I think he was talking about standalone. Hence said 85% gold loans.

Has Manappuram Finance given corporate guarantees to loans taken by Asirvad Microfinance?

Can someone throw more light on the issue?

I checked the annual report of Manappuram and did not come across any such disclosure

In particular, I checked the following

- Loans given to subsidiaries (Note 61)

-

Related Party Transactions (Note 42 to standalone statements)

-

Contingent Liabilities (Note 41)

1 Like

Investment Rationale

According to the brokerage, there is minimal asset quality risk in Manappuram’s business as gold loan has a huge share in the total loan portfolio.

The brokerage expects the asset quality in its MFI business to deteriorate materially in the near to medium term.

2 Likes

Banks & NBFC are new sectors for me, so trying to understand business models,

I have few queries request experts to help me out,

as gold is their liability & not asset,

- What happens to stock price when gold rates go up?

- what happens to stock price when gold rates come down?

1 Like

Finding a relationship between stock price and gold prices is a futile exercise. Instead, you can scroll through the thread to understand what happens to the gold loan business when gold prices go up or down.

1 Like

Naveen Kulkarni, Chief Investment Officer, Axis Securities Ltd likes ICICI Bank and Kotak Mahindra Bank look attractive. “In the NBFC space, Manappuram Finance looks attractive. Apart from BFSI, our key focus sectors are FMCG, IT, Pharma and Telecom,” he said.

30% of their folio is into MF and Vehicle finance. MF can go for a toss. Did CARE mentioned anything on the same. Can you provide full link to the doc

Demand for gold loans may rise in the aftermath of the lockdown as the risk profiles of borrowers deteriorate and lenders become risk averse,” V.P Nandakumar, managing director of Manappurram Finance, said in an interview. “With many non-bank finance companies facing liquidity challenges, lending will be further constrained and gold loans may then become the fall-back option for borrowers denied access to their regular channels,” he said, adding gold loans may grow 10% to 15% this year.

About 1.2% of India’s total gold stock has been pledged as collateral for loans, leaving huge potential for the market to grow, consultancy firm Cognizant said in a note in January.

4 Likes

As per last annual report. Covid has created problems but looking at this level of C.A.R in MFI segment it does not look as Manappuram should face liquidity / solvency issue.

Max articulated risk in MFI space may be that’s why stock dropped hard in recent carnage.

Only time will tell

2 Likes

Another Insider Trading violation episode. This is the 4th time, 4 new offenders added to the list. Still all 1st time offenders, small quantities.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3ea3fd0b-2833-4808-ac47-44109fab7221.pdf

With respect to solvency issues in distress times.

As per 2019 (old) Report. Gold holdings @ 67.5 Tons. 1 ton approx 410 Cr (Taking 41000 gold rate).

67.5 Tons = 27675 Cr.

Market Cap of the company today 10500 Cr.

