Main takeaway message from interview I think is :

Unorganized lenders are the biggest players in this sector and they account for an estimated two-thirds of all lending,

Although banks are gradually attracting some of their customers, the market remains extensive, presenting ample opportunities for growth.

This is a fast-paced retail business where customers take out loans for acute short-term needs, typically lasting 2-3 months. Interest rates are less important than convenience, which is where NBFCs have an edge over banks. Customer loyalty is low, and borrowers prioritize quick access to funds and repayment. They often turn to local lenders or NBFCs for speedy loan processing. This differs from long-term housing loans, which require more consideration. Given the operational challenges and lack of customer loyalty, larger players like banks are typically not interested in this segment. Nonetheless, the nbfcs have proven resilient due to their focus on speed and service, and NBFCs with their quick access and excellent service have become a preferred choice for short-term loan borrowers

I feel that by this time next year, banks will have lost their momentum and will shift their focus towards large-scale lending. They are unlikely to dedicate significant resources towards retail lending due to the inability to sustain high-quality service standards in this segment.

There are borrowers who seek a reputable brand when obtaining an emotional gold loan, with Manappuram and Muthoot being trusted names in the industry after operating for several decades. Such borrowers may be hesitant to approach new or unfamiliar businesses for gold loan services. Additionally, borrowers may opt for local lenders whom they have known for many years and trust to safeguard their gold. Market participants will acquire customers based on their specific criteria, and all are likely to thrive and expand their market share. Banks, for instance, will concentrate on attracting high-value, long-term loan customers, while other players will target different segments of the market.

At present, Manappuram’s stock is trading below its book value, implying that the entire business is undervalued relative to its total worth. The market appears to be overlooking the value of the company’s long-standing brand, operational expertise, diverse customer base, experienced management team, and other factors. Consequently, Manappuram’s share price has fluctuated significantly from 52 week to 52 week, resulting in a roller coaster ride for investors. Nonetheless, these fluctuations present opportunities for traders to capitalize on market movements.

I have personally found the Manappuram market fluctuations to be useful and have used various financial instruments, including options, calls, puts, futures, and equities. I prefer volatile fluctuations to a steady, unidirectional trend as they offer more opportunities to capitalize on short as well as long term price movements.

I feel the promising uptrend in microfinance coupled with a moderate increase in gold loan growth has the potential to elevate manappuram’s growth trajectory, possibly reaching the all time high in 2023

Sub-12% gold loans have completely run down. Gold loan yields is 21%, with incremental bank borrowing cost being 8.5-8.75%.

Asirvad AUM has crossed 10k cr., implying ~25% QoQ growth. Growth is through new customer acquisitions. Manappuram will infuse 250 cr. into Asirvad and is also looking to raise equity capital of $100-125mn.

