@Malkd where can i find the concall transcripts for expleo ? i tried in tikr.com, trendlyne.com but could not find. can you please help

Hey @suryaprakashv73

You need to attend them live and then a few weeks later they put up the transcript on their website:

https://expleogroup.com/expleo-solutions/media-center/

Unfortunately there aren’t audio recordings anywhere so it’s a bit painful

1 Like

It is available in researchbytes(dot)com

Are these violations anything serious?

Today i was planning to buy Alembic and Ce across this.

Thank you @nagesh_reddy

Fantastic resource

@Aniesh7

They’ve already got anda approval for Treprostinil Injection which is an injectable which is to be made from the same factory that got the observations. So it’s nothing to be worried about. Expect them to sort it out within the two week period given by the usfda. Considering its their first injectable facility a few issues were to be expected… luckily they are minor and not data related.

Btw, To know how serious fda issues are with pharma just check the stock performance on the important days… on the day of approval of the injectable market cheered and took the price upto 980+… since then it’s just cooled off and made a new supoort. If there was an issue there wouldn’t be any mercy and it would’ve been in lower circuit before you could say good morning(that’s the danger with pharma and why quality beats all).

When the news detailing the problems came out market barely made a whimper with maybe a few panicked retailers selling out.

One note is that If a company like alembic with their fantastic track record has these issues pointed out by the usfda I can only imagine what observations they’ll have for the smaller companies with not so great track records. Shilpa is getting absolutely destroyed by the usfda for eg.

The stricter the usfda the better for companies like alembic to gain market share, target product shortages etc from their competitors and the companies that survive a round of usfda issues will get re rated soon after.

Edit: While today’s fall by 5 percent could insinuate some insider news regards approval not going through I’m banking on the following

- It’s not 15 working days yet since the usfda visit so nothing has changed regards the approval where the company specifically mentioned it was purely “procedural” in nature and thay they’ve already got an approval for a drug from the same factory. I trust the management to tell us if it was serious. If it turns out to be serious it will be serious red flag against the promoters and I’d sell at a loss if needed.

- Overall market fell and with the panic around Alembic it was an easy target for shorters.

- The factory is for an additional growth driver… So if there is indeed something wrong current revenue won’t be impacted. If they get approval then their muted Eps targets go flying out the window and the upside will be huge

- Technically the stock is now touched RSI oversold levels and the general panic around usfda made this reversion easier and quicker than usual

