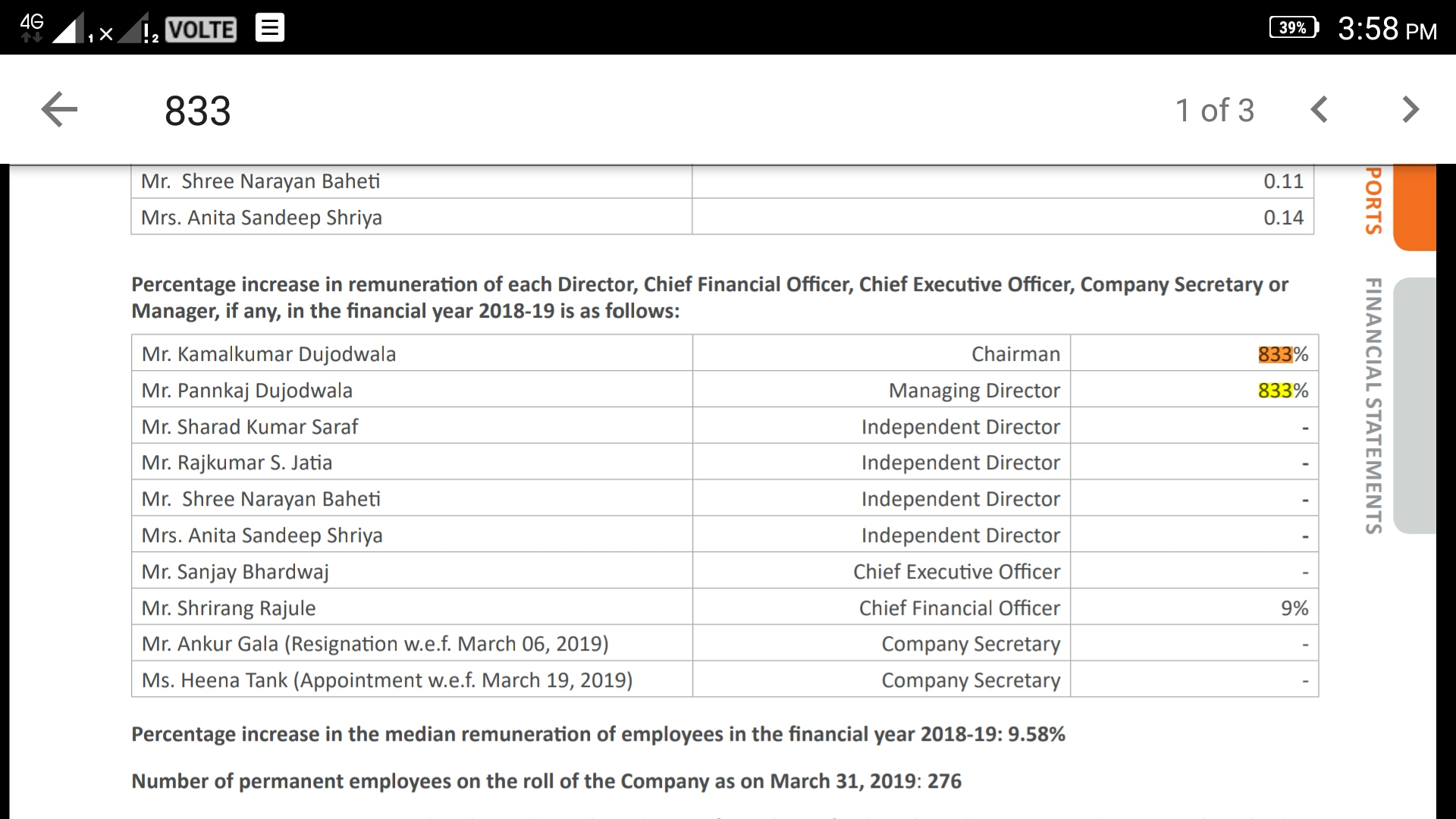

Increasing own salary by 800% while increasing salary cfo by 9% doesn’t look right. I agree management deserves the maximum credit but 800% vs 9% doesn’t sound fair.

