-

Coming back to profitability may take couple of further quarters. Will it happen in Q4FY2026, or in Q1FY2027 or further down .. but the pace & amount of provisioning has been reducing for sure.

-

As an investor (hence, a bit biased views) an interesting fact which is getting executed post Bain Capital has taken driving seat i.e. Introduction of qualified finance professionals in Manappuram & it’s Key Subsidiary (Asirvad).

Look at the new jockeys https://asirvadmicrofinance.co.in/management-team/ CEO, Co-Ceo (https://asirvadmicrofinance.co.in/wp-content/uploads/2025/10/Intimation%20_appointment%20of%20Co-CEO.pdf), CFO, CRO, COO, CCO .. all seems with credible finance experience vs erstwhile puppets of Mr. Nandkumar (deputed from Manappuram, to run the show) -

Quarter Ended Sep 2024 was last profitable quarter, now 4 quarter of losses are complete. During this time, Interest income reduced more than 50% (on account of AUM reduction, as well as Yield compression - RBI ban impact), Interest expenses also reduced (on account of repayment of loans), but Provisions increased (on account of bad debt), and fixed cost such as Employee cost just slightly reduced, other expenses (major chunk of operational & administrative fixed cost) also almost same.

-

A year down the line, with a possible change in MFI perception, Magic of Bain acting as base, New Jockey’s building a good new foundation, Increase in AUM resulting in operational leverage - Numbers may look beautiful again.

-

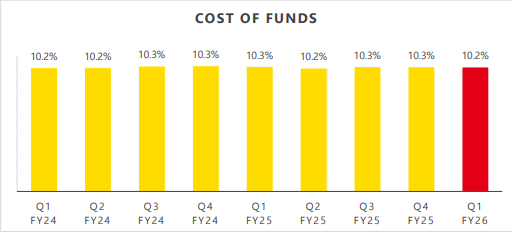

RBI’s 100 bps repo rate reduction resulting in MCLR reduction by bank resulting in reduction of Cost of funds resulting in better net yield. Recently company raised NCD via private placement, with maturity in Aug 2028 - Sep 2028. ROI on these NCD was around 8.7%.

-

Last 2 years blended Cost of funds trend was above 10%.

Growth expected good

Yields dropping

NIM will be maintained with high growth and operational efficiency

Microfinance Will turn around on couple of quarters

New ceo has ambitious plans Will be revealed in coming quarters

Now having lowest interest

- FY26 will remain a transition year, focused on clean-up and restructuring.

- From FY27 onward, non-gold businesses should contribute positively to consolidated profits instead of dragging them down.

- The strong 28–40% CRAR post-Bain infusion provides enough capital buffer to absorb any residual provisions.

Got fully out from Manappuram today itself. It’s wonderful journey from levels of 89 rupees to 289 rupees. I am grateful to this wonderful valuepicker community for this journey of 2.5 to 3 years. I remember the ED fiasco of Manappuram and heard the management concall the very next date. During hearing , I got some sense that ED fiasco is rubbish and management is quite honest.

I called my wife and told her to buy Manappuram with Full force and strength as I don’t have internet reach that day.

As far as my selling rational is that MFI segment of Manappuram i.e. asirwad is in doldrums and will remain so far atleast 2 to 3 quarters. Moreover peak gold price is also not giving me much confident. I am seeing other pockets where valuation is quite reasonable.

Muthoot gave stellar results (Highest Ever AUM, Profit, AUM per branch) and raised it’s gold loan growth guidance from 15% to 30-35%.

Favorable regulatory changes by the RBI for gold loan sector, higher gold prices and tighter norms for unsecured credit are expected to boost gold loan demand.