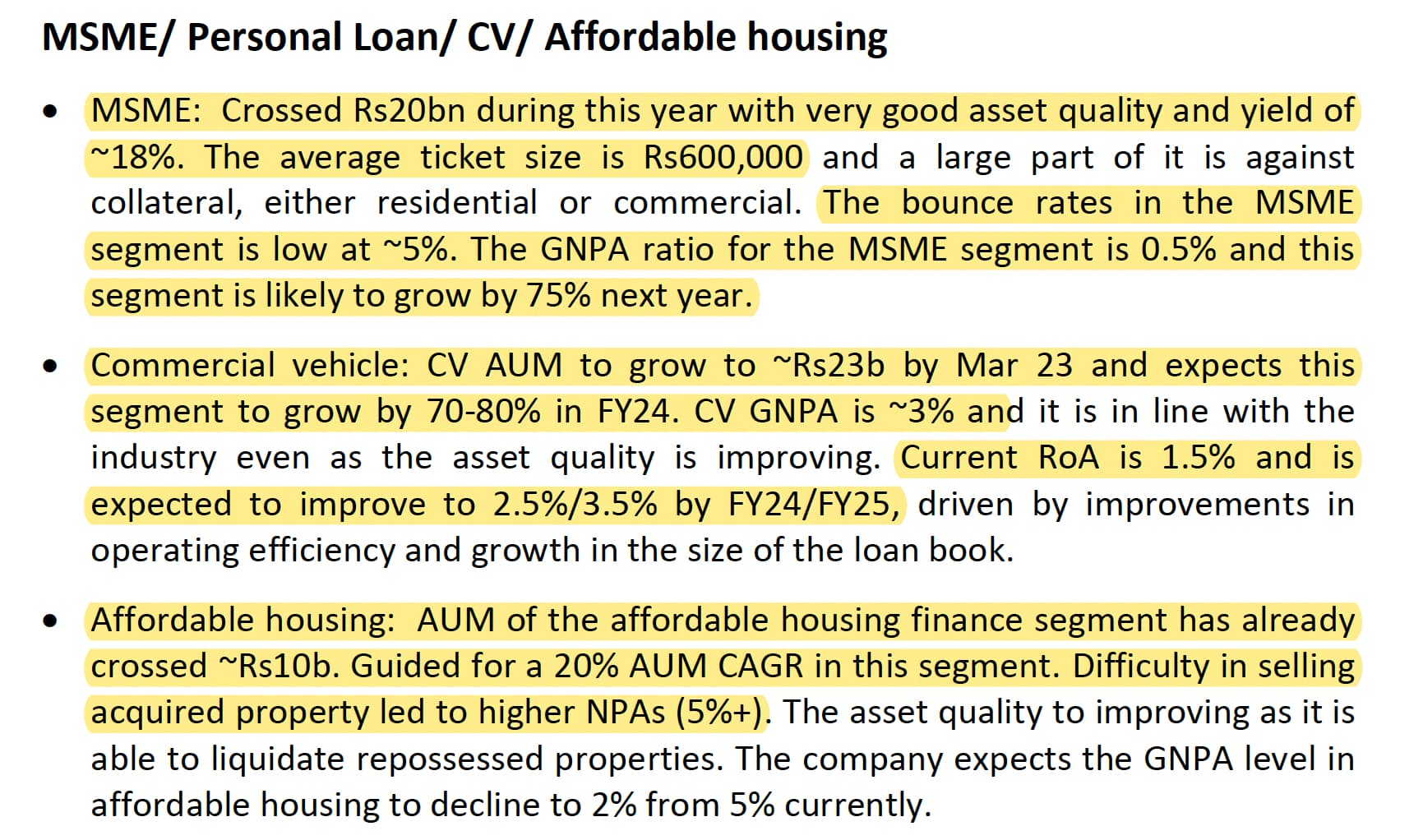

Overall, Manappuram is emerging as a diversified NBFC where their non-gold loan will contribute 50% of portfolio by FY24. The diversification journey embarked in 2015 will finally start bearing fruit, this is where I feel Manappuram has left Muthoot far behind.

Disclosure: Invested (position size here, no transactions in last-30 days)