6 Likes

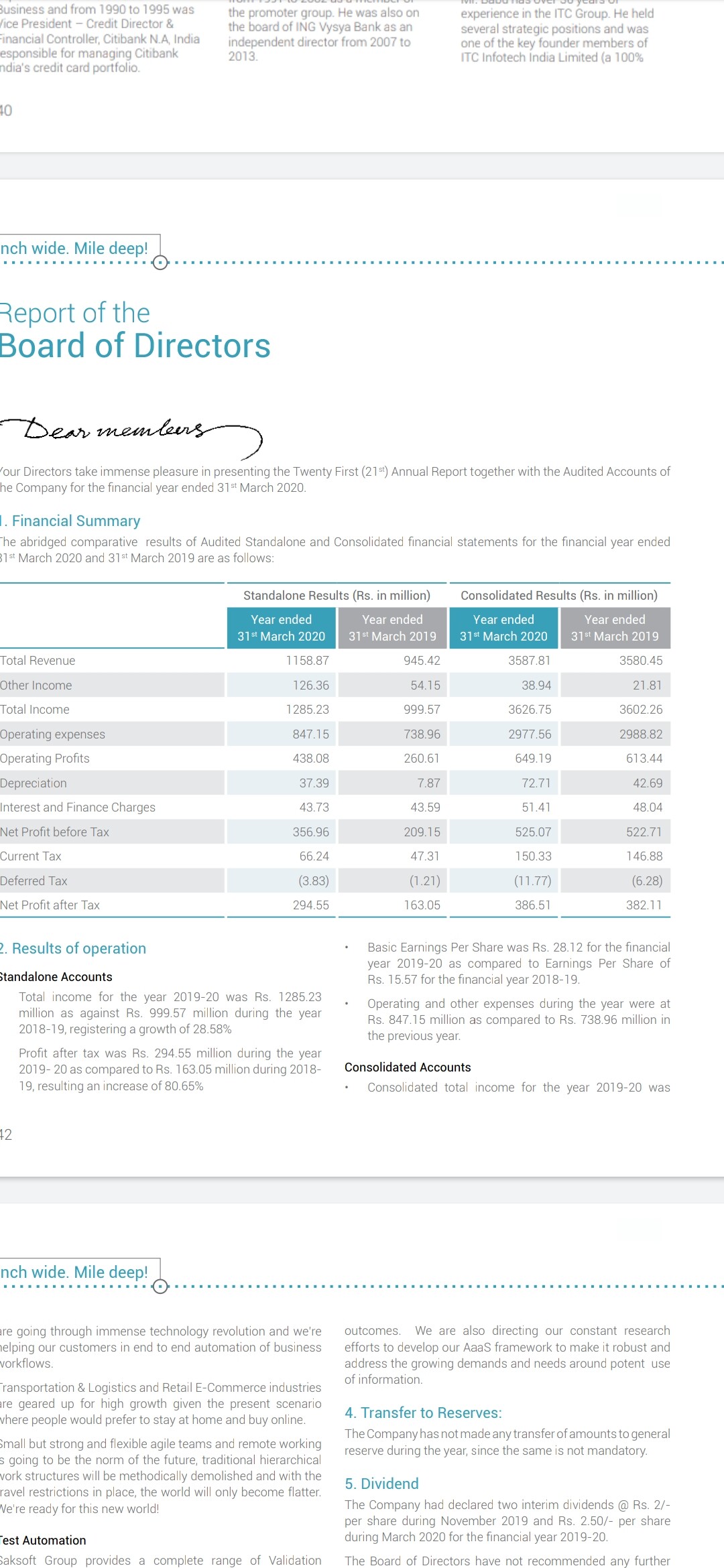

Saksoft Ltd - A digital transformation solution provider:

Currently trading at single digit valuations with about 68 crores in hand(though debt of 26 crores) Saksoft is growing via their own cash and is also giving out dividend from the same to shareholders. Return ratios are good and balance sheet overall is very healthy. All of this apart from the low valuations come part and parcel with IT though… so what makes them interesting?

They have spend the last few years completing a “string of pearls” is what they call it. They’ve been acquiring companies in specific verticals

- Electronic Data professionals in 2013

- 360 logica testing in 2014

- Dream orbit for logistics in 2016

- Faichi for Healthcare in 2018.

All of this helped move towards digitization in the following product mix to the following

a) Fintech

b) Telecomm

c) Healthcare

d) Transportation

e) Public sector

They have paid off almost all of the debt for the above acquisitions and all those are ready to contribute and have already begun contributing. From march 2015 to today EBITDA margins have moved from a low 10/11 percent to 17/18 percent. Revenue has moved from 230 or so crore to nearly 400 crores. PAT has gone up nearly 2.5 times since.

One of the main worries in IT is whether overpaying occurs during acquisitions (panaya cough ) but the way these have already begun paying back I don’t think there’s any worry of that sort here.

As per annual report majority of their revenue is repeat clients which is fantastic for an IT company.

They are continually hiring too which is a good sign. They’ve said attrition rate is low but I can’t find the exact figure.

Promoter holding is nearly 70 percent and there’s an increase in FII holding from 0.84 to 0.98.

They conduct Concalls twice a year and provide detailed presentations every quarter to plug in the gaps.

With their wholly owned subsidiaries and verticals ready to ride the digitization trend this looks like a very, very undervalued company.

The way I see it is if they came out for an IPO now they’d be churning up a market frenzy with their digitization theme and with Tailwinds in this sector

Obviously in a country like India where the big IT companies can squash the small ones at any time there are huge risks here but considering its currently quoting at under 1X sales and has broken through a multi year resistance and taken good support im thinking it could be well worth the risk taking a position here and building it as the story improves YoY (hence completing my relatively low valuation IT/Tech basket of IDA(Bfsi products) + Saksoft(Digitization Other Verticals) + Expleo (Testing)). Another heads I win tails I don’t lose much opportunity .

