The promoters never diluted equity -

Mar 2007 Mar 2008 Mar 2009 Mar 2010 Mar 2011 Mar 2012 Mar 2013 Mar 2014 Mar 2015 Mar 2016 Mar 2017 Mar 2018

Share Capital 13 16 14 14 13 13 13 13 13 13 13 13

| CMP |

38 |

| P/E |

2.5 |

| P/B |

0.3 |

| P/E*P/B |

0.6 |

| Div Yield |

7.9% |

| Market Cap |

249 |

Cash+Investments 491 = 2x Mcap 249.

FCF/CFO 89%

Trading terribly cheap PE = 2.5 earnings, P/B = 0.3, and Cash is almost 2x of Mcap.

Now company is almost debt free ( massive deleveraging happened) -

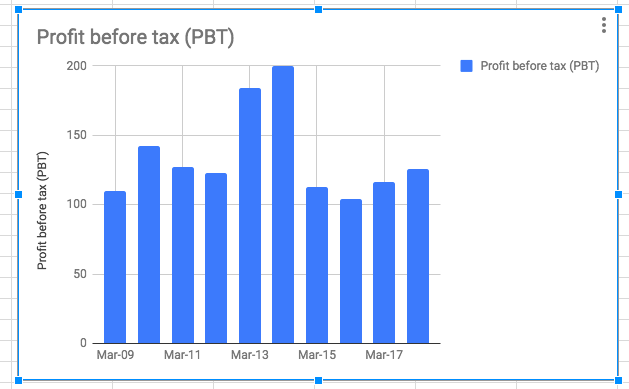

Has always been making > Rs 100 Cr yoy and Mcap Rs 249 Cr.

Company looks terribly cheap but it has always traded cheap -

- Historical PE 10Years: 3.27

- Historical PE 5Years: 3.03

- Historical PE 3Years: 3.56

I am confused why its trading this cheap and always been trading this cheap.

Would love to know views of folks here. To me looks like company is not fraud - Has made CASH , which can be seen in balance sheet. Promoters have shared profits with minority shareholders in terms of dividend.

Total Div 10 Yrs 107

but i am not able to understand what markets hate about this company ? Was it the debt which was too high years ago , which has now come back. should we see the rerating on the cards ?

Disc - Not invested.

2 Likes

I think they sell metal caps for beverages and whiskey bottles

They don’t have any bargaining power

If they start charging more than cost plus a small markup, companies that buy from them will buy a plant for these caps and cancel contracts

Secondly they have to cetynclosely manage their costs which is aluminium, unless you have smart people constantly hedging that, profits can vanish very quickly

So it’s a commodity that requires more than average person to run

It’s like giving a person with an IQ of 230 a cycle to race with someone on a motorbike, even if the motorbike rider has an IQ of a 10 year old, he will still win

1 Like

I think you are talking about BKM Industries limited, formerly Manaksia Industries Limited.

Manaksia Limited is a Marine Engineering company.

http://www.manaksia.com/marine_div.php

Manaksia Limited is one of the newest ventures of Manaksia, a Calcutta based Engineering company listed company. We are presently working on the designs of

- ADS, Air Defence Ship (Aircraft Carrier), being built at Cochin Shipyard.

- Water Jet propelled Fast Attack Craft for GardenReach Shipbuilders and Engineers.

- 12 Ton Bollard Pull Tug for Mauritus Port Trust.

- 80m Multipurpose barge .We have built a number of hull blocks for GardenReach to the exacting standards of Indian Navy, repaired a number of sea-going and river vessels and are presently building the abovementioned 80 m barge.

Our design team, comprising of sixty engineers and draftsmen, is an excellent team, proficient in state of the art softwares like TRIBON .Each is an expert CAD technician.

had a cursory look into thier latest AR.

their buisness consists of food packaging - not just bottle caps.

food packaging industry is set to grow at 5% cagr upto 2020.

India traditionally is against consumption packaged foods and i see a big obstacle here.

Unlisted players probably give a fierce competition to pricing.

They have subsidiary companies in Ghana and nigeria to whom they have loaned out some money. need to check what is being done of this loans.

while such companies may not have pricing power, comfort can be drawn if long term contracts are in place, isnt it ?

@AmitContrarian , doesnt a low P/E multiple also mean that the market doesnt expect the company to grow faster ?

a P/E multiple is also a rough indication of the expected growth, right ?

so in absence of any growth triggers, may be the company will continue to trade at low p/e ?

1 Like

The question is not just about low P/E but how much low. Even 5 P/E is low for a company that has RoE of 12% like Manaksia. Then in that case, this stock can double from here even for zero growth if reasonable dividend is available.

2 Likes

Manaksia is earning most of the profit from their subsidiary in Nigeria & Indian division doesn’t contribute much to the top-line & bottom-line.

I feel there are various reason for the undervaluation.

But most important risk is Co’s main business is in Nigerian subsidiary which is difficult to scuttlebutt,Currency volatility risk & geopolitical risk.

Since Nigerian economy is dependent on crude oil & on 20th june 2016 Nigerian currency devalued its currency by 30% in a single day due to recession because of tumbling oil prices.

Secondly, Promoter is not extrovert & open so very little information available about their future plans.

Thirdly,All the cash is in Nigerian government Bond where yield is near 14%.

Now talking about positives-

1.Balance sheet has improved a lot & company is almost debt free.

2.With crude oil prices going up, Nigerian economy is doing good & their currency Naira has appreciated almost 15-20% against rupee in past 1 year.

https://www.xe.com/currencyconverter/convert/?Amount=1&From=INR&To=NGN

3. As per meeting with management during AGM dividend for FY19 is expected within next 2-3 months.

4. Business activity improving slowly now in Nigeria.

My opinion may be biased as i am invested.

6 Likes

any plans of bringing the Cash back to India ? Did you check with them … Now i see why its trading cheap.

Any chance of revival of Indian division which doesn’t contribute much to the top-line & bottom-line ?

Now i see the risks and why markets not interested in this company. Key is cash if that is not coming back then it will remain cheap stock.

2 Likes