The emotions of people and the market never ceases to amaze me. The same people who were bullish for the long term just a few months ago are now packing their bags and leaving the market. The market does direct moods though… a few months ago while the market was rising you had people talking about how in the long term everything would be fine. Now that the market is falling everyone and their neighbour assumes this is the end of the current world order. Personally, I’m enjoying this. I’ve always bought companies only when i feel their valuations were good and hence why ive not experienced a huge Zomato esque crash.

I haven’t added more to my PF since I’m still about 6 months away from reaching my target Emergency fund value. However, my wife already has an emergency fund built so I’ve begun building positions for her again.

Added a huge amount of Lux industries yesterday at 2080. I have been patiently waiting for these levels for a while and I’m glad i got to pull the trigger.

Will be adding more into piramal too.

Also, watching Bajaj consumer intently. If the overall market crashed and it’s available at 110/120 i will finally pull the trigger

I’m also eyeing a new age tech basket for her with Zomato + infoedge etc but they are still nowhere near the valuations I’m comfortable with so I’m hoping for further draw down.

In short, if we don’t build our positions during bear markets when companies reach reasonable valuations… when do we? I’d rather build now over the next few quarters or years(depending on how long the bear market lasts) and stop building when we things are rosey and everyone predicts infinite growth.

When people start predicting market direction with certainty(almost everyone assumes we have a recession on our hands)… it’s time to go in the opposite direction… atleast if one has a long timeline and huge trust in their mentality and the companies they own.

At such mouth watering valuations, I have also been meaning to add Lux Industries but still not able to make peace with the corporate governance, especially the recent insider trading case. Even though, I feel that all these pessimism is built into the current valuations, but still it feels not so safe to bet on such management for long term.

I have been studying both Lux and Rupa, since both looks very attractive at such valuations. But IMO, business wise Lux fare much better than Rupa especailly the way they have scaled it up and changed the product mix towards premiumisation. Lux also has a better brand recall than Rupa. But just because of Coroporate governance overhang in Lux, I ended up buying Rupa couple of days back.

What’s your view on this?

I can overlook it since it’s not about money being diverted to subsidiaries. Case like these are rampant in the Indian markets and are forgotten in the long run. There’s a grey area here too regards disclosures and i find it provides opportunities more than anything else. Had a similar issue with intellect and i was comfortable with it. Lux as a whole won’t suffer due to it. It may take a couple years to resolve… but by then lux would have moved further into premiumisation and opened more ebos so as a whole the company will be a lot more valuable then. Will be adding every few quarters until the position is large enough. Right now I’m just done with tranche 1 and will add more if it breaks this support and falls further

@Malkd Thank q for the timely updates and valuable data points with strong conviction views on businesses.

