MFS’s debt issue is fully subscribed for the minimum amount of 200cr now let’s see if they could garner 1000cr by 22st Nov.

Not sure what’s this about and almost 5% drop today

May be due to the sensex which cracked today

Regulation 29(1)(d) of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (Listing Regulations), we wish to inform you that the meeting of the Financial Resources and Management Committee of the Board of Directors of the Company will be held on Tuesday, December 11, 2018 inter- alia to consider and approve the issuance of the Private Placement of Unrated, Unlisted, Secured, Redeemable Non-Convertible Debentures.

May because they could not raise the required amount from their public ncd, hence going for private route for raising funds

Probably it fell showing sympathy with Muthoot after it reported average set of standalone Q2 nos. I think Manappuram should show out performance now after blowout set of Q2 nos.

Asirvad reached 3000 cr aum . Having incremental growth of 100 cr every month for past 5 months. to reach 3500 cr by year end

Ashirvad microfinance securitises Micro Finance Portfolio

Came across this article here that mentions an IPO for Asirvad Micro Finance subsidiary of Mannappuram. Can veterans of VP throw some light on how this would impact shareholders of Manappuram itself? Asirvad has been recently doing well and an IPO would mean dilution of stake for Manappuram - OR would this be something like a de-merger and shareholders of Manappuram would receive additional shares of Asirvad?

Well, I have heard that Mr. Nandkumar is unwilling to exit gold loan biz which is a kind of cash cow. There are many who wanted to buy it though. Sentiment towards well run MFIs is improving after Indusind’s acquisition of Bharat Financial and now HDFC’s financial interest in Bandhan. It seems that he would like to monetise MFI biz at some point of time and focus on Gold, Vehicle and housing. In the long run he would face pricing pressure from SFBs and better to prepare accordingly. FYI, Mr. Nandkumar is a veteran of commercial vehicle finance and exited this biz reluctantly only during NBFC crisis of late 90s. I am sure he would build it again. For the next few years MFI will be a growth engine but it is better to focus on secured lending i.e. Gold, Vehicle and home finance in the long run

Expecting over 20% consolidated growth

Great Q3 results:

Q3 presentation:

Highlights:

- Consolidated AUM growth: 3.4% QoQ 21% YoY

- Consolidated Net Profit: 10.3% QoQ 41% YoY

- 5.2% consolidated ROA, 23% consolidated ROE

Gold Loan:

- AUM up by 10.6% YoY and down by 0.5% QoQ

- Gold loan growth impacted by seasonal lumpiness in gold loans market, Gajacyclone and changes in certain operational processes

- Improvement in gold loan net yields from 25.0% to 26.3% due to (i) full quarter impact of withdrawal of discount schemes in the last quarter, and (ii) yield optimization to pass on the increase in cost of funds

Asirvad Microfinance:

- 51.3 % YoY AUM growth, 29.4% ROE

- Plans to raise funds from PE to achieve targeted growth in the business

Other highlights:

- Q3 FY19 was the first quarter when all of the lending products reported profits on a standalone basis

- Security costs have halved from INR 44 Cr in Q3 FY18 to INR 22 Cr in Q3 FY19

- C/I ratio in the standalone business has improved from 36.8% in Q3 FY18 to 32.9% in Q3 FY19

- Did not face any significant liquidity stress during Q3 FY19. Undrawn Banking lines Rs 19,240 Mn

Really impressive result from Manappuram. I think the biggest take away is a note give in the investor presentation which says "Plans to raise funds from PE to achieve targeted growth in the business ". While it is not clear whether this is going to be done at the parent level or specifically for Asirvad at the subsidiary level - it is really interesting, as any fund raised at a parent level will give us the kind of valuation multiple a PE is ready to place on the listed entity and if this is done at Asirwad level then that is a clear sign of them listing this entity in the near future.

Disclosure: Invested.

AJ

Having begun its diversification in 2014, the company is well set to reap the rewards from here on.”

What about asset quality ? I don’t see asset quality in results.

Investor Presentation has it(only stand-alone figures). You can refer to it.

No meaning of seeking defaults in gold loan. Once they declare loan assets in other areas, they must declare defaults too. Without looking for NPAs , no meaning to asses profit loss account sheet of finance company. Any profit can be declared by playing on provisional coverage ratio.

