Muthoot gave stellar results (Highest Ever AUM, Profit, AUM per branch) and raised it’s gold loan growth guidance from 15% to 30-35%.

Favorable regulatory changes by the RBI for gold loan sector, higher gold prices and tighter norms for unsecured credit are expected to boost gold loan demand.

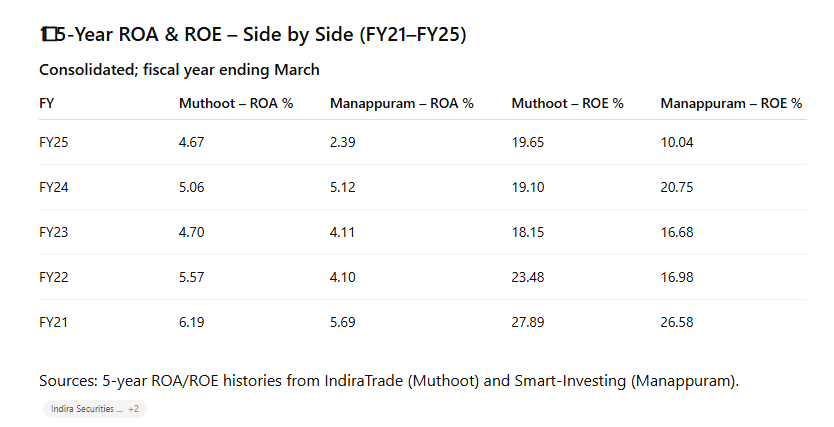

Manappuram is clearly lagging behind in their core GOLD lending business and has lot of catching up to do. Their GOLD AUM PER BRANCH (Rs. Cr) is just 8.6 Cr Vs. 25.15 Cr for Muthoot. This leads to higher OPEX / AUM and combined with higher credit costs (MFI), the ROA and ROE has deteriorated. This is reflected in the wide gap in their P/B valuation.

It is raining gold loan (literally) and they are out there with a bucket. There are clearly many areas where they can improve with such high demand scenario. MFI industry is also seeing signs of improvement which hopefully should end the pain for them. But they have to act fast.

A smaller “number two player” often has a greater opportunity to increase its market share and earnings, which drives massive stock returns -Peter Lynch. (Amara Raja Vs. Exide - 2010 to 2015 period)

However, in this case, staying with the market leader would have definitely been the smarter bet. Muthoot has given far superior return than Manappuram over past few years.

In this case, Hiren Ved’s philiosophy holds true.

Key Point: No investment style or quote by legends hold true in all cases. It is always our personal experiences and biases that shape our thinking.

Can Bain turn it’s Bane? Only time will..

Discl: Invested