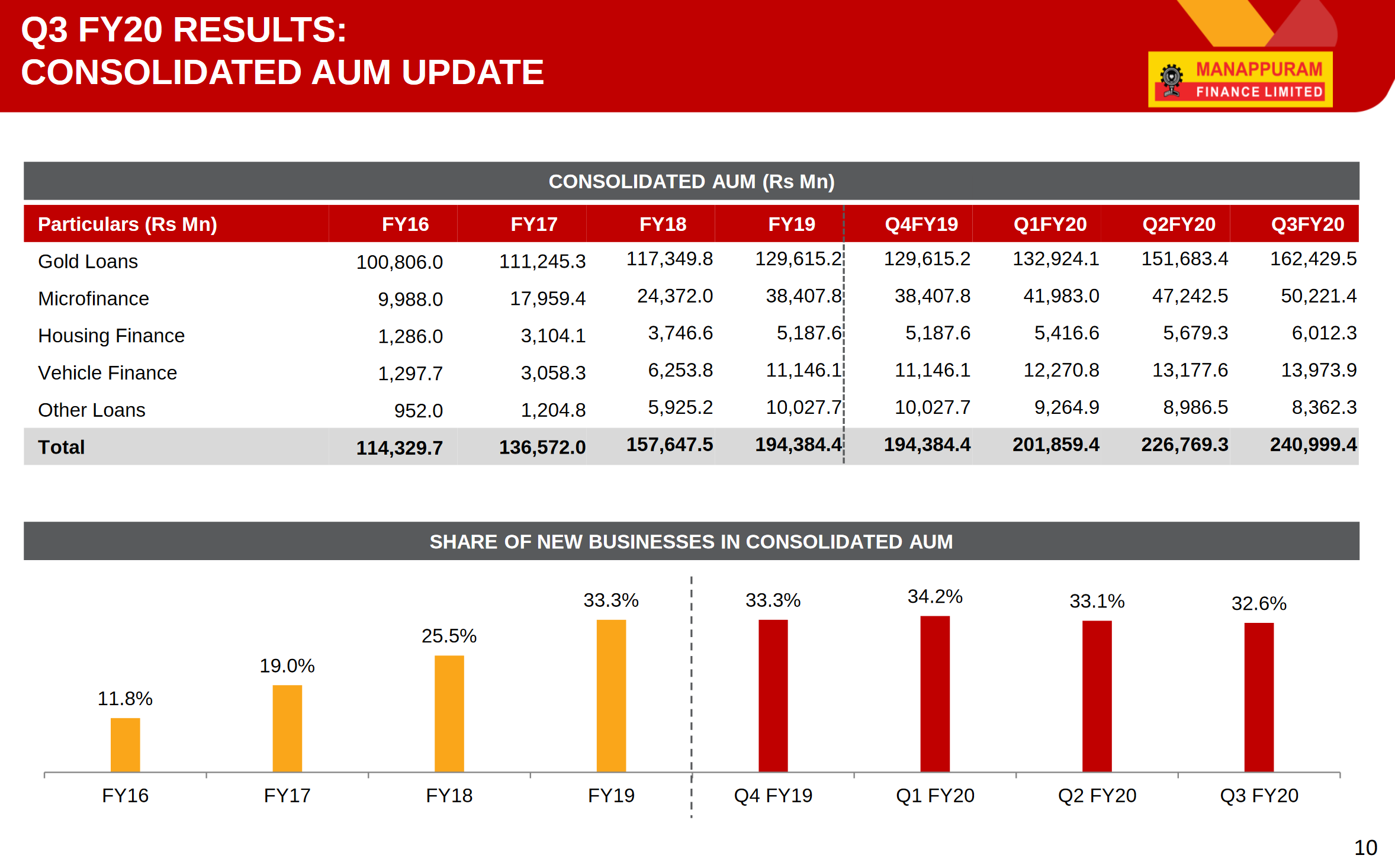

Gold AUM % in Consolidated AUM is 67%

MFI AUM % in Consolidated is 19.5%-20% approx.

Even if the 20% portion of business yields subdued returns for next 2 -3 -4 qtrs. The business doesn’t look like going under as there is ample margin of safety. They should be steady and doing more business 5 years from now. Valuations are one’s personnel assessment.

5 Likes

Would this mean reduced business as customers may prefer to sell to Government?

This is mainly purchase, Usually gold in India has a sentimental value and they prefer to hoard it and pass it to the future generations. So they may use it as collateral to get a loan and then on repayment they get the gold back! But this obviously has a certain impact which I don’t think will be very huge. Last when I read their average ticket size was under 50k, so for such an amount no one would want to get rid of their family gold is what I believe

2 Likes

I recollect gold monetization scheme which was announced few years back without much success. Gold ornaments will be melted and checked for purity and effectively cash in hand is much less than what you paid for jewellery which is big turn off for majority people. Rather they pawn and get money for immediate needs. Unless one has 99.99% purity gold coins and bars which you want to get rid off these scheme won’t make sense.