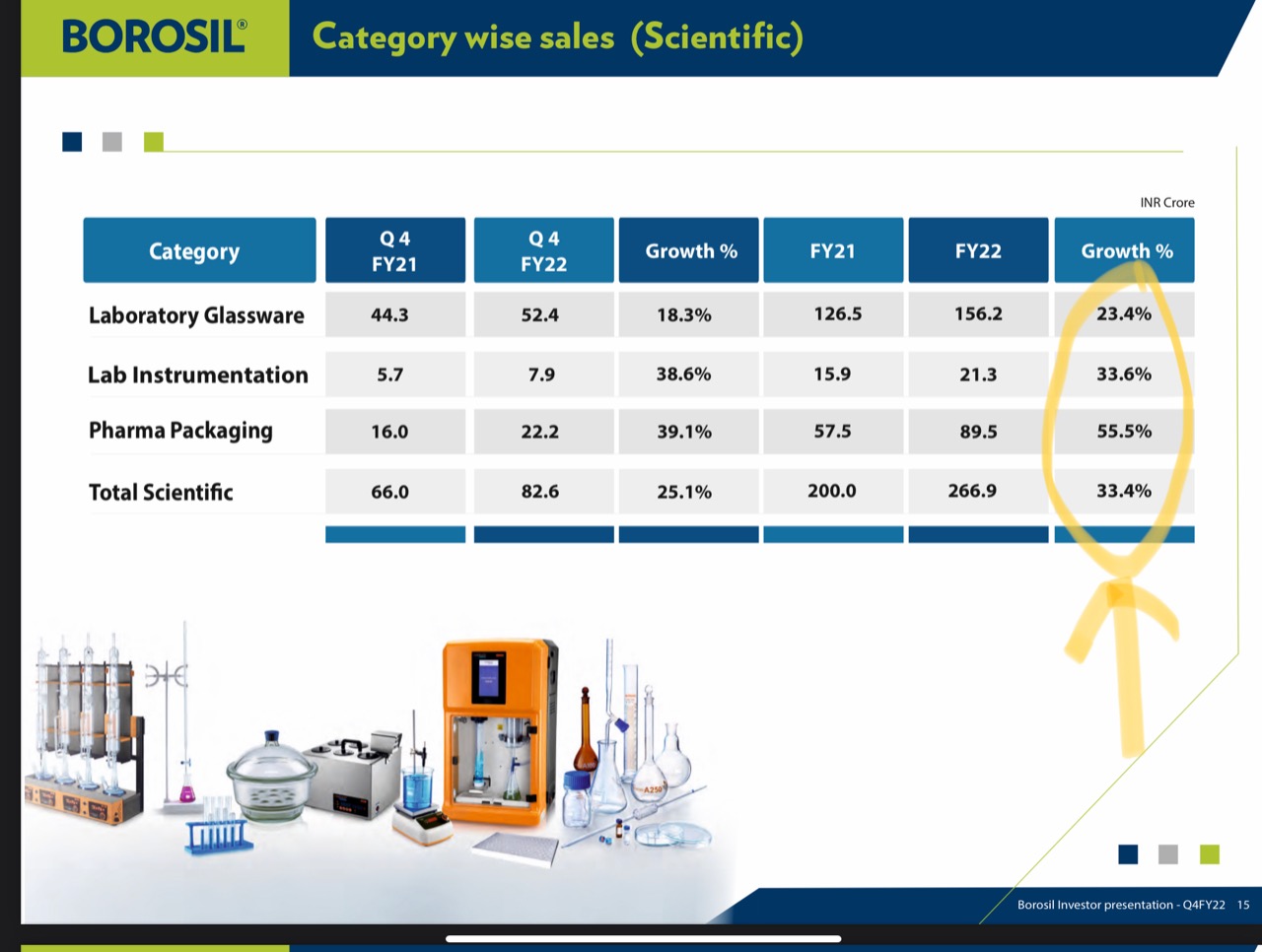

I read couple of your views on Bajaj Consumers, if u are looking for developing consumer story request to check/look into Borosil Consumers, solid story developing there.

Refer below some snaps from Investor Presentation and latest Concall added for quick review.

I’m a huge fan of the borosil group… especially renewables. I am staying away from high valuations at present though. Maybe on much further drawdown i would consider.

The reason i like the Bajaj consumer story is because

Pessimism has reached the point where the dividend yield alone should be near 6 percent even during trying times. Perfect place to park money long term vs my idfc first savings account once I’m sure we are near bottom since huge supports have been broken and the original ipo price is around 132 and I’m going to be greedy here and stubbornly wait for that price(ignored it at 140 too)

Nothing good is priced in. I like their new digital ad campaigns along with Mr nandi and the move to premiumisation plus new products and do believe that they are moving in the right direction but slowly. Their overall business is a good margin cash flow business so even if they don’t grow and give the shareholders the money i m happy. Expecting nothing here for 2+ years but thats the beauty of this company for capital protection…

The bet is to buy in at 6 percent yield and wait for the business to improve and see the dividend rise from rs. 8 to rs. 12 per share over the next few years and wait it out while the new products get built(similar to the bet with ITC from 2020). If things go superbly then this could go even better. If things go bad i would probably be stuck with the 6 percent yield for a few years which is equal to the idfc savings account. Bonus is this is a 2000 crore FMCG company with no debt and huge amount of cash in the bank (700 crores) and free cash flow every year… ie safer than any bank. As long as no CG issues arise I’m quietly confident regards capital protection here. I also know i would enjoy seeing the progress over quarters via the presentations and concalls too.

There are obviously much, much better stories in the market right now and this is one of the worst companies to bet on… and hence why i like it lol. In the current market i only like these kind of low risk (for me) bets. Not eyeing the likes of borosil etc right now but will have a look in the future. Cheers.