Disclosure - I am a complete newbie so my concern might be completely misplaced.

Increasing own salary by 800% while increasing salary cfo by 9% doesn’t look right. I agree management deserves the maximum credit but 800% vs 9% doesn’t sound fair.

Disclosure - I am a complete newbie so my concern might be completely misplaced.

It is totally wrong to compare cash flow of mangalam and kanchi as mangalam is expanding it’s capacity and also it is changing it’s sales mix from being 100% B2B to also B2C player and in this shift you also need to give credit to distributors and you also need to maintain inventory which is what mangalam has done if you see properly trade receivables have jumped to 14 cr our of 100 cr PBT and there is jump in inventory to 32 cr due to there retail venture and they have paid 30% income tax that is 30 cr where is the problem and despite all this cash generated from operations is 30 cr still…on other hand kanchi has not done anything to either expand it’s business or to change it’s business model to improve margins …due to all this even if there is a correction in camphor price mangalam will easily maintain it’s margins and kanchi will face difficulty to manage it’s margins …thanks

I agree with all your points. But these are things that are likely to happen in future. But the promoters have already reaped the rewards for it by increasing salaries by 833%.

I agree with you that the percentage might look eye popping due to the small base but the base for other employees would be even smaller and the median salary increase is 9%. My reasoning is that if the promoters put themselves so far ahead of their employees, they might put themselves ahead of investors as well.

During 2018-19 there was windfall gains to certain companies due to various external factors not exactly attributable to management efforts. Some companies like Graphite India paid huge dividends Rs.55 (if I remember correctly), IOL Chemicals reduced the debt equity ratio by paying of the Loans in advance and companies like Mangalam Organics have increased the Managerial remuneration. All the above actions are within the rules, each management had it own reasons. We have to understand whether the actions taken by the management are in the best interest of all the shareholders.

Salary was increased last year this year there is no change in salary also total salary post hike is around 9% of PAT AND around 6% of PBT …they also distributed 15cr among shareholders via buy back which is 20% of PAT and promoters did not participate in the same this year dividend was less due to known and visible expansion and change in business model of company …

Buy back by the company can be viewed in both ways.

Positive: Investor friendly, reduces equity, improves EPS. Demonstrates the confidence of management in the company.

Negatives: If I have to increase my stake in the company just before a bumper year, it is very simple do a buyback and dont tell the shareholders about the tail winds. Let the uninformed shareholder tender the shares.

If you want money give the shares back, if I want, I will increase the remuneration.

Evaluating Management is a very difficult aspect and is very subjective and each shareholder can have different view.

I dont want clutter the thread further.

Thanks.

I found the Annual Report very insightful & a huge improvement over earlier years. The mgt. is working towards adding more value added derivatives which are more than likely to boost the margins. It’s reasonable to assume that the ongoing expansion will facilitate these value added products. Currently, exports are insignificant, & the expansion / upgradation will also possibly improve the quality of camphor to pharma grade enabling higher exports, besides earning about Rs. 200 per kg more in the local market. Perhaps the mgt. can be faulted for not throwing more light on the ongoing expansion in the AR.

About lower operating cash flows, as mentioned in an earlier post, the Sales have grown to 424 crs in the current year from 244 crs last year. This has led to increased working capital requirements. Debtors & inventories have gone up by 40 -50 crs. This is along expected lines.

Director’s remuneration in the context of the scale of operations is acceptable. This is a personal view & everyone is entitled to one! Besides, what option do we have other that to exit the stock, but why give up on an exciting investment opportunity over it? One has to look at the larger picture. Can this story going forward create significant share holder value or not? To me, Mangalam is hugely under valued at current levels.

Sir, without knowing what kanchi kapooram management is planning to do you should not comment on it.