2 Likes

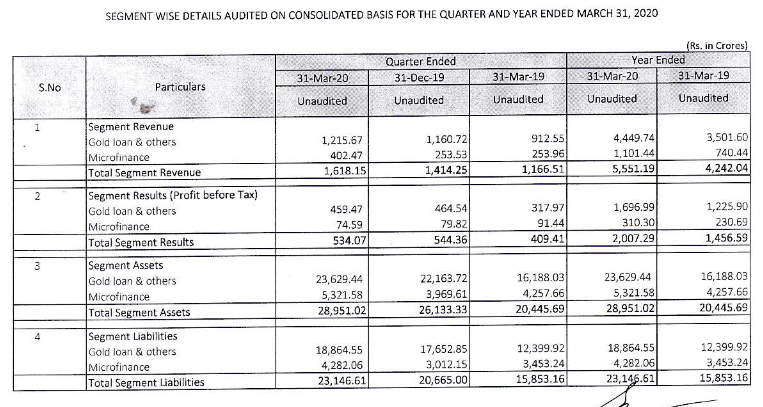

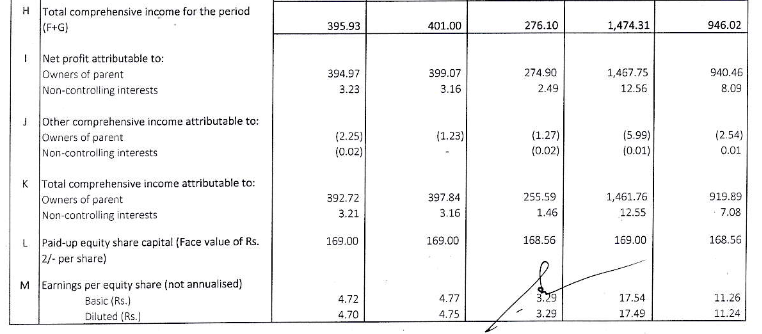

Results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/df326ff1-5f9e-4ba5-a7ed-d1caf7280f7d.pdf

4 Likes

Mannapuram Q420

April 1st to now: disbursals : very high 17,000 cr…as 70% online…and collections…almost all interest in gold loans…hence accrual not much difference. (BULLET repayments)

our opex is lowest in industry …at 5%…we can go down 1% lower (of assets I guess)

Loan guarantee for 75 k cr for NBFCs and MFI’s will help

most of our braches are open

AUM up 29% yoy; 4% qoq ; gold loan AUM grew 4% qoq…and 30 or 13%% yoy on ?

60% LTV…vs RBI limit of 75%. existing buyers have room to boroow more ;

Bounce rate of EMI has been 40-45% in last couple of cycles…; pre covid bounce rate gone up to 80-90%; collection ins vehicle portfolio is 45%

avg loan per customer : 50-55k for gold

Online gold loan 50% of portfolio gone…up 10-12%…collections…improves…ppl love it.

70% of our portfolio will be online by end of the year

we have brought down security cost; technology enabled storage…subsidary 200 engineers…

Ashirwad home finance : 40% yoy and 9% qoq AUM growth

district wise cap of 1% of AUM…now reduced to 0.5% of AUM

we expect short term pain in Micro finance portfolio post morotroium

9.4% incremental funding cost on liability side

brought down dependence on ST sources. don’t except funding challenges…comfortably on ALM

Security costs have come down

we are going to be cautious on non gold portfolio

ROA consol : 5.7% ; ROE : 28% for fy 20

gold loan : 67% of AUM (aum increase 30% yoy and 4% qoq)…79 tons…tons increase 7 tons…down 1.5 qoq) …68

26 lac customers;

most of our customers haven’t taken moratorium

51,000 cr gold loan disburabls ? vs 48,000 cr qoq

online gold loans 48%

Aashirwad home finance : 25% ROE; one of lowest cost providers of MFI in India AA minus by crisil. Q4 : 60 cr; 100% provision on loans above 90 days

CAR : 23%

Book value : 68 rs

we got roll over in CP. 1800 cr 2 months CPs ;

positive response in 100 cr TLTRO

we may get new lines also…first 2 months slow as audits…we are expecting new sanctions

Aashirwvad : only AA- rated MFI in India ; we are good for next 2 months/ quarters ?

CV portfolio : we expect short term pain. 40% customers took moratorium…30% of them came back and paid EMI

Morortoium gold loan biz : very low…less than 5% customers. only 100 customers have taken.

After lockdown first reaction to redeem the gold. volume will be same. Gold loan is for fast hassle free quick loan

90% of branches are optational

loan growth guidance we should continue with ; fy 21 : 10% growth in gold loan we should achieve. this year overall growth could be 10%. we have lost 1-1.5 months ;

we expect no growth in non gold segment. we will focus on collections. will be reduction in portfolio.

