To begin with, an honest disclaimer, I have no back ground experience on company’s financial system/analysis. However, the reason forced me to write on this subject is no discussion on Mandhana-Demerger till date.

I do see some potential value in Mandhana Demerger. Requesting forum experts to guide me further whether to stay invested or exit.

The brief :

Mandhana is going to demerge Retail division (Being Human, Salman Khan brand). Details available on number of stores and future plan in many websites. The key take away is…

The retail division is going to post 40% Y-o-Y growth till 2019.

Higher Net profit margin.

The promoters increased their shares and very upbeat on retail division.

The bad : - Promoter pledged shares. - Though high court approved the scheme on 29-March-2016, till date the company not fixed the record-date. I suspect its due to worry of pledged shares’ stop loss triggering on ex-date. - Solely depend on Salman Khan.

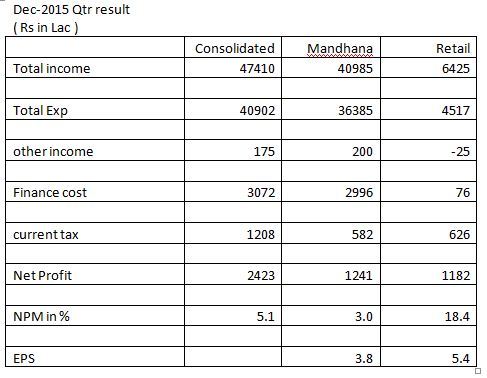

The only available financial figure of Retail is from their Standalone Dec-2015 qtr result declared recently and compared with the same Qtr result in previous qty which included retail details.

Annualized EPS for Retail division may be around 22 in FY2015-16 and 31 ( 40% growth ) in FY2017. Though high growth sector PE rating may be higher around 25 or 30, I have given conservative figure as 20. For Mandhana, I considered 10 PE.

The expected demerger-unlocking in few months time……100% gain. Demerger ration 3:2, i.e 2 Retail for every 3 held in Mandhana.

( I’m not able to stick 2nd image showing the profit calculation of demerger…will add in the thread ).

Apologize if I offended the financial experts or violated the forum rules / regulations.

First of all the figures in both Dec and March results for the qrt Dec 15 do not match in any respect and are wide off the mark.

Now secondly I do not get it from where have you arrived at the figures of retail sales of 6425 lacs.

Garment capital emloyed is nearly 20% of total CE so how come interest cost is only 3.5% of the total interest outgo.

Things do not add up or am I missing something.