This was expected the moment war broke out And hence the low valuations. Bought it with this in mind… I won’t be adding further but i will be holding on to the stake I’ve added already to see how it plays out. It’s a small risky position that will prove insignificant if it fails and could have a huge upside if it works out. Buying companies like these at huge valuations when there’s hope in multitude is the problem. Buying them at current valuations offers a margin of safety. I’m not a huge fan of the company though… can see a lot of pain here with recent admin changes, debt servicing, delay of demerger, generics derating etc and if anything it’s the perfect storm of things going wrong for me to sharpen my knife regards pharma and give me a huge amount of knowledge that i can apply elsewhere ie laurus which is my main pharma bet

Small update:

When setting up my Wife’s safety portfolio i set it up such that ITC was the biggest contributor. The whole of India knows ITCs results so i won’t comment on it anymore… However, it’s been a roaring success. Yesterday’s results were good too and imo it continues to be the perfect hedge in this current market. That being said… i stopped adding at rs. 200 and will not be adding any more to it until the dividend yield comes back to the 6 percent which i don’t foresee happening again for a long time or ever. The reits too have performed well in this bear market and are refusing to come back to levels I’m comfortable with to add more. So I’m currently on the lookout for a new company to protect capital, give out dividends and have some upside too long term. Currently I’m just building cash for her and watching the following companies closely:

Bajaj consumer, PTC india, Manapurram finance and Amaraja Batteries.

They are nowhere near investable right now due to both technical and fundamental reasons and I’m just tracking them to see if i get an unreasonably low opportunity in any of these over the next few quarters if the market continues in this direction. For now I’ve open an idfc first bank savings account for her and I’m letting the excess cash collect in there at 6 percent interest…

if Bajaj consumer reaches a 6 percent yield (assuming a base of rs. 8 dividend) i will deploy there. Written a note about this above.

If PTC india comes down to rs. 60 then i will deploy there too(the PFS issue requires a bigger margin of safety than i initially thought).

If Amaraja Batteries goes down to it’s march 2020 lows then i will add there… i am still unsure about the battery and EV market so this is my least priority.

If manapurram continues to fall below book value il start adding at around rs. 80… it’s a fantastic company that’s going through a rough patch due to being overly conservative last 2 years while it’s competition went agressive… personally i prefer conservative management in financials over agressive and can’t believe that the dividend yield alone here is going above 3 percent right now so il be investing very soon… The nature of the market has made me greedy though and I’m looking at lower levels if possible.

If none of the above occur then il just leave her cash in the idfc savings account. The mirae fang etf would seem a good alternative too if it comes down to rs. 30 to 35 since she wants some tech exposure and I’m not comfortable with the Indian basket even after their huge falls (ie naukri, Zomato etc)

As far as my PF is concerned I’m still continuing to save up cash for the emergency fund. It’s going well and i should be able to be active in the markets again by December of this year.

Side note: Bear markets are a lot more interesting than bull markets for me considering i build at low valuations for the long term. I’m sure we ll see further crashes over the next few months… the same way we had bull market gurus in the bull run we ll have bear market technical chart predictors in this bear run (already seeing them pop up everywhere predicting complex factors that no one human can comprehend in one simple chart) etc… but that’s all part of the game. I will continue sticking to the principle of adding when valuations are in my favor during a bear market and letting run during a bull market.

@Malkd Since you are considering PTC as a Dividend stock, may I enquire why PFC or REC fails to match your criteria ? I also had PTC but sold it on doubling my money. But as I see it , REC & PFC has even better dividend yield without the PFS complication as well .

Also, at what price would you consider polyplex a buy(I am assuming that you are aware of it and it does not meet your criteria for some reason) ? Even at current price it has 6.5% dividend yield besides good financial metrics(It looks that way to me atleast ) .

Your latest posts after Q4 results on Laurus, DN & IDA were great to say the least as it really tells one how to think about long term investments .