Gold loan growth : 10-18% usual plan…

1/3rd of the year is lost. balance of the year can grow 10%

Gold loans are bullet payments….out of 2.6 mn customers…only 100 have asked.

o loan tenure of gold loan is 3 months

In aashirvad we took 1% of loans as covid provision

in standalone we took 15 cr….this is for vehicle finance

FOR GOLD finance NPA will not go up drastically…small spike…in 1-2 qtrs will get platueued. given gold price has gone up…borrowers LTV Is down…so don’t have to give as much interest

fy 20 :

we were disbursing 700 cr every day even during lockdown ; 50% of gold loans is online. volumes were high

Vehicle portoflio : Our customers mainly retail…businesses are local, intra state, intra city; 10% of customers opted for morotoroium; 60-70% of collections thru online…own app…couple of months pain…; out of 1500 cr porfoltio 300 cr is 2 wheleers

in MFI portfolio : our NET NPA is zero….fully provided above 90 day NPA. we write off everything above 90 days…so didn’t take any provisioning…we have taken advances

our branch AUM avg is 4.5 cr…we can go to 15 cr without adding opex

we give free storage to customers

we have 24 hour gold loan anywhere. we don’t do wide publicity. we plan to use digital mode

IN lock down out of billing we could collect 45%…due to digital in APRIL.

o in May we should get 60%

in NON GOLD : None of the cos have disbursed in last 2 months…entire industry is watching in June…what will be collections/repayments…in MFI…0.5-0.75% concentration district level

9 Likes

Got few queries from my friends circle regarding Bajaj Fin entering gold loan segment and its impact on Manappuram since they know that I am betting on Manappuram. Thought of sharing my thought process for my own benefit and knowledge sharing. Views are welcome.

Who are customers for gold loan?

- Non Salaried

- Agri / Rural

- Small vendors / business

When gold loan is opted?

- Medical Exp

- Educational Exp (Term fees, Sem Fees or Joining Fees)

- Agri inv needs (Fertilisers, machinery rent)

- Personal exp (Festivals, Ceremonies (Mrg, Death, etc))

- Short term needs. For eg, a lot would take jewel loan when housing load approval is delayed to avoid halting work, they typically pay back when the loan is sanctioned. Similarly farmers would take gold loan, when the agri loan is delayed.

- Anything else

Nature of Gold load customers

- My dad worked in PSU bank in tier II town, when I visit his branch (which I do so often during college days) I sit aside gold appraiser whose counter was in the backside of bank. I am recollecting my memories below to give a picture about the typical nature of gold loan customers. General questions I heard from the are

- How much I get for this jewel?

- How much I have to pay every month?

- How long will it take to get it back when I have money?

- Rarely you would hear a question about interest rate? Most times the appraiser wouldn’t tell the interest rate and simply communicate the interest they have to pay per month.

- Several customers would rotate their loans. Every X months they pay the money, take back the jewel, and keep it back the next day.

- The appraiser generally visit the bank 3 days a week and would be quite irregular as he is not in the payroll of bank. You can see frustrated customers when they get to know that they can mortgage it only on the next day. Sometimes they would get disappointed when they get to know that appraiser is un-available and they can’t take back the jewel on that day. Once a customer fought in the branch saying that she has to attend a marriage in next two days and she needs the jewel badly.

Would Bajaj impact Manappuram?

Did HDBFS impacted Bajaj Finance significantly in consumer durable lending? Also, in the case of gold loan,

- Manappuram and Muthoot are still struggling to grab bigger market share from un-organised players though their interest rate is lesser and gold security is higher than the later

- Banks are still lagging behind goal load NBFCs though their interest rate is lesser and gold security is higher than the later

Alike above, it is going to be very difficult for Bajaj to sweep the gold loan segment. There will impact on Manappuram but I don’t think it would be significant but only time can answer this. In any consumer facing industry, when a new strong player enters, (1) segment could grow faster than before and (2) existing players could lose market share. Impact on existing player depends on how (1) and (2) plays out.

Disc: Manappuram constitutes ~20% of my portfolio holding at an average price of ~90

18 Likes