Bests

Manoj

Hi all

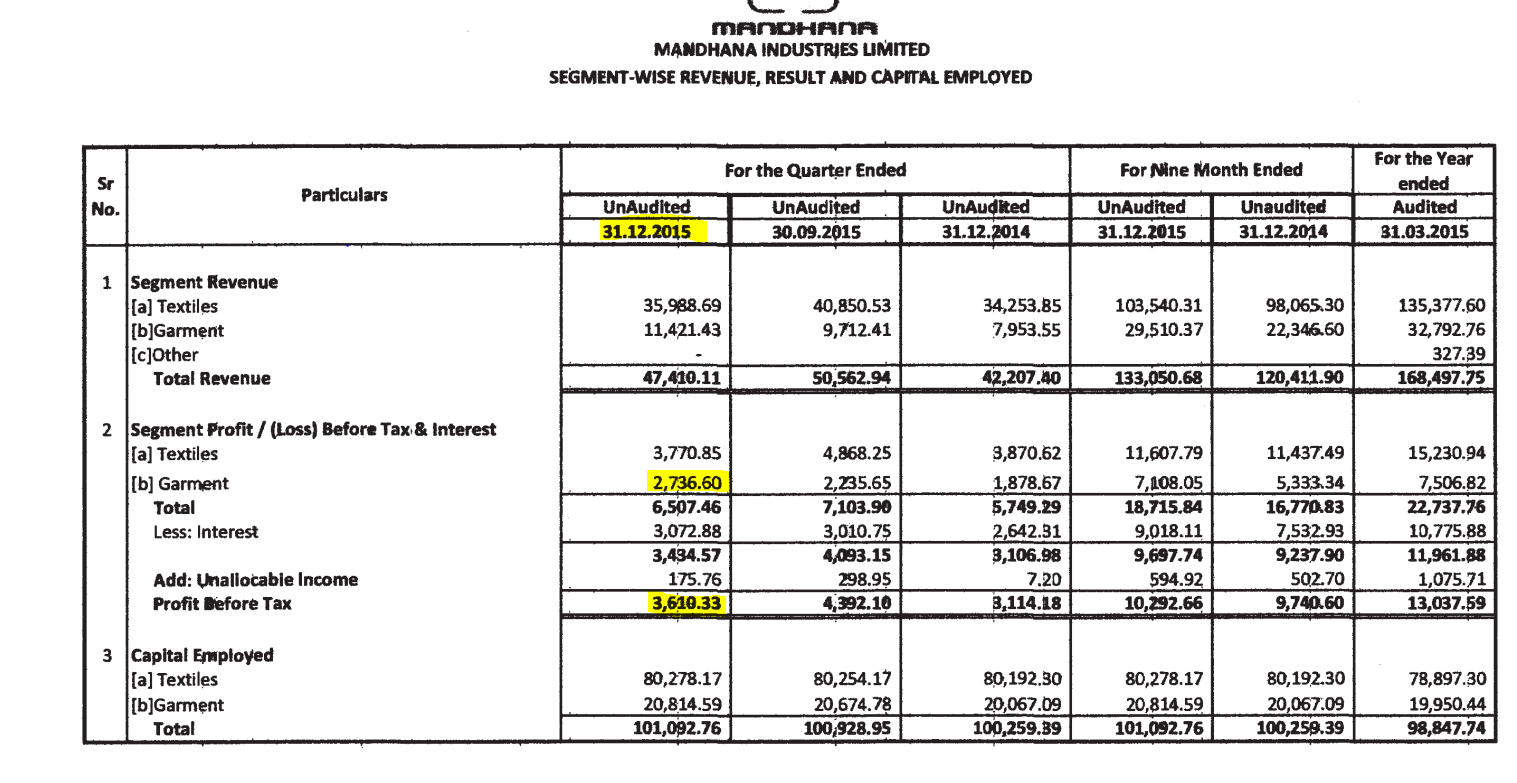

I’ve been tracking and invested in Mandhana for over a year. In Q4, they got their demerger sanctioned and in the March 2016 results, they only have their textiles and garments division as part of their P&L. However, by doing some simple bootstrapping it is possible to get results for Mandhana Retail (Being Human), which was included in the garments portion of segment reporting until December 2015:

Till December 2015, 9 month results of Mandhana shows Garment sales as 295 crores and EBIT as 71 crores.

On March 2015, garment sales are 210 crores ans EBIT is 41 crores (This excludes Mandhana retail as figures have been restated post demerger). Now we remove the figures of garment sales and EBIT for March Quarter which are 70 crores and 12.5 crores respectively from the annual numbers. The residual is 9 month figures of garments without Retail arm. These are 210-70 = 140 crores and 41-12.5 = 28.5 crores

Third step is to extrapolate Mandhana Retail sales and EBIT for 9 month ended March 2015, so subtract Step 1 from Step 2, which is Sales: 295-140 = 155 crores, EBIT: 71-28.5 = 42.5 crores.

Now with 9 month figures, we can make an inference of 12 month figures of Mandhana Retail (Being Human), we just add the quarterly runrate with say a 10-20% growth rate to take into account additional winter season sales that will be reflected in the March 2016 quarter. So let’s say March quarter sales are 155/3 quarters *110% and EBIT is 42.5 / 3 quarters *120%. These figures are 57 crores and 17 crores respectively.

Now we add step 4 to step 3, thus total extrapolated 2016 sales of Mandhana retail are 155+57 crores = 212 crores, and total EBIT is 42.5+17 = 59.5 crores.

Valuation of Being Human: Applying principles of conservatism, let us take EBIT as 55 crores and not 59.5. EBIT after tax = 55*70% = 38.5. Good multiple for Being Human is 15, so Valuation = 38.5 X 15 = 577.5 crores, round down to 550 crores - No adjustment needed for Debt because company will be almost debt free as per management. Some adjustment may be needed for future store capex and for inventory investments.

Valuation of Mandhana Industries (Remaining) = considering that the company is highly levered, it deserves a lower multiple than the industry - let us apply a blank PE multiple of 4 to PAT of 2016 = 57 crores times 4 = 230 crores

Total valuation of combined entity = 780 crores

Current market cap as on June 20 = 740 crores

Note that I have tried to take extremely conservative numbers. Thus although the undervaluation apparently looks just 40 crores, this is essentially a margin of safety computation and upside should ideally be considerably more.

No idea on why the stock is down 20% today. However, few days back there was a FIR against Salman Khan of Rape case filed by an attention-seeking cine screen lady. No one believe this case thats why no big coverage by media.

Just 2 lac shares traded today…20% down.

Delivery 64%.

The management is very careless…silent for last two-and-half month on why the delay in fixing the record date for demerger.

Now the corporate governance is under scrutiny. Hereafter market may not give thumps up even for good result in Retail division.