Hey @Ghonarbochon

One of the main things i consider when investing for a dividend yield is downside protection. Polyplex deals in a commodity and is cyclical… Atleast it was when I looked at it back in 2020 when it was sub rs 500 and it showed up on screener with an insane 16 percent dividend yield. In hindsight that was obviously the best time to invest and i missed it. Right now at current valuations I’m not comfortable investing since i don’t want to chase a 7 percent yield at the top of a cycle and potentially lose half my capital.

Apart from capital protection i also like the possibility of some sort of upside in the long run . I just don’t see that with rec and pfc. That being said i haven’t really studied them well enough to be certain about dismissing them. The perfect combo of Capital protection, yield + long term upside was ITC at sub rs. 200 and reits at 30+ percent discount to nav. I’m trying to replicate those right now which is a bit tricky but i get a sense of similar possibilities with the options I’m currently looking at ie capital protection + yield + long term upside ( offs, rites, ptc, Bajaj consumer etc)

Thanks for the quick reply !

I asked you about polyplex to get a counter view about Polyplex and thanks for providing it. I bought it at around 1200 as to me it looked like a company that has achieved scale in a competitive industry. Also while the industry PE indicates the commodity valuation, the company profits for past 6 years or so looked stable and rising. Plus if dividends could make Rockefeller happy, it surely can make me happy . .I am also not adding anymore except to buy more of the same out of the dividends .

I had bought PTC as well @49 Rs. looking at the demerger possibilities and the Pranurjaa hype but sold out at 110 , because it seemed to me that they are so slow that the demerger could become a posthumous affair for me . But at 60 it would be definitely worth it again.

Same here. I’m targetting 60s for PTC. It may never reach there but I’m hoping the PFS issues forces it to. If it doesn’t then il just look elsewhere. I personally love dividends when I’m investing in a company that will struggle in the short to medium term… reason being i get some sort of short term gratification while waiting out headwinds to disappear. Same reason I’m currently targetting Bajaj consumer and Manapurram. If they fall to unreasonable lows of 120 and 70 each i will be taking the plunge and enjoying the 5+ percent yields (blended together) in the short term at the current business bottomswhile waiting for green shoots to appear and for things to improve in the long term since these kind of bets take a while to come to fruition. the trick is figuring out if profits have stabilized at a bottom and hence one can extrapolate atleast current profits in the near term to maintain yield and also if one is getting a huge margin of safety at an unreasonably low valuation so that capital protection is also ensured. Hopefully out of 3 to 4 companies that i track atleast one will offer the above at some point in the future for me to invest since im asking for what looks like unachievablely low entry points in all of them due to the opportunity costs involved in these kind of bets. All 4 of Manapurram, Bajaj consumer , Amaraja and PTC have crashed quite a bit but are each still about a 15 to 20 percent fall away from my entry. Here’s hoping the Bear market continues for a bit so that atleast 1 of them gets there haha.

Nearly a year ago i began one of my biggest deep dives into a company yet where in i literally tracked their branches and made friends with the CS and a leap of faith trusting and researching a questionable promoter plus checking their placements at various colleges to see where they were hiring. A small risky nbfc called ugro capital:

The profits at the time were a lowly 1.5 crores in a quarter and the price was around rs. 100 and i created one of my biggest financial positions in my PF. They just announced their results and profit for the quarter has jumped to rs. 6 crores ie 4 times in a year and about 2x qoq! There is definitely something big brewing here. Will edit and add more info to this comment post their concall. Here are the results for now:

@Malkd Why not look at irfc? Dividend yield is great. Trading below book value + No npa so no provisioning + company can potentially benefit from rising interest rates

I think it’ll match your dividend with capital appreciation framework

Thanks @ravigala … IRFC is intriguing but I’ve already got a stake in RITES and I’m not too happy going with 2 companies in railways. Also, i don’t see a huge upside with IRFC.

Currently my main target if i were to go the financial company route for capital protection and upside and dividend is Manapurram finance over the likes of irfc. I understand why it’s been battered down and considered a value trap(losing market share, rbi capping growth, gold loan cycle etc) but i also know that the management is proven and have an eye on sustainability and the long term and can be trusted to turn this ship around in the long run. Just purely based on dividends it’d be a good bet at current prices… on average they’ve paid out 28 percent of their profits as dividend since 2014. With just 14 percent of payout last year the dividend is rs. 3 ie around 3.4 percent yield at current prices since it’s trading at under book value. If growth stalls i can see this payout increasing… if growth comes back i can see 10 to 14 percent payout being the base but on higher profits so the 3 percent yield looks good as a minimum going forward(maybe an exception if profit falls over FY23). At current prices and considering how well capitalised they are and the brand they’ve built I’d also say there is a huge downside protection since i can’t see the book value falling too much and hence i can’t see the price dropping much further either.

