can be good in the long term as bain capital can subscribe to loans of the company and other support if required -Parent support

may make the company more professional

real question what will be the role of Nandakumar and his family?

will the culture and the management change

will that be good or bad?

1 Like

This Indiainfoline referring to this piece from ET:

Some key points mentioned by ET:

“Bain is said to have shown interest in buying a 10-11% stake from Nandakumar’s family and simultaneously infusing Rs 2,000 crore of primary capital into the shadow lender via a preferential allotment. It will then make a voluntary open offer for an additional 25% of the company which, if fully subscribed, will take its economic interest to 45-47%, making it the single largest shareholder. Bain is keen on controlling rights to ensure the company is professionally run. Bain is said to have offered a premium of 20-25% to the current market price. However, this could not be independently verified. At the present market value, a 47% stake would cost Rs 6,289.46 crore.”

“Nandakumar is trying to retain control and only dilute a smaller 5-10% to bring in “confidence capital,” said one of the persons. But the Boston-headquartered private equity (PE) group has made clear that a minority stake is of no interest.”

"Succession Challenges:

Industry sources said the Reserve Bank of India (RBI) has not been enthused by the addition of Nandakumar’s daughter Sumitha Jayasankar to the board as executive director. A gynaecologist by profession, she has been groomed to take over the reins at the company from her father.

Coming under pressure from the regulator on the issue of succession planning and realising that RBI may prefer an out-and-out finance professional rather than anybody in the family taking the leadership, Nandakumar started thinking of divesting his stake,” a person aware of the development said.

He has engaged previously with strategic and financial investors including IDFC and Poonawalla Finance as well as PE funds such as Carlyle to explore a buy-in, business carve-out or even a merger of operations, said the people cited. Those negotiations didn’t work out and there is no guarantee that the current discussions will end in a transaction, they said."

Key takeaways:

- There are interest private parties, who see a potential money making opportunity in Manappuram.

- The one with capital will come, when they will have their ways to operate business - not interested in minority stake.

- Current promoter’s next generation - not considered good (as per regulator as well as market forces)

- Current promoter don’t want to let go of operational control to professionals (deputed by a private party) .

- In past also, there were talks of takeover - but no result.

- Most important - Either current promoter will have to mend his ways - the way he run business (means bring in professional as his replacement) OR regulator will keep their life as difficult as possible OR down the line they may be some hostile takeover opportunities too.

Disc: Invested

7 Likes

Bain Capital will be an equity investor not a debt investor - Hence, my view is they will not subscribe to loans of company.

For Sure, Bain Capital will put in their best people to run the show. At the end of day, they will expect ROE (on their own equity investment) in double digits and that will happen will Company share price will increase, and that will help each investor.

Imagine a scenario, where valuation gap (in terms of P/B and P/E) between Manappuram and Muthoot is skewed to nil.

6 Likes

With monthly repayment (like EMI) for sure outstanding exposure to a borrower is going to be reduced regularly.

But at an operational level or AUM growth per se, any thoughts from fellow investors - if any (-ve) impact on Manappuram ?

1 Like

In Bangalore I see Rupeek aggressively marketing gold loans with these kinds of boards in many small petty shops.

1 Like

When I reviewed the screener, I noticed that the Earnings Per Share (EPS) of Manappuram Finance increased significantly, from ₹11.16 in March 2019 to approximately ₹26 in 2024. However, during the same period, the stock price has not appreciated; in fact, it appears to have slightly declined.

Given that five years is considered a sufficiently long horizon, I am curious as to why the stock price has not moved in tandem with the company’s earnings growth. Members of the forum, could you help me understand what factors I might be overlooking?

1 Like

please search in google news about ban on microfinance loans and refer to previous chats in the forum you will understand

expected for Asirvad also soon?

2 Likes

Put in another way, the price to earnings ratio has declined during this period. Or in market parlance there has been a derating of the stock.

Rerating and derating can happen due to various reasons and all reasons point towards change in market expectations regarding the future of the company. It can be change in expectations regarding growth, margin, need for reinvestments or the cost of capital.

From ED raids to COVID related disruption to change in product mix to change in competitive environment, expectations may have indeed changed for Manappuram.

The question seems to stem from the saying that stock prices should be slave to corporate earnings. While it acts as a good general guidance, expecting a perfect correlation is not warranted. A better and may be a more robust perspective is to view stock price as the present value of future cash-flows.

