The fully hedged international funding will cost approx 11 percent

I wanted to highlight that Euro funding cost is higher than some of the other Indian companies and also to show that cost of funding is higher than that of INR funding

The fully hedged international funding will cost approx 11 percent

I wanted to highlight that Euro funding cost is higher than some of the other Indian companies and also to show that cost of funding is higher than that of INR funding

Coincidentally, CNBC asked the question in Manappuram live call going on right now.

The question was that the cost of $ borrowing is effectively 200 bps higher so why did they do it.

The answer was that they wanted to have buffer given the liquidity scenario in NBFCs, even though they did not face the challenge.

I personally did not find it convincing enough that pricing of 200 bps higher should be agreed in that case.

He also briefly highlighted the MFI business challenge from some politicians in south but is expected to resolve soon.

Someone can pull up CNBC TV18 feed from around 9.45 am today 29 Jan 2020 to view the interview

We are underestimating the reach, comfort level and confidence that this action will create in the medium to long run with international investors. The funding will form less than 15% of the overall borrowings and the hedging cost will have only marginal impact on the profit.

They are exposing themselves voluntarily to the international market and its a learning curve - Manappuram will have no choice but to adopt the best practices both in terms of governance and operational controls. The faster they adopt the best practices, the credit rating will start reflecting them which will in-turn help them to issue better priced bonds to pay off the current bonds.

I’m sure we all want Manappuram to adopt the best standards and also like it to be acknowledged by the international market. I believe the benefit of this action will slowly start reflecting in the earnings multiple that the stock will command in the medium term.

Thanks,

AJ

Disclosure: Invested.

So this year, manappuram is growing at >30% bcs of rising gold rates. This will continue for next two quarters bcs of smaller base. Then, assuming gold stays where it is right now, their tonnage rate is just about 10% around, so gold loan sales will grow only 10%. Comments???

Rest of their business is 37%, including mfi,cv, housing etc., it would reach about say 45% by next two quarters. This part i believe will continue growing at 30%+, so overall growth after two more quarters would be <20% (55% gold pf at 10% and rest 45% at 30%)… comments???

They would continue posting 400 cr+ Profits for 2 more quarters and hence PE will become 10 at yearly profit of 1600 cr (400*4) aftet 2 more quarters.

At PE of 10, with growth rate of<20%, how would it look post two more quarters??? Views…??? I find it has more stock price rise up ahead…

Thanks in advance.

Just a word of caution:

If i understand the business model and comments from Mr. Nandakumar correctly - the growth for the current quarter is to be understood in context - most investors in Manappuram are not the ones who have ever availed a loan from this company and it is for a reason - its the poor and marginalized who do not access to bank loans and the ones who have unaccounted stashes of gold(expected to be only a hand full) are the ones who approach companies like Manappuram and Muthoot for a loan. The recent crisis in the market made it even more difficult for the bottom of the pyramid to avail loans even from micro finance companies - and naturally a lot of the micro finance customers would have gone to gold finance companies for loans. So i don’t believe the growth for the current and previous quarters should be extrapolated.

Mr. Nandakumar keep stressing on the above aspect in most of his calls and tries to keep the growth expectations low. Manappuram’s organic and sustainable gold loan business drivers will primarily be branch expansions to newer geographies and rise in gold price.

Thanks,

AJ

Disclosure: Invested.

Expecting and hopeful of 5% growth in q4 and 20% in fy21

Gold loan price increase and volume growth has helps in growth this quarter

Expanding in non south states where gold finance competition is less

Some areas of Microfinance have local political issues and may take a hit of 20cr as provisioning in q4 if issues get unresolved

International funding cost is high but when combined with domestic funds ,margins won’t be affected much

Nirmal bang : The brokerage retained a ‘buy’ rating on the stock with a revised price target of Rs 218 (Rs 207 earlier)

. ——increase price target to Rs 213 and change our rating to ‘buy’,” Narnolia Financial Advisors

You have raised valid points… One more thing to consider is that these foreign funding agencies conduct a rigorous due-diligence of the organization before considering them for loan… These include business practices, corporate governance issues, financials etc among other things… So, this kind of gives confidence about the company and its business…