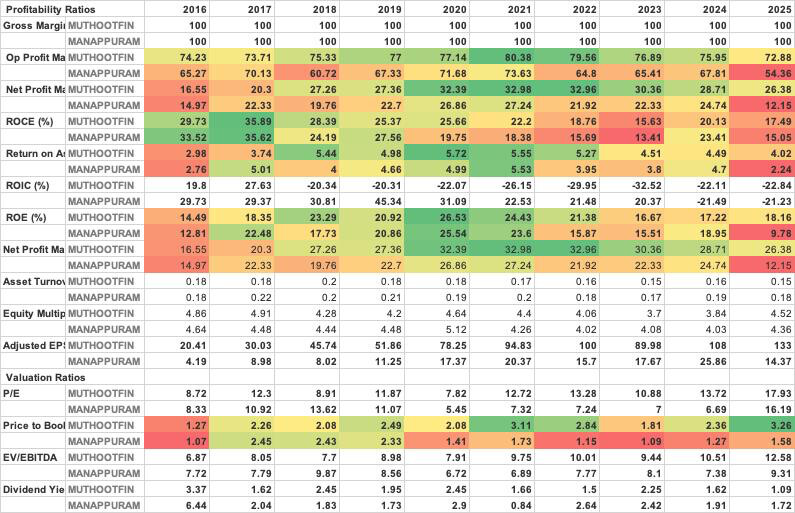

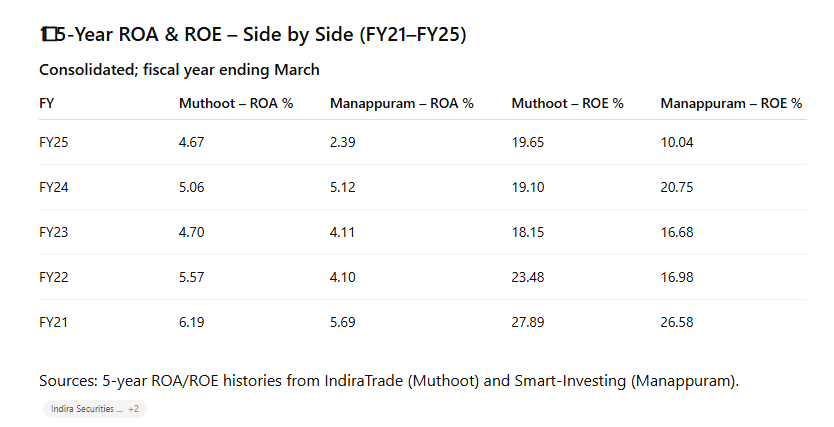

Manappuram is clearly lagging behind in their core GOLD lending business and has lot of catching up to do. Their GOLD AUM PER BRANCH (Rs. Cr) is just 8.6 Cr Vs. 25.15 Cr for Muthoot. This leads to higher OPEX / AUM and combined with higher credit costs (MFI), the ROA and ROE has deteriorated. This is reflected in the wide gap in their P/B valuation.

It is raining gold loan (literally) and they are out there with a bucket. There are clearly many areas where they can improve with such high demand scenario. MFI industry is also seeing signs of improvement which hopefully should end the pain for them. But they have to act fast.

A smaller “number two player” often has a greater opportunity to increase its market share and earnings, which drives massive stock returns -Peter Lynch. (Amara Raja Vs. Exide - 2010 to 2015 period)

However, in this case, staying with the market leader would have definitely been the smarter bet. Muthoot has given far superior return than Manappuram over past few years.

In this case, Hiren Ved’s philiosophy holds true.

Key Point: No investment style or quote by legends hold true in all cases. It is always our personal experiences and biases that shape our thinking.

Can Bain turn it’s Bane? Only time will..

Discl: Invested

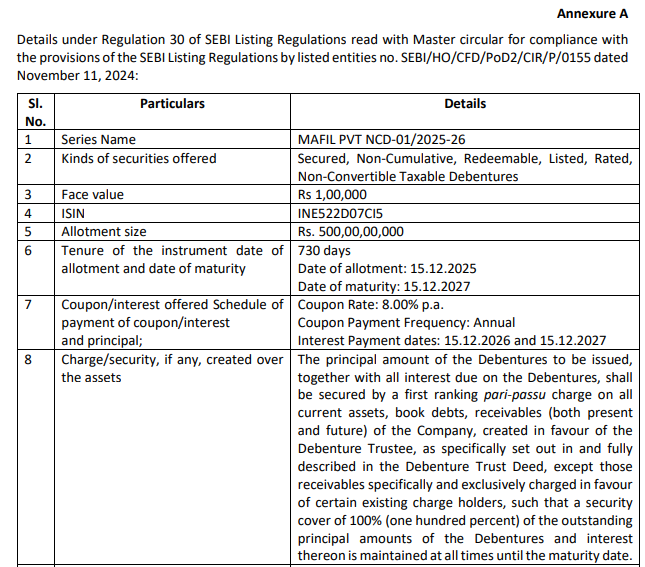

Rs. 500 Cr of Fresh Funds, on 15/dec/2025, raised via privately placed NCDs @ 8%… Seems debt market expressing trust on Bain led management.

Bain plus high gold price playing out well gold could double from here and bitcoin to zero Why Gold Will Hit $10,000? This New Gold Price Prediction Sees the Yellow Metal Doubling[quote=“maheshkumar, post:1871, topic:5328, full:true”]

Bain plus high gold price playing out well

[/quote]

As I go through Q concall, couple of tailwinds

- Gold Price. It’s the days of hard assets. People who predicted , gold price will crash, are severely disappointed. I am not in prediction business, because I don’t know.

