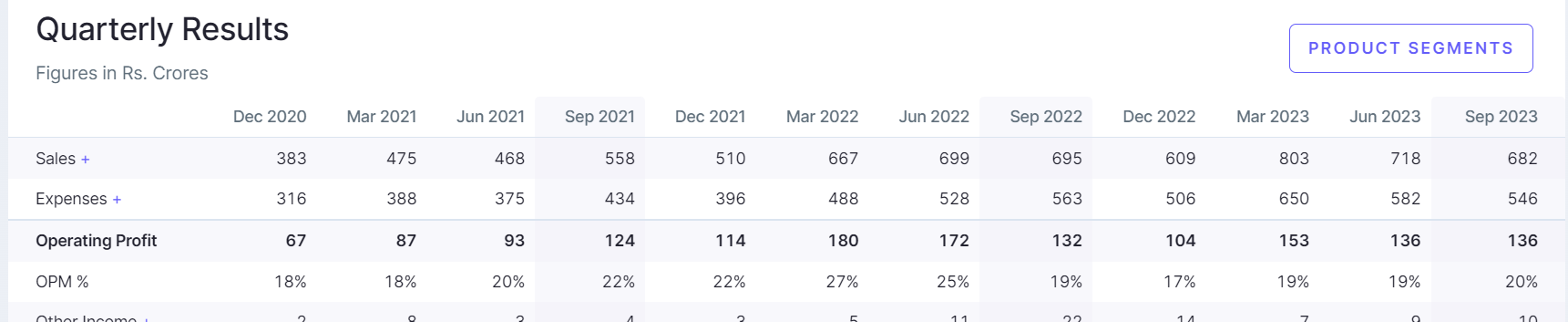

SKP Bearings –

SKP Bearings Ltd is a microcap company involved in manufacturing of Steel balls, Needle Rollers, Cyclical rollers and pin

The company’s Business dates back to 1991 which was established as a partnership firm, which eventually in January 07, 2022 got converted into limited company.

The promoter Mr. S.K. Palshikar is Engineer with a Masters from IIT Bombay. Prior to SKP he has also completed Rolling Bearing Theory from SKF College

Criticality of Bearings

Consider a car where a bearing of the wheel suddenly goes Belly up during the Ride, this can cause the accident and in order to prevent it Quality checks for OEMS are very Stringent so that they can assure that the Customer is safe and Secure And due to the above reason

the Bearings Are generally Purchased from the Reputed Companies with Proper Quality Control Audit and This Bearings manufactures integrates their value chain After considering very Strict Quality control Measure of another firm

The company Has 2 Segments –

Roller and Balls

Roller –

s High Margin Segment Which Gives Round to 40% EBITDA margin

The current Capacity is 1320 Tonnes P.a. at 92% Capacity Utilization Post Capex the Capacity will be 2400 Tones P.a.

The Rollers are very Much Customized as per the need of the OEM and Therefore the Margins in Rollers are Quite High

The share of Revenue of this Roller in FY 23 was 77% This is the reason of more than 35% EBITDA Margin of the company seems the rollers Accounts for more than 40% EBITDA

Balls-

Balls Segment Commands Less EBITDA margin in comparison to that of Rollers but the margin overall is more lucrative at 20%

The total capacity utilization of the Balls Segment is around 45% out of the total 480 Tonnes P.a. Capacity

The share in the revenue of the Balls segment is around 9.5% of the total Revenue

The capex is more toward the boosting the capacity of the balls segment i.e., post capex the capacity will increase from current 480 tonnes P.a. to 2500 Tonnes p.a.

Massive Capex

The capex spend is toward the machinery which will become functional in the Q3 Of current Financial Year i.e., FY 23-24

The company is going through the massive capacity expansion The current Net block is of 22 Crores and expected capex during the next 1.5 Years is 25 Crores

The company expects this capex to yield anywhere between 150 to 200 Crores of revenue from current 50 Crores of Revenue

Thing to be kept in mind while evaluating the current Capacity expansion is that There are no pre orders to cater for which the company is undergoing such huge capacity expansion The nature of industry is such that there are no Pre orders

There is different landscape in the industry i.e., SKP After completion of the Expansion will Introduce the product portfolio to OEM and then they will give order to SKP Bearings

SKP Bearings had to Let go the Some of the orders since the Capacity utilization was at peak