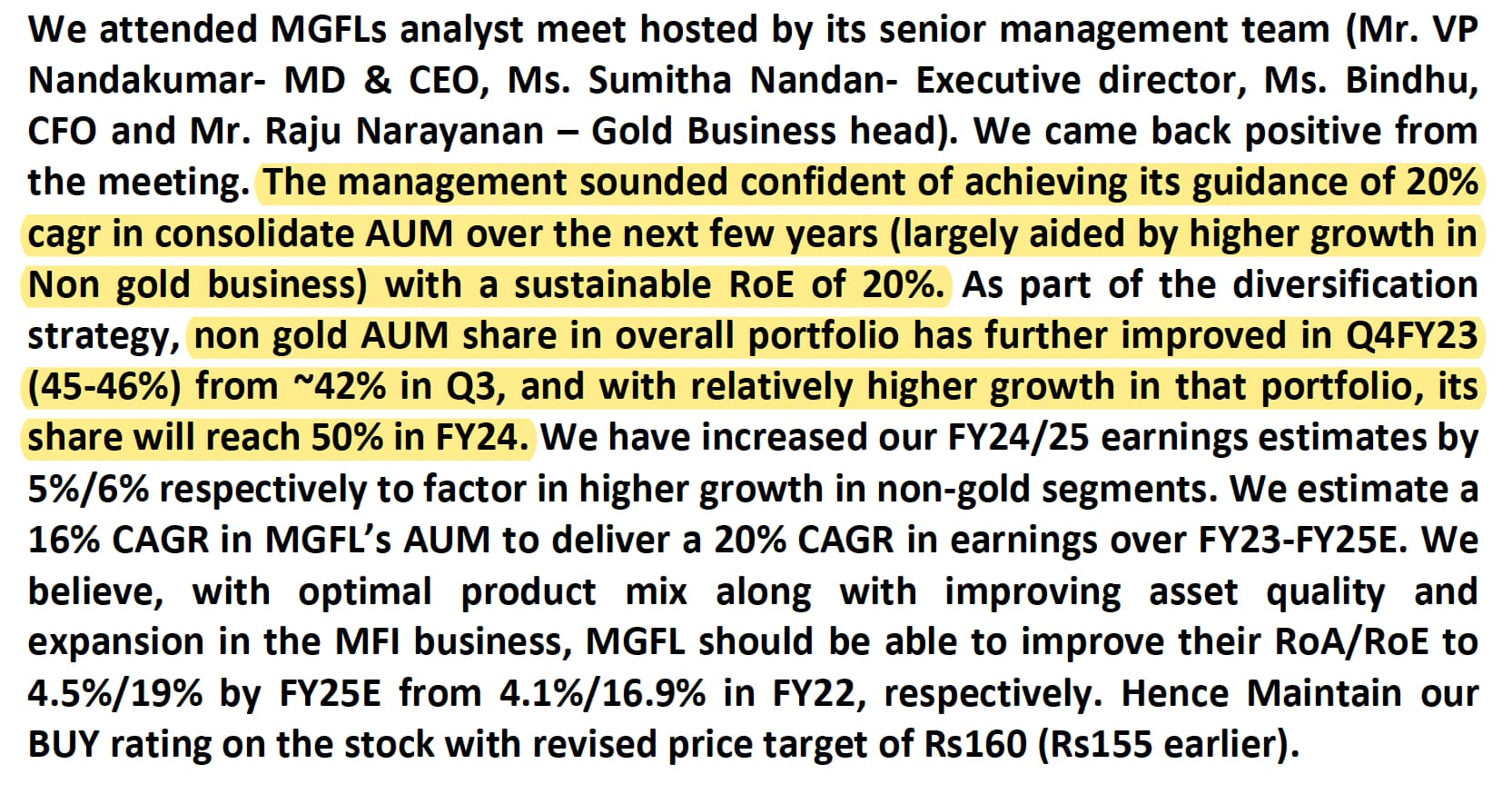

Two strong reports after analyst meet mentioning about rerating possibility due to expected 20% CAGR with 20% ROE and establishing as well diversified NBFC

Gold is becoming increasingly popular as a safe-haven investment due to economic uncertainty

While it’s unlikely that any single asset will replace the US dollar, diversification into alternatives like gold and cryptocurrencies is on the rise.

This trend could lead to high gold price and so more opportunities for gold finance companies in India as there are many households with significant amounts of gold and many needs instant money

It’s better to take gold loan rather than selling gold to get money ,you might pay high interest but in long term it pays off

So even if one has to pay high interest rate it’s better to hold the gold and not sold the gold to save interst on gold

loan

Some economies like Brazil and Saudi are showing some preference to trade in alternative currencies like the Chinese yuan, which may not weaken the value of the US dollar but is creating some question mark on US dollar in some people’s mind

In 2006, the price of gold was under 10,000, and it has since increased five-fold, resulting in a 500% return. If someone took a loan at 20% interest in 2006, the additional payment would only have been 2,000. However, if another person sold their gold to avoid paying the 20% interest, they would miss out on any future gains from the rise in gold Considering the current scenario, I believe gold loans will continue to be in demand in India.

Manappuram, being a prominent player in gold and microfinance, has a great opportunity for growth. With the company’s current price trading near book value, there are interesting times ahead.

From a technical perspective, the current price is close to its resistance point. If it crosses 126, it may indicate the beginning of the second leg of the rally.

Interst rate was around 19% in 1981, during a period of high inflation and economic uncertainty now if similar situation happen of bit higher interst rates than we can see high gold prices

In 1981, the price of gold started at around $590 and increased to around $712 by the end of the year.

Technical news

The underlying theme now is that Manappuram is moving from a gold NBFC to a well-diversified NBFC, Also there is momentum in gold in the background of economic uncertainty and questions regarding the US dollar’s status as a universal currency with some people diversifying in alternate things like gold and crypt of with added advantage of near book vskuations

Positives -

high gold price

Moving towards well diversified nbfc

Coming out from low base

Ashirwad microfinance showing good growth

Strong brand value

Good management

Positive cash flow

Cheap valuation

Strong network across India

Negatives

Slow economy

New player in non gold segment

“We are planning a big marketing campaign after all the products get launched. In the coming years, we expect at least 30-40 percent growth in our business. Our vision is to become one of the top 5 Insurance Broking companies in the next three years,” concludes V.P. Nandakumar, Chairman of Manappuram Insurance Brokers.

Insurance broking is highly competitive space. Everyday some new startup is coming up in this space. Moreover, most of the banks and NBFCs are also jumping in. Is it really worth it?

they alredy have their thousands of branches the reach no online only broker or bank can ever have in the rural/semi urban areas… there is very little added cost to runnign this business for manppuram as per my understanding…

Bank vs nbfc vs unorganised sector

Interst rate banks < NBFC < Unorganised sector

Dominant lender is still unorganised sector inspite of highest rate

Everyone has a role in diverse population with diverse needs

High gold prices effect will be seen soon

Gold vs US dollar

Can us dollar sustain its dominance as universal currency and how long everyone will accept as universal currency

Can gold or crypto be seen as semi alternative

Gold is back in picture due to uncertain economy ,recession,Us dollar dominance ,hunt for alternative

Now general consensus is everyone should have some gold

Yea, this is the big question. Whether this is political or not, if political it could go nowhere. But if its not political, could mean big trouble for the company.

150 crore accusation

That’s ridiculous

Such a big company with 400 cr quarterly profit won’t do any thing for 150 cr

Looks more political stunt especially as it’s in one particular state

Came to know about the ED raid from the thread, checked the fall, a 12% is big, so wanted to take a position purely based on the fall. Checked the chart, the fall looked more pronounced with a big red candle, couldn’t bring myself to buy, as except for the basic understanding of the business, I don’t follow the stock closely, also the price is also around 52W high, so not a wise bet if it falls more, also wouldn’t have bought much even if I had bought, so dropped the idea altogether.

Already having a position and looking at the current status is one thing, and initiating a position under these circumstances without a plan is another.