More than anything investing in this small company basket is teaching me a lot about IT/Tech from the ground up so a few years here with skin in the game will help me in the long run even if I lose my shirt in the process.

@rshankv … as usual your thoughts would be greatly appreciated

2 Likes

What a coincidence, I was comparing these three companies on trendlyne and going through their presentations

As I understand for SaksSoft nothing is working for them, Their acquisition has not put them on a growth trajectory as per my expectation, they are focused on repeat business means they are unable to acquire new customers which is problem when it comes to growth. so I rather bet on Expleo which is having a better growth or IDA which has having a good product in their arsenal, both of these companies valuation is higher than SaksSoft and there is a reason for that. IDA has shot through the roof in the last couple of months.

IDA has onboarded “Dave Revell” on its growth advisor board to expand its product sales which is a fantastic news

https://www.linkedin.com/in/dave-revell-icd-d-69b28914/

If I have to bet, then i will pick IDA and Expleo.

3 Likes

Thanks rshankv. IDA looks the best bet but valuations are the highest too. Expleo has good potential but is limited to the testing field for now but I do love their 3 year growth potential post recent concall. Saksoft i noticed this in their annual report

Their standalone business as specialist Bfsi is growing quickly. When it comes to their consolidated businesses they seem to have issues… however, those businesses were bought as recent as 2 years ago. Latest concall all they are talking about is their new verticals and about the new clients in those. Management doesn’t give growth predictions here but they sound very bullish overall talking about stake holder wealth etc . I think those new verticals have got enough Tailwinds now to start contributing meaningfully. At less than 1 times revenue it is tempting me still though this is more of a punt so if do get onboard it will be with less than 1 percent of my portfolio for now.

Btw I have to thank you again for helping in this sector. When considering no capex or debt worries (which are the usual worries in the sectors I invest in) and with free cash flows abound investing in this sector is a breath of fresh air and comes down to understanding the complex products/services and betting on management allocating well and innovating.I understand now why this sector has high valuations.

Creating an IT basket with IDA has my highest allocation, Expleo second and Saksoft a small third. Total will be 5 percent of my Portfolio. Will help me understand this sector better too and keep me ready for future opportunities when they appear.

2 Likes

If their approach to grow is through acquisition then their strategy is not the most efficient, They will acquire a company and in the next year the revenue and profit increases due to that acquisition and again if they have to grow, do they need to acquire another company? sorry if i am too skeptical here. These is very very small company with 1250 employees, and they have not shown any fire to expand their business other than through acquisition.

If you have their latest concal video link, please share it, want to hear them out.

1 Like

I have the transcript only. Here you go:

Just a few investors and questions so it’s short and sweet. Thanks for the pessimism. I’m getting too bullish in this space and need a reality check.

Based on what I’ve read they’ve completed their acquisitions now and did them urgently over past few years to get a legup in each vertical and will be concentrating on growing each one of their current verticals and have no plans of adding any more verticals.

2 Likes

Thanks Malcolm for the transcript, their onsite and offshore mix is close to 50:50 , I don’t know how they will leverage labor cost advantage that is usually found in India… I believe if we explore all the IT small caps , you will find the same story that this management is weaving, I will try to pull out all the IT small caps stocks and analyze on the mentioned parameters of 15% ,margin, growth and dividend yielding, Almost zero debt stocks.

The below is the list we need to comb through them ,keeping the current valuation in mind

https://www.moneycontrol.com/stocks/marketinfo/marketcap/bse/computers-software-medium-small.html

Saksoft is more of a BodyShop type of company . Its one of the main contract employee provider for the company im working for , from last 5 years . Dont think they have any significant product offering that would stand out .

3 Likes

Thanks @aerofire. I think their core business is body shop but since they bought these 4 companies

Electronic Data professionals in 2013

360 logica testing in 2014

Dream orbit for logistics in 2016

Faichi for Healthcare in 2018

Those are adding some more value. Il try to dig up details on all 4 of those companies. That’s being this seems like a lot of work to do for a random company like Saksoft but I’m enjoying learning lol. I may just give up half way and build Further in IDA Monday

2 Likes

I don’t understand IT sector much but as a long term investor can’t ignore it. So as safe bet I hold Infosys.