It is a different question whether we as individual investors agree with the change in market expectations or not.

PS: If you use a different time frame, say 2006 Nov to 2024 Nov, the price has grown by about 210 times but the EPS has grown only by about 150 times.Do we really have a reason to complain?

9 Likes

https://rbidocs.rbi.org.in/rdocs/PressRelease/PDFs/PR162884107C3460F3464BB431BD7037A3ACB1.PDF

NAVI achieved success in 45 days.

That is an example of fire in belly.

NAVI’s emergency response, be it to regulator or investors seems above all. They have established when it is the matter of existence, management will not leave any stone unturn to get the life back.

Is Manappuram doing the same … May be Yes, may be No.

In their last concall, VP Nandakumar said “Next week, we are meeting deputy governor, etcetera” Page 8of18 - https://www.bseindia.com/xml-data/corpfiling/AttachHis/6edf2abd-3419-49c0-b327-93043bc502c4.pdf

But Muthoot management clarified, to the question of Abhijit Tibrewal of Motilal Oswal, in their concall - “I don’t think any such meeting has taken place and I don’t know. I’m not aware of such meeting” - Page 6of17 https://www.bseindia.com/xml-data/corpfiling/AttachHis/88aa3134-74ef-44b8-a141-bc96d7b2fe3b.pdf

Valuation per se, Manappuram shares seems to be discounting the discomfort (and may be questionable) in integrity of VP Nandkumar led Management.

Disc: Invested, but not okay with the way VP Nandkumar is managing business recently.

3 Likes

-Hopefully soon RBI will lift the ban from ashirvad

-gold growth looking good at least in medium term

- consistent growth in book value

- Consistent increase in dividened

- management walk the talk always… experienced many times in past eg in covid , demonitisation , ED raid ,bank competition

- and now hopefully with ashirwad ban they will act soon

6 Likes

1 Like

Navi is able to resolve their new loan ban issue swiftly with RBI, why Malappuram is not able to show such urgency, management need to show fire in belly to increase business, they might lost much interest in expanding business and it will be better new promoters comes who are interested in creating wealth.

3 Likes

After the recent Ban from RBI on issuing new loans through Manappuram’s microfinance division, the stock fell up to 130 rs and currently trading at 175 as on today.

In my view, even if their microfinance division is adjusted or removed completely, the stock is at fair value.

as we know there is a tightening rule by RBI for unsecured loans, can’t expect a huge growth in this segment as well.

Here is my basic P&L statement Analysis:

