https://www.icra.in/Rationale/ShowRationaleReport/?Id=77707

Very nice credit report

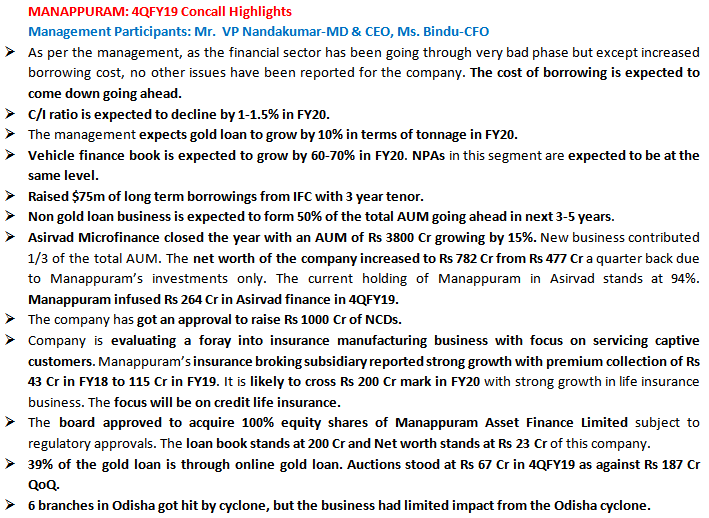

The board approved additional infusion of Rs 120 cr into the Microfinance subsidiary.

Interview with md Nandakumar

Expecting 20% consolidated growth

Stock trading at around 11 PE

If we give modest Pe of 15 -20 then rerating is possible

Intimation of Acquisition under Regulation 30 of SEBI (LODR) Regulations 2015

Please be informed that the Board of Directors at their meeting dated 20.03.2019 accorded their approval for acquiring 100% equity shares of Manappuram Comptech & Consultants Ltd and to make it a wholly owned subsidiary company of the Company.

Material Details regarding the Equity/Proposed Acquisition as per SEBI Circular

Nandkumar:

Microfinance business Ashirwad grown at 40-45% last year

Expecting to grow at same rate this year

It needs capital to continue its momentum

We have invested 264 cr which brings our stake to 94%

Banker is appointed to raise capital 100 million dollars from private equity by end of second quarter

Ashirwad Expecting to grow to 10th Crore in 3 years

Currently 25% of portfolio in Tamil Nadu

7 Lac customer base

We want to get in sme loans (which will be co laterally backed by lender properties )from early second quarter

By 2020 gold loan will be 60% as non gold loan portfolio growing at decent rate

Over next 3-4 years gold loan portfolio will come to 50%

This year expecting 10-12% growth in gold loan

Recents cuts 25+25 will bring down our cost to 80 bips

No slowdown in lending by banks to us

From NABARD we got around 700 Crore

We expect international finance Corporation to lend us 500 Crore

In the past six months, the market price of manappuram has surged 73 per cent on the back of foreign portfolio investors (FPIs) buying.

Manappuram and muthoot least affected by liquidity crisis

Steady set of numbers from Manappuram yet again.

See the presentation for the quarter below:

Result presentation

Q4 Result

Quick updates from the Concall:

Ashirvad valuation - Recently Manappuram infused about 264 Crore as additional equity into Ashirvad MF valuing the business at 2.2 times the book value. With the closing book value of Ashirvad being 782 Crore the value of the company roughly translate to Rs. 1700 Crore.

Branch expansion - Company is planning to open about 150 branches during the year 2019-20.

Insurance business foray - Currently Company is collecting third party insurance premium of about 150 Crore from its gold loan customers. Company is planning to start an credit life insurance company to bring this business inhouse. Total investment expected in this venture is about 200 Crore.

Acquisition of Manappuram asset finance company - The idea is to avoid conflict of interest considering the business is run by the same promoter group. The current loan book is less than 250 Crore and the book value is about 60 Crore. Mr. Nandakumar did not disclose the valuation assigned for this business.

Disclosure: Invested

Great results

Q4 FY19 RESULTS

+23.3% YoY and +9.3 % QoQ consolidated AUM growth

5.2% consolidated ROA, 23% consolidated ROE

+42.8% YoY and +4.7% QoQ consolidated Net Income growth

Standalone GNPA has declined to 0.5% in Q4 FY19 (vs. 0.6% in Q3 FY19 and 0.7% in Q4 FY18

Link to management interview , held today

No divident declaration by Manappuram??

They keep paying interim div. per quarter. What else you are looking for?

Sent from Economic Times Mobile App.(Download Now):

http://ecoti.in/etapps

"Manappuram has been immune to the ongoing liquidity crisis given its ALM profile and robust profitability

In our view, it will continue to act as a ‘safe haven’ with stable business trends and an undemanding valuation (8 times P/E and 1.7 times P/ABV on FY21 basis)," said the brokerage.

consolidated AUM is expected to witness 18-20 per cent CAGR over FY19-21