Invested in Mannapuram

Dividend tax gone .Extra 30 Crore profits per year for Manappuram.2% extra income ![]()

Baring Private Equity selling their stake

According to a Bloomberg report, Baring India Private Equity Fund II is offering 42 million shares (5 per cent) of the company in an accelerated book-building with a floor price of Rs 172 per share, which are at a discount of 6.57 per cent to the last closing prices. As on December 31, 2019, Baring Fund has 8.76 per cent stake or 74 million shares in the company, the shareholding pattern data shows.

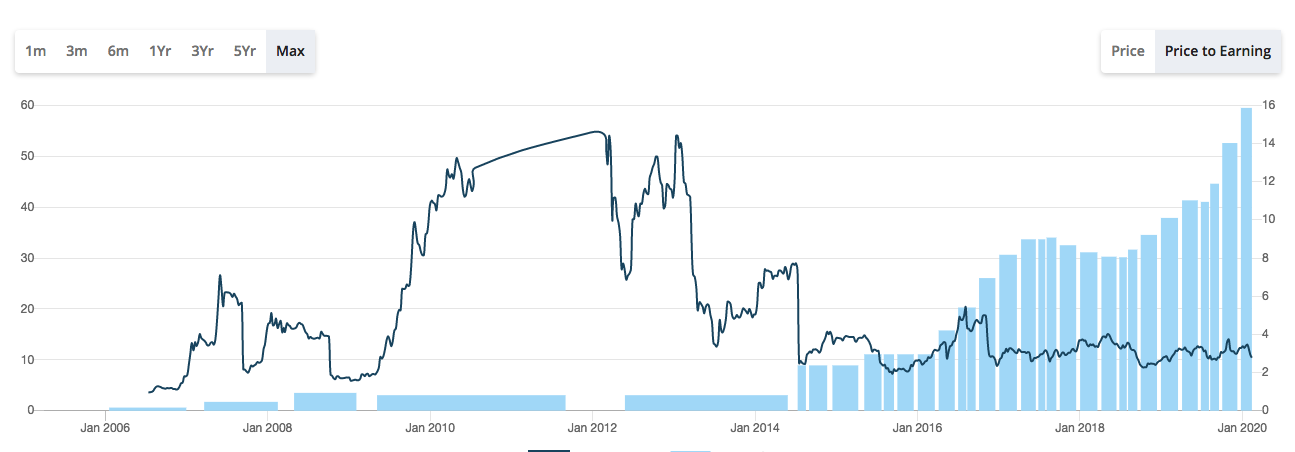

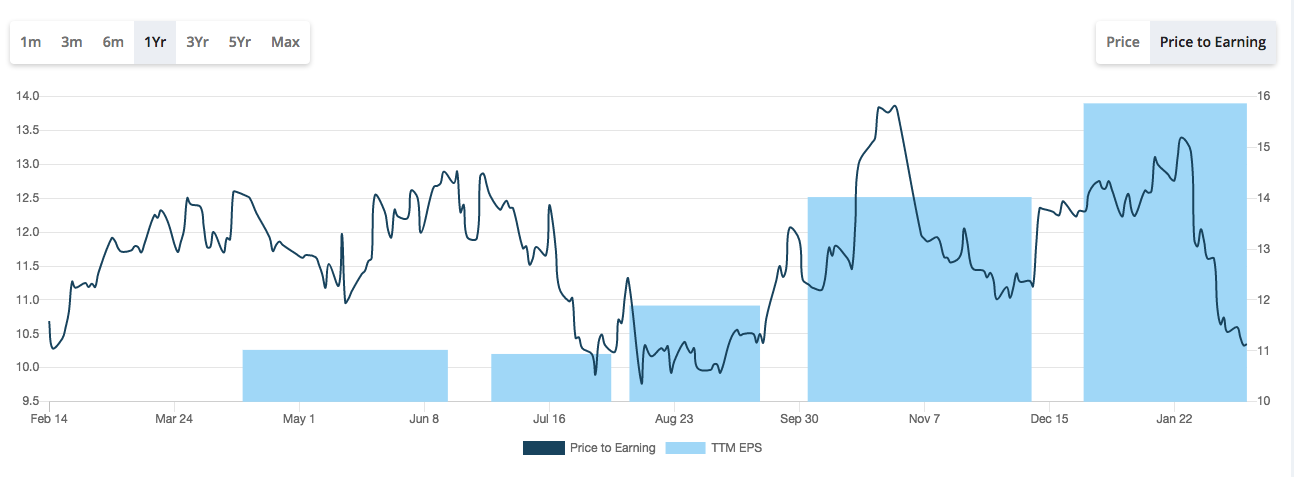

Despite posting solid earning and growth, the Market seems not to be willing to rerate Manappuram leaving it a current 10.6 pe. On the contrary, the market has lowered the rating a little. Is there something missing in our analysis as it seems the company has and will do well.

Thoughts and opinions very much sought…

Thanks

https://www.icra.in/Rationale/ShowRationaleReport/?Id=92457

Asset quality risks and forward looking statements (micro finance) in credit rating report. An interesting monitorable in future.

I have a question on gold finance business.

It almost ticks all the parameters, then why is market not giving it a high PE?

I believe markets perceive that gold loans have an inherent risk of accumulating high NPAs if there is a sudden crash in gold prices… that is why gold loan companies usually do not trade at high multiples…plus microfinance business is prone to risks in case of any major incident like floods or demonitisation etc…, however manappuram has been diversifying into other businesses well and sooner or later rerating will happen . Disc : Invested at lower levels and adding at regular dips

Manappuram finance

Key takeaways

Guidance:

Medium-term growth guidance of 20% and RoE of 20% plus.