Please look at the expansion plan submitted by Kanchi Kapooram to environmental clearance department on 23 August 2019. Company was suppose to increase the capacity by 2x as per earlier application made in May 2018 after which they have revised their plan and made purchase of adjacent land around 3.5 acre on which the expansion is planned.

Kanchi kapooram is expanding its capacity of camphor from 110 MT per month to 550 MT per month. For other derivative product company is expanding its capacity from 1456 MT to 3596.8 MT. As per timeline given by management the capacity will be live by April 2020. Cost of project is 14 crore. Company has also highlighted the demand and supply gap during festival season. Visit of top management people in European countries and the response they got for their product has made them to go for expansion.

Once the capacity is live think of the turnover company can achieve by operating at maximum utilisation level. Company has appointed Japanese consultant for their project feasibility study.

Further the company has funded the project by issuing preferential allotment to promoter at 360 per share. Debt is negligible as can be seen in annual report. Plant and machinery will be imported through internal accruals.

EIA report of Kanchi Kapooram is attached in 2 parts as the size is big.

Kanchi expansion-1.pdf (4.0 MB)

Already read long time back mam but it is still to receive EC And it does take long time to receive EC on other hand mangalam new capacity is coming online in October

Part 2 expansion of Kanchi Kapooram.

Environmental clearance department the file is also attached.

Status.docx (231.6 KB)

Kanchi expansion 2_reduce.pdf (2.5 MB)

Please check the details. it is under examination as earlier they plan for expansion without buying adjacent land. Now they revised the plan and expanding on newly purchased land.

Please share EIA report of mangalam organic expansion if you have. Have mangalam organic mentioned how much capacity they are expanding

Read the above article and also look at fixed assets in balance sheet and cwip

Same way Kanchi is expanding 440MT per month of camphor i.e. 5280 MT pa. and also look at kanchi annual report for the addition made to CWIP.

The promoter has infused funds of 8 Cr showing interest in their business and growth to come. They have not diluted infact raised their stake in the company.

mangalam organics current capacity is 9000 MT pa and expanded capacity will be 15000 MT pa also with this expansion it will also start manufacturing lot of new products (pine derivatives) as mentioned in AR also with new capacity it will start selling pharma grade camphor for export market which would yield them 200 rs more then synthetic camphor

Apart from agarbattis,imports of ‘other odiferous’ items from China are now restricted.

Does this move have any material impact on camphor prices?

Will mangalam organics benefit in any way?

I am surprised. I thought the Indian camphor industry is booming as China’s industry is becoming uncompetitive due to government intervention. But if that was the case, why do we need to subsidize? Are our camphor producers not efficient enough to fend for themselves? Is it time for camphor prices to fall unless artificially supported by government?

Don’t want to be an investor in a industry which requires government protection, though I like the retail story of Mangalam. Thanks to the government, my principles are in conflict with my selfish interest. I expect the subsidy to be short term positive, will use the next bounce to exit.

In quarter 1 result of 2020 why has company made provision of tax expenses of just 11 percent?

As per annual report company is paying tax around 29 percent. Shouldn’t it be case were company should make proper estimate of taxes quarter on quarter basis?

As per my understanding company does not enjoy any tax benefits from government. Further as per IT law if company in excess of of 400 cr turnover need to pay tax MMR. Accordingly if company could have made provision at MMR then profit could have read at 12 CR instead of 17 Cr.

Views are invited

Promoter akshay k dujodwala, bought 1.6 lakh shares @314.35 today.(Source : bse website > bulk deals.

This bodes well and a clear signal by promoters, on the extent of undervaluation of MO!

Nice to see promoter increasing holding by almost 2% today (5 Cr by value), taking total promoter holding to about 52%, from 47% it was early last year, before the tailwinds began. At least the salary increases they gave themselves seem to be used for showing faith in their business.

If anyone goes to the AGM, please share notes.

@phreakv6 - any thoughts on supply side of such huge delivery of shares? Surely good sign for investors though:)