I feel it is the listing in NSE see the volumes post listing

1 Like

NSE listing has certainly helped, but the sudden spike of over 20% in 2 days has got me wondering is there more to this fireworks

was unable to gather any worthy information to justify the same, its peer kanchi karpooram is flat in the same period, so mostly nothing to do with camphor prices or the industry I guess

Good quaterly results, listing on NSE and capacity doubling from Jan’22 seems to be positive triggers. Looking at volume, it seems big hands are entering.

1 Like

True , A reason for this spike could be NSE Listing , but 20% In 2 days too much for Listing

I am also not able to find exact valid reasons for sudden upsurge

1 Like

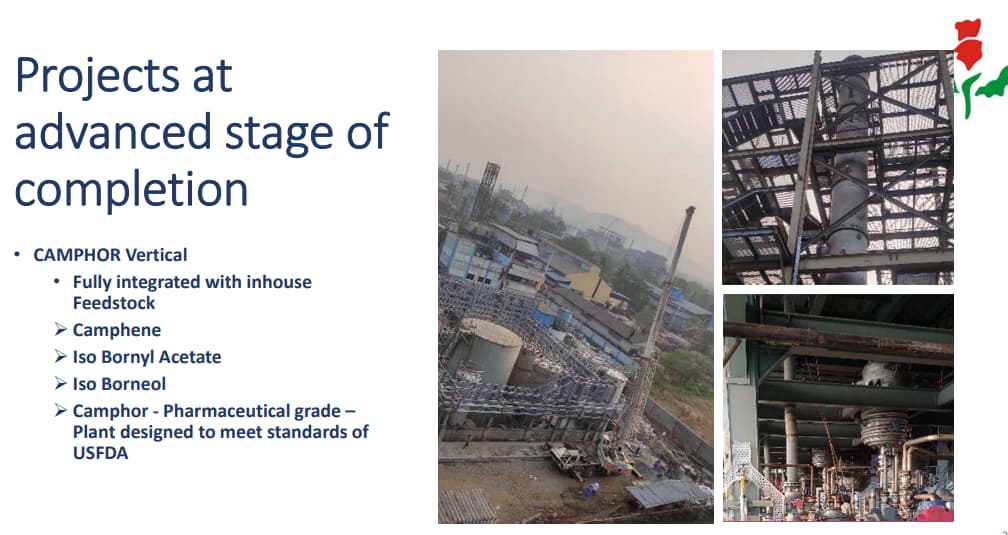

They said capacity expansion of camphor from 5000 MT to 10000 Mt. Also R.K. Damani iholding shares could be ? It’s a bull market

It is getting discovered. Some big player or broker must be promoting the story. Valuations still look attractive at these levels. P/E 10, EV/EBITA 7.

Considering doubling of capacity the forward multiples look attractive. Any timeline on when the new capacity could acheive 70-80% utilization? What is the nature of the new capacity? What is their current capacity utilization?

1 Like

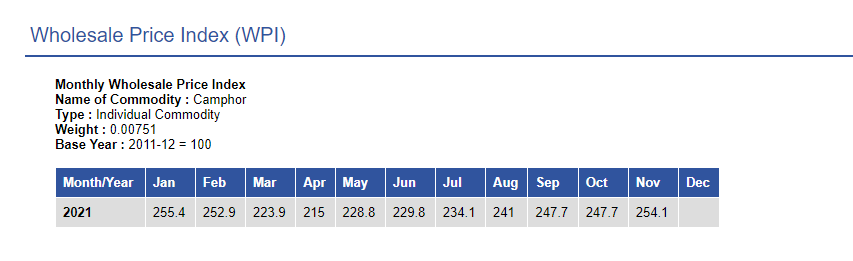

Can you share link where WPI prices are available ?

Thanks

Privi specialty has a camphor plant coming onstream shortly, capacity 4800 mtpa vs 5000 mtpa for mangalam