Aim is to achieve 50/50 split between gold and non gold (equal contribution from

MFI, CV and MSME).

Business growth and operational metrics:

Online Gold Loan (OGL) model is an important focus area, which now accounts for

43% of gold loan book.

Door step gold lending started on pilot basis in four cities and will roll it out from

150 locations gradually.

The company is also trying to control operating expenses and bring in cost

efficiency.

o Under OGL model, customers will not have to visit branches, which helps

takeaway crowd at branches. Though gold loan is growing, there is no need to

add employees.

o Also, security cost was down from INR1.6bn to INR420mn; guard cost is in the

range of INR25,000-INR30,000 per month with three guards per branch.

MFI segment is facing problems in one district in Assam (INR1bn portfolio), in two

districts in West Bengal as well as two districts in Karnataka.

o In Karnataka, its exposure is INR400mn to Mangalore and Udupi on which it

has provided 40%.

o Assam has 4% exposure with collection efficiency being 98.5%.

Breakdown of RoA:

IMO the biggest risk with gold loan companies is theft and regional disturbances as most of business is focused in south. Not sure if theft portion is insured.

The loan which manappuram gives is very short term (3-4 months) and that too 60-70% of collateral value. The probability of gold prices falling 20-30% in span of 3-4 months is extremely remote.

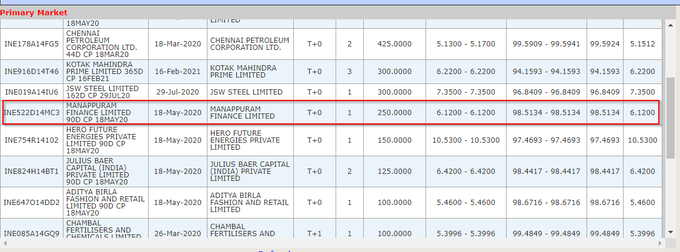

Manappuram just raised 90 day CP at 6.12% - that’s quite a bit lower than the 8.5% odd it was raising at a year or so back.

Board of Directors of the company will be meeting on Thurdsay,27th February 2020 at the Corporate office of the company, Mumbai- 400093 interalia to consider declaration of Interim Dividend.

2nd dividend in two months…

impact of DDT. dividend received will be in this fy, instead of next FY. same with bajaj finance and finserv.