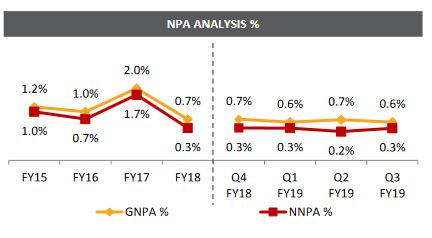

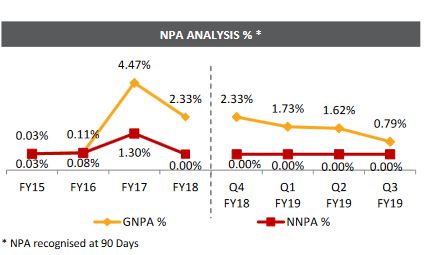

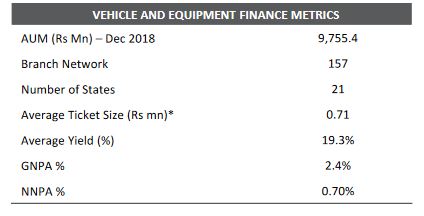

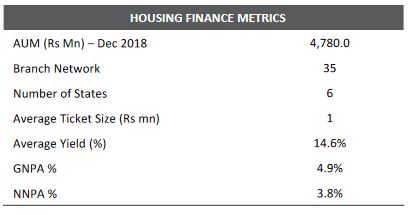

Investor presentation has the NPA numbers:

Gold loan:

Asirvad Microfinance:

Vehicle finance:

Home loan:

Thanks, I missed it.

Manappuram Finance Ltd

Highlights Of Q3 FY19 and Nine Month FY19 Results

Financials

-

Consolidated

- AUM grew by 21 % to 17,783 Cr compare to last year same quarter and 3.4 % QOQ.

- Income from operations was Rs 1081.2 Cr an increase of 6.6 % QOQ and 24 % YOY.

- Net Profit stood at 244 Cr compare to 221.4 Cr preceding quarter an increase of 10.3 % QOQ and 42 % YOY.

- ROE stood at 23.02 % annualized for the quarter ended 2018

- Gold holdings were at 6.3 ton the holding is decrease by 1.58 % QOQ and 6.4 % YOY. Total number of gold loan customer stood at 23.8 lakh . Gold loan book is at 25223 Cr which was up by 10.6 % YOY.

- Auction during the quarter were Rs 187 Cr

- Weightage average LTV stands at Rs 1890 of 65 % of the current gold price.

- Gold loan disbursement during the quarter were at 21028 Cr compare to Rs 18,337 Cr in Q2 FY19.

- Online Gold loan book is stated which is on account of 36 % of total gold loans.

- Consolidated net worth stood at Rs 4341 Cr as on 31st Dec 2018.

- Book value per share stood at 51.41 of diversify business

- Capital adequacy at the end of Dec-31st was 26.36 %.

- Consolidated borrowing stood at Rs 14267 Cr as on Dec-18.

- Proportion of CP reduced from 24 % to 21.6 % YOY

Segmental Performance

-

Ashirvad Microfinance

- AUM stood at 3195 Cr an increase of 17.1 % QOQ and 51.3 % YOY.

- Registered profit of 33 Cr compare to 29.4 Cr in Q2 FY19.

- Provision of 5.3 Cr for doubtful loss.

- Company provided 19.4 Cr access compare to RBI prudential norms.

- 100 % of disbursement were made in Non-Cash manner.

- Company has 16.66 lakh customers , 928 branches and 4872 employees present in 22 states and 7th largest MFI in the country among the lowest cost MFI in India within the AUM cost of 6.4 %.

- Company had capital adequacy ratio of 18.3 %

- Plan to raise equity in the near future

-

Commercial Vehicle Business

- AUM grew by 95 % to 975.5 Cr compare to 500 Cr last year same quarter

- Double asset quality of 2.4 % DNDA as on 31st Dec 2018.

- It has 157 branches compare to 90 branches a year ago.

-

Manappuran Home finance Ltd

- Reported AUM growth of nearly 40 % to 478 Cr

- It operates in 35 branches and new business contributed 29.6 % of Consolidated AUM.

- Average cost of borrowing during the quarter increased by 48 basis points to 9.37 % which does not impact the margin due to optimization of yield.

- Benefited from significant operating leverage of overall OPEX only grew by 9.8 % compare to 21 % growth in AUM.

- Significant saving in security cost compare to few quarters ago. It reduce to Rs 44 Cr from Q3 FY18 to Rs 22 Cr in current quarter.

- Provision and write off for the standalone entity were Rs 1.4 Cr

- Gross NPA was 0.58 % at the end of quarter. Loss assets to AUM was only 0.4 % of AUM.

Key Highlights

- All subsidiary business contributed 30 % of consolidated AUM

- Average cost of borrowing increase by nearly 50 bps to 9.7 % but in the quarter company was able to pass on the increase cost.

- Despite the tight liquidity company face no difficulty in existing credit lines and new lines of credit.

- In start of the quarter company secure funding of NABARD and in October 2018 company launched public issue of secure NCD. That issue was fully subscribe and company raise about 1250 Cr.

Outlook

- Non gold portfolio would be 40 % in next 1-2 years

- Borrowing cost will be moderated at current level in next six month because of liquidity situation emerging scenario

- Company got license for opening 150 branches in next year

- Target is to double the AUM in next financial year.

- Company expect cost to income ratio to 6 % from 6.4 % current rate