In Advance talk with Hyundai to land them as their customers

Moat

Rollers play important part in bearings and Bearings play important part in any machinery as the failure of it can cause the life damage and therefore no OEM in right mind would change the Suppliers, unless there is very huge Issue with the supplier

almost 100% of their revenue is from repeat Customer

Once the Relationship is formed it lasts for years and even for decades

To onboard a single client they require 2 years of time

Completed Audit of Maruti giving SKP a stand of Green Supplier, earlier it was Yellow Supplier, Now SKP can integrate with as many Suppliers of Maruti They can on board (earlier it was not Allowed)

Think of this audit as a Traffic Sign, green Light mean Go ahead

Risks

Customer Includes Major OEM like Maruti and Hyundai and Also Bearings manufacturer like Schaffler, Timken, SKF, Etc. Risk Prevails regarding the backward integration,

But the company doesn’t undertake every task of value chain under one roof or else it becomes Jack of all and master of none

SKF has already closed its Rollers Plant 5 Years Back so one can get the idea as to why Backward integration is unlikely

Brand Concepts-

Brand Concepts Sells handbags, Backpacks and Luggage Goods

The company is Licensee of Tommy Hilfiger (expires in 2023 December end, Likely to be renewed)

The Revenue from the same is around 80%

The company has the ambition to get to 500 crores of yearly revenue in Next 3 Years (FY 23 Revenue near to 160 Crores)

Brand concept helps Tommy Hilfiger to deign the bags, Sends those design to the Tommy and when the approve the same will be manufactured by Brand concepts marketed by them and sold by them

Tommy receives the Royalty in exchange of the sales made under TH name

The TAM is 24000 – 48000 Crores, which is majorly Unorganised and Organised player like VIP, Safari and This small Company is snatching the market share away from this Unorganised players (Look at performance of Safari and VIP in last 10 Years)

The company has signed 2 New Players Aeropostale and United Colour of Benetton

Aeropostale is Heavy Brand Were as UCB is light brand

They Intend to Undertake another Heavy Brand as they states that dependence on One player (TH) is big risk for them

The company is undergoing the Reverse merger with their parent company which is contract manufacturer of Luggage and Heavy Goods

The implied value of Parent company is around 50 Crores+ which is 3x Price to sales of FY 23

May be less if the Revenue has increased in this FY

The Parent company is profitable and is having double digit EBITDA margins

Cantabil Retail Ltd

Operating EBOs of Clothes in lower premium segments (ASP Of 1200 per piece)

Operates 500 stores (Weighted average last year =420)

Accounting upto 1.4 Cr of average Realisation at 530 cr Revenue

Gross margin @55% highest in industry

Working capital cycle: Lowest with fast cash conversion, Reason being backward Integration in almost each part of Value chain,

Increasing the Backward Integration by establishing one more Factory in C.F.Y,

SSG(same stores Growth) can be 5-7% p.a.

Meaning with 3 years down the line it (Realization) can be around 1.7 cr per store

New Stores guidence:- 700 stores by fy26

With 100bps improvement in EBITDA

Meaning 1.7cr70030% accounts for 357 cr FY26E EBITDA

EBITDA to free cash conversion 50% meaning at 180 cr cash p.a in 3 years

Guidence to double the same in next 3 years

Meaning almost 400 cr of FCF in next 6 years

New Stores requires 25 Lakhs. capex (Per store) opening 60-70 for 2 year each gives Capex of almost 25cr

Debt free company

Robest ROCE at 47% p.a

Anti thesis

Company’s promoters might have been involved in Some corporate governance issues, no articles though that I found

But the mention was there regarding the quality of promoters on Valuepickr forum

Cyclical company :- Season sale 65%; fresh stock sale 35%

Season sale runs for 3months while as fresh stock sale for 9 months

See the parity

Visited the store myself although the ASP in book is at 1200 per unit piece sold couldn’t find any shirt for less than 2500₹

QUALITY AND SHAREHOLDERS

the valuation seems attractive

Authum fund purchased 4% approx stake at 777₹ approx

Valuation

Company aims to double the revenue in next 3 years I.e. 1000cr

Pat margin to remain stable + - 50 bps

Say 12%p.a.

120 cr of profit

And 80% of FCF gives 96-100 cr of FCF valued cheaply at 17xFY26E FCF

And 14x FY26E EPS

Disclaimer - holding all of the above

Views are welcomed

Thanks