- Businesswise, new CEO is at the helm, who has started working and promised to scale up ‘Gold Loan’ business and reduce losses in MFI businenes

- Overall MFI as an industry, is improving across states

There are many other factors..rationalizing gold loan rate

Rerating happens in a company where things are improving from Low RoE to High RoE , where maximum money is made, not where it’s already known…eg Muthoot

I have significant exposure in Muthoot but feel , mkt is waiting for 1 good result…also with BAIN, ultimately , PE player, they will be determined to see, return is there..

Let’s hope for the best..

Agree with @nil_71 .

Mannapuram.is undervalued compare to muthoot . There is no reason that mannapuram cannot grow their gold loan aum by 2x or 3x . They have being in business since long has good reputation and branch penetration and now also have focus.

Even mfi has improved but its much more cyclical than gold loan with a big risk of loss. I am happy that new mgmt is more focussed on gold loan

Wonderful to see, BAIN bringing a full stack of professionals on the ship for interesting onward journey. CEO Reddy is now supported by new Group CFO, Group Compliance officer, Group General Counsel, Co-CEOs in Asirvaad.

Once RBI approval on BAIN transaction is approved, wondering, how long DII’s will still ignore Manappuram as potential re-rating candidate.

xpecting boook valve of 200 and price to book of 3 [quote=“Gaurav_Catalyst, post:1874, topic:5328, full:true”]

Wonderful to see, BAIN bringing a full stack of professionals on the ship for interesting onward journey. CEO Reddy is now supported by new Group CFO, Group Compliance officer, Group General Counsel, Co-CEOs in Asirvaad.

Once RBI approval on BAIN transaction is approved, wondering, how long DII’s will still ignore Manappuram as potential re-rating candidate.

[/quote]

Not Sure of PB 3 times, will it come, and if it → then by when.

But For Sure, Book Value of Rs. 200 / share is not too far.

Almost 4 months ago, had Tried to play with these numbers for self clarity on possible valuation upside as well as downside.

Considering fresh Capital is infused, by BAIN post receipt of RBI approval, by 31 March 2026 → Manappuram at Consol level can have a Networth of approx. Rs. 17,500 Cr (against a total of 103.25 Crores outstanding shares) → Which makes BV approx. Rs. 170/share.

For BV to grow from Rs. 170 to Rs. 200 (organically, and without any further dilution) → Business needs to ear ROE approx. 17% which is fairly possible by March 31, 2027 (i.e. within a subsequent year) considering the past trend of 3 Years / 5 Years/ 10 Years.

Source: Screener.

Another tailwind for MFI is RBI has allowed upto 40% of AUM as GL. RBI understood, how broken MFI industry is, it’s a tailwind for Manappuram and Muthoot both..Just go through Q2 concall

Whatever I read, this deal will face delay because of Bain’s other investments. Deal is not cancelled.

Reuter has published the report citing unnamed sources, according to which the Reserve Bank of India has raised concerns to Bain Capital’s proposed acquisition of a majority stake in Manappuram Finance Ltd, as Bain Capital already has a controlling stake of more than 90 percent in another NBFC, Tyger Capital. RBI is uncomfortable with a single entity controlling multiple lending companies.

According to Reuters, to address this RBI’s concern, Bain Capital is considering diluting or exiting its controlling stake in Tyger Capital so that Manappuram transaction can proceed smoothly.

It is important to note that, till now, there has been no official communication or press release from the RBI on this matter. The report is entirely based on anonymous sources who declined to be identified. Reuters also notes that the RBI, Bain Capital, Manappuram Finance, and Tyger Capital either declined to comment or did not respond to queries.

At the same time, it is equally important to highlight that the transaction has already progressed meaningfully on the regulatory front. In recent months, the RBI has approved the appointment of Bain Capital’s nominee directors on the board of Manappuram Finance (https://www.bseindia.com/xml-data/corpfiling/AttachHis/fe6fb9f0-0280-486a-bf12-87bdddd84550.pdf)) as well as on the boards of its key subsidiaries, Manappuram Home Finance Ltd and Asirvad Micro Finance Ltd https://www.bseindia.com/xml-data/corpfiling/AttachHis/6a7eb742-2ad9-491a-a055-540b8d96fdfb. In addition, the transaction has already received approvals from the Securities and Exchange Board of India (SEBI) and the Competition Commission of India (CCI).

Lot of up & down will happen in this.. It has a rich history of doing all these :)

Wondering few days back, there was a planted news (citing resources) that Bain Capital may increase open offer price → which resulted the CMP to cross Rs. 300 first time.

Now, a news has been planted (citing resources again) that RBI is not so okay with deal considering Bain’s major holding in another NBFC.

Personally, I look forward to much more such planted news till the time RBI finally announced the go ahead.

Disc: Invested (till Bain appointed team is running the show).

After all, there seems to be some issue and thats delaying rbi approval ! I guess everyone is puzzled equally.