6 Likes

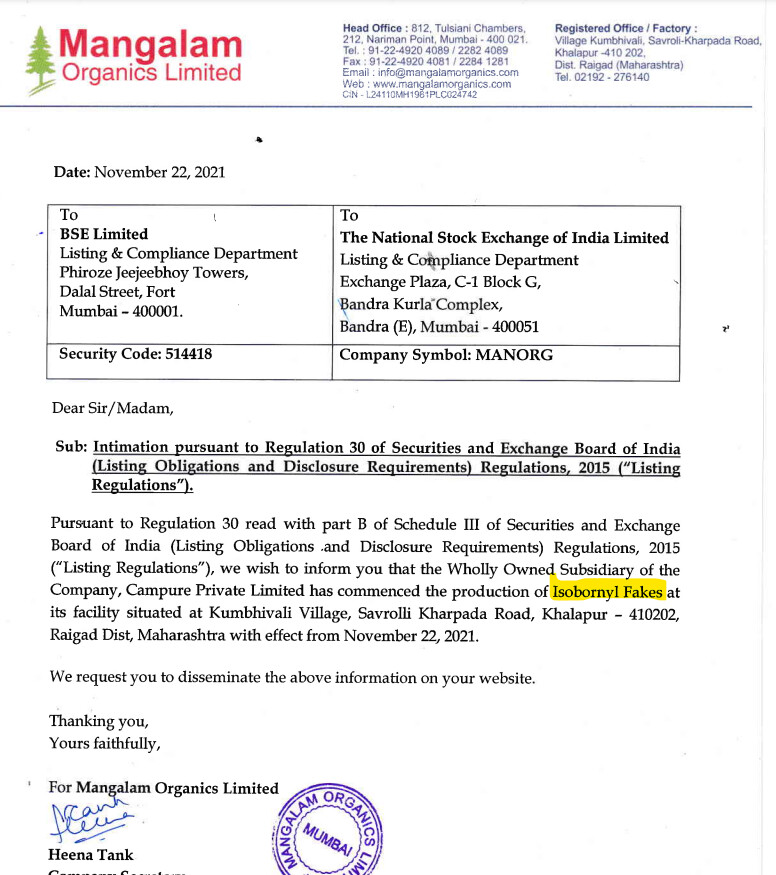

Company has commenced production of Isobornyl Fakes. Can any of the learned member tell about the expected OP margins from this product and how much this can contribute to topline.

1 Like

Isobornyl Fakes is “BHIMSENI KAPOOR”

1 Like

Wanted to check on how to interpret WPI data published on economic advisor website. As per the excel the camphor price realisations for Dec 2021 is 241.6 . Does that mean the wholesale price for camphor for dec is 241.6 and hence we can compare this with yoy or qoq to get a price trend for the end product which is camphor. Is this the right interpretation ?

1 Like

It is an index not the actual price.

So we can use it only for checking if the price has increased / decreased as compared to previous months.

2 Likes

Further announcement on additional capacity.

“Pursuant to Regulation 30 read with part B of Schedule III of Securities and Exchange Board of India

(Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”), we

infonned you vide letter dated . October 215, 2021 (https/www.bseindia.comAonl-

daty’corpfiling/AftachHis/e8b101524d6e-4e4tl-a2ca-0bc8ead598a1.pd0 that the Company had

successfully commissioned the new Steam Boilers and Thermopac to manufacture L0,000 MT per

annum of Camphor from existing capacity of 5,000 MT per annurn.

We are pleased to further infonn you that the commercial production for the additional capacity of

5000MT per annum has been started w.e.f January 31,2022and is under Stabilization”

Demand pull from retail and private labeling can lift both top line and bottom line. Also supply of pharma grade camphor to more customers can unlock the real potential of the company. This augmented capacity will play key role in these.

Disc: invested.

4 Likes

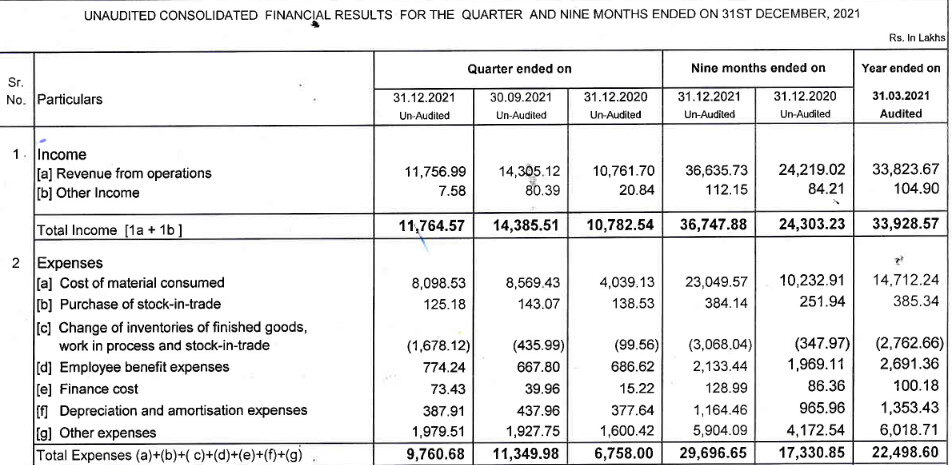

Not exciting results, however sales going up YOY. raw material cost almost doubled, cutting heavily into margins. Company’s pricing power will be tested in coming quarters.

1 Like

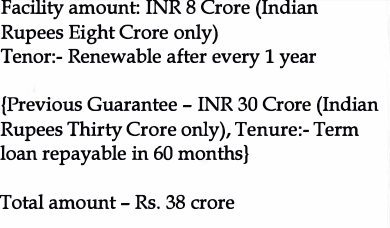

Mangalam has given guarantee to wholly owned subsidiary Campure’s term loans which is disclosed now.

"

"

A bit late disclosure, corporate governance standard needs to improve further. That said, the future prospects have not changed and remains intact, company even can positively surprise in FY23.

Disc: invested.

4 Likes