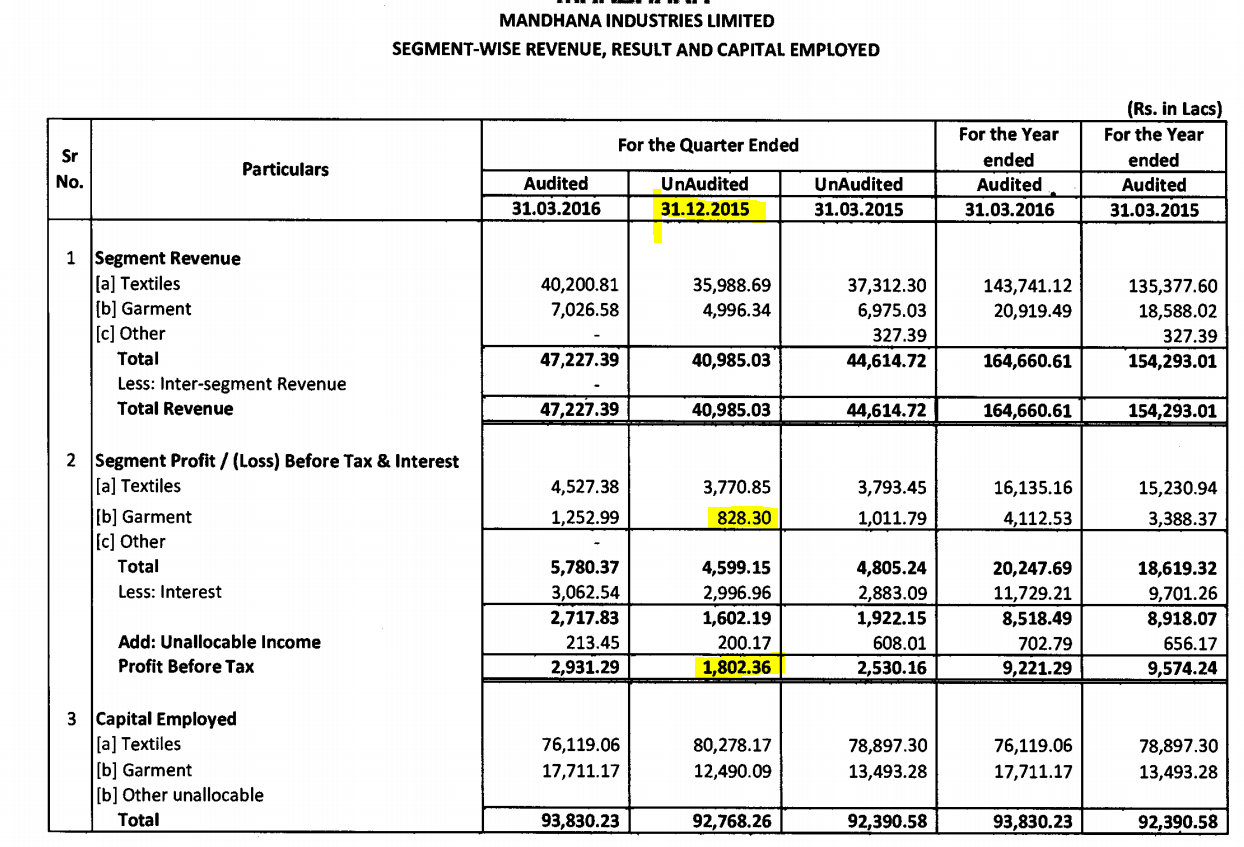

@manojag You have missed Notes to account number 3 which says

…the result of the discontinued retail division of MIL is not included for current as well as previous periods given above.

@AxisVarun I have re-checked. Your calculation for MRVL looks broadly correct. I could not understand why company did not include the result of retail division in Q4FY16 when in fact the demerger is effective Q1FY17 i.e 1-Apr-16.

Promoter must be buying from open market because they could see lot of value unlocking. It is good sign, IMHO.

But could not understand the reason for this 20% down filter along with volume breaker in both BSE & NSE.

@Gaurav_Agarwal

Thanks for endorsing my calculation.

Upon frustration, I called the company about a week ago. The receptionist transferred the line to a guy. My concern was why the RoC is taking too long to register after court approval. Understood that the RoC part is a done matter and the ball is in Management court for so long to fix the record date.

I sent emails too…but no response.

My worry is…if the down circuit continues then no one can stop as its a illiquid counter also the stock gets down rating…won’t get premium rating for Being Human listing.

Looking it at another way the consolidated NP for nine months was Rs.6806 lacs as per Dec qrt results.

Full year profit without Retail for March 16 is 5713 lacs. From this we deduct March qrt NP of 1594 to get nine months stand alone NP of 4119 which is the np without retail. So retail NP for nine moths is 2687 lacs giving an annaulised eps of 16.25

The total pledged shares of promoter is 1.11 Cr ( out of 2.41 Cr )

Just a while back the situation was covered by CNBC-TV18. They spoke to company management. According to them there is no selling from Promoters. TV18 too have no clue on who is selling.

The other share holders detail–

LIC - 6.58 lk

Religare Finvest - 5.2 lk

Axis Bank - 4.97 lk

Bajaj Allianz - 3.5 lk

According to Moneycontrol.com, other investor holding more than 1% are

Azarel Fashions Private Limited - 5.1 lac shares

Arnold Holdings Limited - 9.5 lac shares

Win Sure Invest Private Limited - 5.0 lac shares

Orders outstanding in BSE & NSE on Tue 21 Jun 16 12:31pm are 15.38 lac.

Can pledged shares be sold without margin being triggered?

I can think of two possibilities in this case

Either one or more investors holding more than 1% were in touch with the management and their issues were not taken seriously by the company and therefore they have dumped shares in the open market

Someone is trying to do hostile takeover of the company by dumping the shares in the open market and as result triggering the margin call on pledged shares, putting additional pressure on promoters.