So this is my number 1 bet in financials which hit my criteria of slow growth but with stability (with possible upside in the future) + capital protection(at under book value) + dividend (with a base of 2.5 to rs. 3). Such opportunities are pretty rare and for someone who has a 5+ year timeline they are perfect. I am being greedy and waiting for low 80s/70s though to increase the possibility of my returns if the risks of losing market share etc do play out.

Note that my family has been invested in Manapurram since 2016 ie sub rs. 30… so for some people who have invested recently it’s a wealth destroyer. But through my eyes it’s a huge wealth creator which in just 6 years gives my parents a 10 percent yield on original investment even without capital appreciation(though it’s been a 3x since then too and was a 7 bagger a year ago) even now when the company is struggling and hence why i may be biased.

@Malkd Apologies for bothering you again …

Would you consider adding Vaibhav Global at this price or do you foresee further slide ? I have been eyeing it for a while and I am aware that results are unlikely to get back to eye catching levels for 4-6 quarters ,but I am not sure what would be a safe price to pick it up without causing too much heartburn in short term .I am still very much prone to FoMO and not much good in calculating margin of safety ,so It would be very helpful to hear from someone who already has a stake in it .

@Ghonarbochon

If i did not already have a sizeable stake in it i would have definitely started adding now. PE 20 for a business model that churns cash so easily is a great buy. I’m just annoyed i overlooked valuations here and built my position at nearly double the current valuations… something I’ve never done before and will never do again

@Malkd any thoughts about KPIT? I’m still holding it from 130 level…At what level u find it attractive again if it comes? I will add more at around 350 of it comes

It’ always great to listen to you sir. You keep on inspiring newbie like us. With your inspiration I started studying gold finance business today. I will share my learning with my wife also so that knowledge keeps on passing. I am very grateful to be the part of this forum which have wonderful person with whom we can learn much. Keep writting @Malkd sir…As far as gold finance i think Rupeek has very disruptive businees model of giving home loan within 30 mins at your home. The whole business is based on asset light model. Does any body have any experience of doing any sort of business with Rupeek? They are claiming that they have 5 lacs + customer in one their ads. Ab se, Sone Pe Loan Right From Home. - YouTube

@PraveenKG

I’ve realised in time that I’m not so comfortable with IT companies… especially the smaller ones… i think i have to accept that they fall outside my circle of competence. I just don’t understand how to valuate them(apart from IDA due to its link to the banking and financial industry). I honestly have no idea what levels to look at regards KPIT. I found it risky at rs. 60 and just 2 years have passed so my mind can’t wrap around the current price … in the future il just be following a basket like approach with IT with mid/large cap companies. When companies like HCL tech or LTI etc crash or have temporary issues il just add them instead of trying to understand the small caps. I’ve realised I’m not built for small cap IT after i sold kpit, expleo and saksoft early only to see them defy gravity price wise.

@thakurvi

Gold loan companies are facing a lot of competition and headwinds. Add rbi regulations and Imo the period of fast growth is now behind them but that does not mean they’ll stop growing whatsoever … which is what the valuations in Manapurram are saying. Il be happy even if it grows at 10 to 12 percent per year over the next 10 years at current valuations + spin-off of MFI since those alone could lead to huge upsides from under its current valuation(not quite current valuations… I’m still waiting for the golden number 75 to take the plunge). I don’t think the gold loan sector will lead to any multi baggers etc. By FY28 I’m just targetting a book value of 160 ie 10 percent cagr over 5 years + mfi spinoff + dividend payout increasing to rs. 7 or so per year after 5 years(increase from current 14 to 20+ percent) with downside protection due to good management of npas so i can bet big. If there is some re rating and it’s valued at 2x book value over that period then it’s a huge bonus… these low valuations allow for huge upsides. At even slightly higher valuations i wouldnt even consider investing.