@Prdnt_investor 7 months back the share price of Manappuram was around Rs 85-90. Are you sure Nandakumar sold 4.3% 7 months back? Infact VP Nandakumar has only bought shares in 2016, he never sold a single share. Verify this yourself at the BSE trading disclosures link

The business outlook for this financial year - growth in AUM in the range of 15 to 20 per cent. non-gold businesses already contribute about 16 per cent of our total business, which we hope will increase to 25 per cent by the end of 2017-18.

Thanks for very timely sharing. Based upon RJ blog that Samir Arora has exited micro finance business and declared that he would never enter it again- I was seriously considering pruning my holding in Manappuram tomorrow. However, based upon what you have shared- I will increase my holding tomorrow ! Thanks.

@yudiaag Friend, do not take anyone’s analysis or statement on face value , be it Samir arora or nandkumar until you have tremendous confidence and evidences of their success ratios

Something seems off about their Cash from operating activities. Fluctuating wildly from -ve to +ve and back. Does anyone have an idea what could be the reason?

It’s probably because their loan book (considered as part of operations) contracted in 2013 and 2014 because of RBI regulations and LTV and duration of loan. This must’ve led to inflow from operations (usually a sign of contraction in the financial sector)

It’s common in most of the financial companies.

Their cash flow fluctuate positive /negative.

For validation you can check the same for hdfc bank, icici bank etc. Actually it’s quite complex to read cash flow of such institutes. The best parameter for such companies is the honesty and quality of management. Then comes growth, RoA etc

I agree. The way one need to look at Finance company is different. Though i am also learning it, but is essential to know it as absence of such insight may lead to serious trouble as well.

I think markets are spooked by results of the MFIs and SFBs and Manappuram also own a MFI business

RBI regulation on gold loan cash disbursement limit to 20k affects about 25-30% of all GL disbursements

However, I’m thinking that the current valuations mean that any average Q4 results shouldn’t also take this much lower unless there is an overall market correction.

Reminds me of a recent TV quote - ‘You either get good prices or good news’ - good prices these days I say

It formed the handle in March when it hit 105 but failed to breakout and instead has fallen for over a month now. Today’s rally gives hope. Fingers crossed.

Manappurum share price is well correlated with price of gold at least in the short to medium term. So far discussion on this correlation has been focused on effect of drop in gold prices on the NPAs and resulting credit costs. While we have seen credit costs have gone up in the past when gold prices dropped, rise in credit costs were not big enough to say that gold prices have a substantial impact on the bottom line simply due to rise in credit costs.

Upon further analysis, I noticed that a drop in gold prices forces Manapputum to reduce (or limit the growth of) its loan portfolio as it has to maintain loan-to-value ratio. This limit on loan portfolio actually has a big impact on its interest income and bottom line more than the credit costs.

Only way Manappurum can grow its loan portfolio (in terms Rs Cr) is to grow the size of its gold holdings (in tons) such that rise in tonnage will more than offset drop in gold price thereby keeping value of collateral from falling too much.

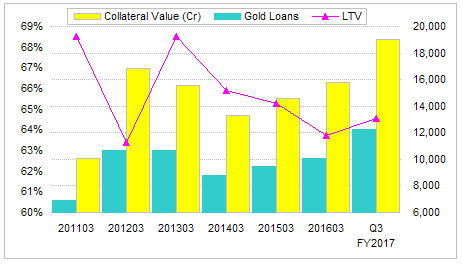

Here is a quick chart that shows gold tonnage, loan portfolio and LTV ratio over last few years.

Source: Company Annual Reports

This chart clearly shows that company’s loan portfolio (green columns) is well correlated with value of the collateral (yellow column) and its LTV is maintained just close to prescribed minimum (which was cut in 2012).

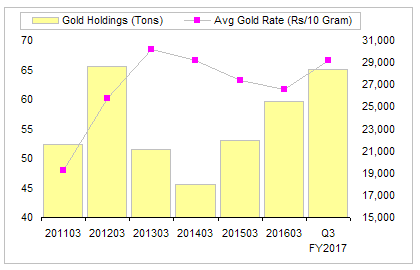

Value of collateral is further broken into gold tonnage and gold price. Chart below shows two numbers.

Source: Company Annual Reports & IR Presentations.

This chart shows that until 2012, both gold prices and gold holdings were rising which resulted in sharp rise in value of collateral and loan portfolio. 2013 came as a shock as LTVs were brought down by RBI so gold holdings dropped even if gold prices rose. Since borrowers could not put up more collateral, gold holdings dropped further in 2014. Gold prices also dropped in 2014 resulting in a sharp drop in collateral value and loan portfolio. Over the next 2 years, while gold prices continued to trend lower, Manappurum was able to grow its gold holdings fast enough to offset the drop in gold prices resulting in growth in net loan portfolio.

Last one year has seen the dual effect of rise in gold price and rise in gold holdings (exact opposite of 2014) resulting in sharp rise in gold portfolio and recovery in share price (which has quadrupled in last one year).

The point is, gold prices do affect Manappurum profits and share price but not because of impact on credit losses but rather for a simple reason of its impact on size of the loan portfolio.

Results seem largely in line with expectations … especially considering time for business to pick up after demonetization impact and Return to normalcy somewhere in mid q4 … concall details will be awaited