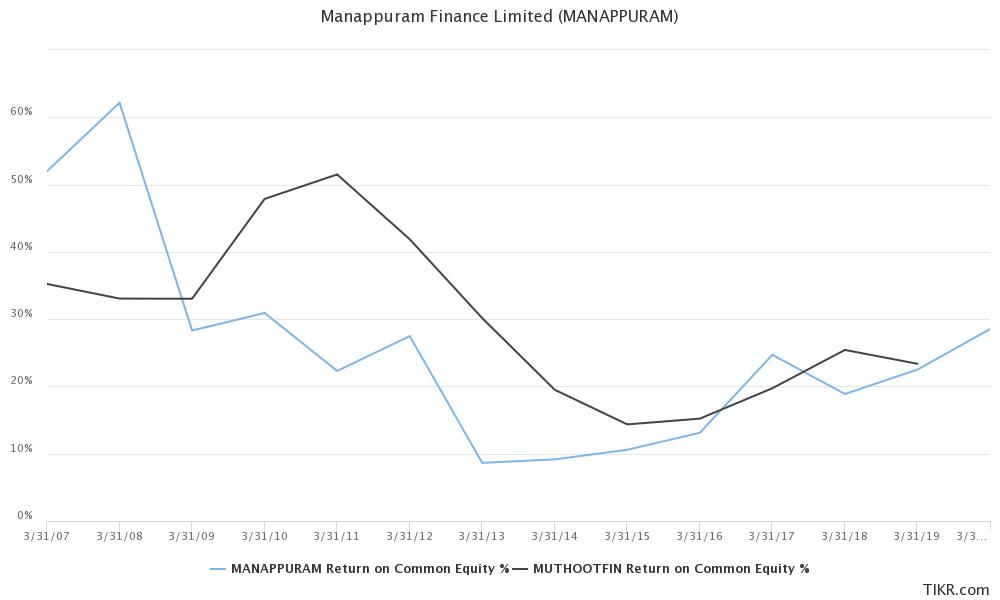

ROE is the bridge between P/B and P/E (PB = ROE*PE). Anytime, P/E looks low but P/B looks higher, it means market is saying that the current ROE of the business is not sustainable i.e. the business is going through a cyclical uptrend. Does this apply to gold financing? Hell yes! ROEs of Manappuram and Muthoot are shown below (taken from tikr).

In the last cyclical downturn, ROE of Manappuram went down to single digits (close to cost of capital) and P/B also went below 1. It will be prudent not to extrapolate 30% ROEs as the inherent business of gold financing depends on gold prices which is cyclical. Over a cycle, this business is still quite attractive making ROEs much higher than cost of capital. But 30% ROEs cannot persist forever.

A good way to play these cyclicals is to wait until market gets excited about them and starts paying a high multiple (>4x P/B) during a business upturn and sell it to the optimistic participant. This has not yet happened for Manappuram because market is skeptical of their non-gold finance lending (vehicle, microfinance) but has already happened for Muthoot (look at PB ratios for Manappuram and Muthoot).

Disclosure: Invested (position size here)