Hello All,

Around 5-6 quarters ago company was posting losses but it has turned around from thereon with consistently positive net profit, along with increase in sales. It is one of the largest Malaria API producer in the world and it has WHO ,GMP approved facilities.

Key points:

1)From negative EPS, it has turned to TTM EPS of around 10. 3 Year CAGR NP 107%.

2)Promoters knew about this turn around in advanced and that why they increased stake in the company by 10%(by issuing warrants, 5% converted, remaining 5% will be converted in next FY soon). New holding will be 52% after conversion of remaining 5% warrants.

3)Company’s sales is also increasing with the increasing demand in domestic segment. 3 year CAGR sales 13%.

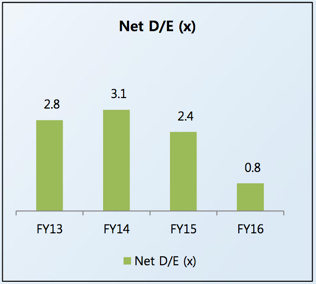

4)Company has reduced debt drastically recently by using warrants money received, this will reduce interest and improve NPM in near future, thus EPS will be increased.

5)Expansion is going on the existing plant for newly approved product on HIV and some new approvals waiting for WHO approval(please refer to the investor presentation for product details).

Important links:

1)Company management is doing an Excellent job by publishing the result within 2-3weeks after completion of q(it was 5-6 weeks earlier) and again they have proved it by putting enough effort to create such a well written Investor Presentation.

Must read Investor Presentation containing all required information for all investors:

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=a181d847-2c62-472b-b2b5-d926306d0abd

2)Article on Mangalam Drugs:

3)Company website:

http://www.mangalamdrugs.com/

Concerns:

1)Promoter stake pledged is around 60%(decreased from 97%), however it has been pledged at price less than 20, so there is no risk of invoking, however it should be released for confidence of investors.

2) With TTM EPS 0f 10, it should start paying dividend(no dividend as of now for reducing debt and expansion , but in near future it should share the profit with shareholders).

I know a lot of VP boarders are having huge knowledge on Pharma sector, I would request them to analyze the company fundamentals, potential of its products and future prospect ignoring the price chart movement(sharply up/down movement is being seen recently).

Disclosure: Invested.