5 Likes

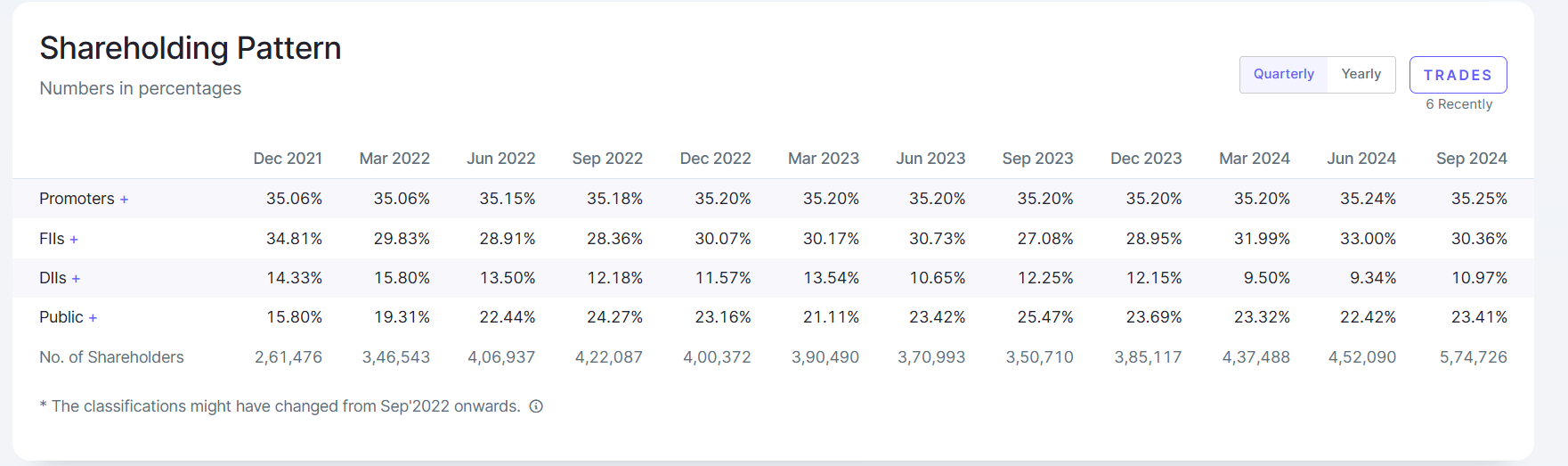

FII shareholdings is down from 34.81% in Dec’21 to 30.36% in Sep’24, still substantial %age (1/3rd ) own by them. DII holdings is down from 14.33% to 10.97%. public share holding increased from 15.8% to 23.41%. number of shareholders increased from 2.61 Lac to 5.74Lac (double)

FII - No major names except , 3.4% hold by smallcap world fund.

DII -2 MF DSP & SBI

Public -No Major name.

high number of retail investors.

whats your observations here, please share

2 Likes

Judging by the momentum, it seems the ban is likely to be lifted soon. Perhaps traders have caught wind of the news.

1 Like

Frankly, none of these concerns matter if the company delivers strong fundamental performance. Narratives shift swiftly. In the past, Manappuram was criticized for its concentrated gold loan book, which analysts linked to low valuations. Now, despite diversifying into MFI, home finance, vehicle finance, and MSME lending, the concern has shifted to the unseasoned nature of the new portfolio and potential asset quality challenges. There will always be some narrative.

The company has successfully navigated various headwinds in the past, and if its performance continues to improve, investors will return, and the narrative will shift accordingly. Management succession might pose a temporary overhang, but this could stabilize if a fund acquires a significant stake with management control.

Disc- Invested and hence views could be biased.

9 Likes

While not comparable, take the case of Suzlon Energy. Stock hovered around 5-10 rs for years/ almost a decade. It was all in the hands of retail investors only. No institution, mutual fund were present. And retail was mocked for buying a company which is struggling. All changed within a year in FY23. The larger point I am trying to drive is all the analyses we see is post facto. Good fundamental performance changes all stories and as long term investors our endeavour should only be to keep finding signs of improving fundamentals. Rest all is for news articles.

6 Likes

If stock price does not appreciate in a 1-2 year timeframe then it is obvious that retail investor starts getting frustrated. This is due to his limited capital available with him. What should be the mindframe for the long term investor to hold for 10 years without any appreciation in capital?

1 Like

Unfortunately, now a days, Narrative is highly mis-used word be it in national politics or investing world. When we don’t like something, often it is called as Narrative by others.

We as an investor must look at the actions of management. If Manappuram has been underperforming vs its peers like (Muthoot, IIFL, other NBFCs etc.) then there must be reason to investigate and ask not just few but millions of questions to management - specially when the same management is promoter also.

Mr. VP Nandkumar don’t have any succession plan, his kids are not interested in business.

Unethically, in personal capacity also he bought shares in Asirvaad along side listed Manappuram (ideally if VP Nandakumar got an opportunity, every other shareholders must have got the same opportunity).

Look at the skillset & capabilities of Management personal deployed in Asirvaad vs that of listed peer MFIs (for Ex CreditAccess Grameen etc.) - and we will see the difference.

Similarly, for Home Finance, have a look at Management personal of listed peers - and we will have reasons why those peers are above 2 times Book value and why manappuram is at discount.

For an investor, returns matter. It’s the bread & butter for investor to remian invested in a listed stock.

For Management, its their Salary (and other disclosed/undisclosed perks).

I remember, there was an FPI investor " Quinag Acquisition (Fpi) Ltd", who invested in Manappuram for almost 5 years, but in USD terms hardly they made any return, unfortunately in Sep 2023 querter they exited just before filing of IPO papers of Asirvaad.

1st Disc: Invested from last 5+ years, and looking to start liquidate position gradually once 200+. Now it’s not much of a return in Manappuram, but less trust in VP Nandakumar.

2nd Disc: View’s is subject to change in case change in promoter either because of friendly sell down or hostile takeover.

6 Likes