But as IT sectoral Tailwind is happening, I like to take more exposure especially midcap .

I was analysing IT firms which are purely into product businesses .

Like Intellect Technologies Ramco Systems Nucleus Software etc .

Is it like these sectors May show small spurts of growth once in a while if they win a few good contracts? N after that will it be subdued growth ?

Will they be able to sustain growth when IT sector take a downturn?

Are these IT product business cyclical in nature?

It will be very helpful if some1 can answer. As being from law field I have lot of limitations.

I can take a dig at the question.

Yes if a company bags a big contract, yes their revenue/profit goes up, the question to ask are

-

What is the the value of the contracts?

-

The type of work that they are taking up(Dev, Testing, consulting, analysis, support etc) , support and infra related contracts are not high in value, but anything related to data analytics ,business intelligence and development are high end work

-

The duration of the contract

*The contract type (fixed bid, time and material) , fixed bid are high risk and high reward , or is it just body shopping (like collebra, L&T ,IKYA,cybage,NLB, careernet)

*The model of work, in terms of offshore, near shore, onsite based or mixed, Offshore modeling has high margin

Usually US based companies will not award new contracts during their Q4 ,as the budgets are frozen ,so it cant be really termed as pure cyclical

3 Likes

Thanks for such details explanations and valuable insight

Appreciate it

1 Like

Now a days, most of the business are moving toward cloud from their inhouse platform. I have seen Microsoft Azure picking up and taking market share from AWS. So one can try to find companies like Mindtree who are working with Microsoft(30% of their business comes from MSFT I guess). Also Mindtree has bought a company in US(Magnet360 who is SalesForce partner). SalesForce is also picking up and gaining market share. Apart from Azure, any company working on IOT,Machine Learning, AI etc will gain market share. Now a days all big companies are setting up their vertical in these areas.

Another niche area could be LTTS which provides pure engineering services(medical/industrial/telecom/autonomous vehicle etc). I believe this is the future and could be a long term investment.

I have invested in both of them even though small quantity and very bullish on LTTS for long term considering the number of patents it has(around 400) and own 5G lab in India. I am sharing my thoughts since there is some discussion on IT companies in this thread.

5 Likes

Hi Want to know your views on following.

What is better business among LTI and Mindtree (As both are L&T business now) as of now and is there any possibility of merger in near future? However management has clearly said there is no merger and both will work independently. Mindtree is still trading at some discounts wrt LTI.

HappiestMind is also in same nature of business but size is small and do most of their business in digital category only.

Is LTTS under some investment phase and when the growth can be seen?

Disc: Invested in LTTS and LTI.

After having spent half my weekend looking at saksoft I’ve decided i may be biting more than I can chew. It’s been a fun experience and it’s made me fall in love with this sector though so I can’t complain. Management seems honest but there are too many unknowns here and with the other options in the market this really isn’t worth pursuing. Will be adding a grand total of 1 share tmrw just to track it for a few years and see if anything happens here ![]() … and keeping my cash ready to deploy even more in intellect and expleo as my IT/Tech bets as their story develops.

… and keeping my cash ready to deploy even more in intellect and expleo as my IT/Tech bets as their story develops.

Anyway, attaching expleo’s concall transcript below since it was requested above. One of the most bullish Concalls I’ve attended in a while

Earnings-Call-Transcript-Q3-2020-21 (1).pdf (200.2 KB)

Main pointers:

- New project that requires 120 hirings and that has the potential to last beyond 2 years. Also, another similar project in the pipeline. Clearly shows that they are attracting big clients

- Aim from the promoter is to double size and scale in 2 years. What that means is doubling number of people to increase scale which should lead to 50-60%+ rise in revenue approx (though could be closer to being directly proportional to rise in scale)

- Full Answer to question about whether exploring beyond Bfsi and testing:

" beyond testing for sure because now that the customers are also in agile

mode, so you need to be have the capability of software development and testing together, it is

not going to be just testing. And beyond BFSI for sure because we actually have now two

customers who are non-BFSI customers as well and most of the non-BFSI engagement that we

are winning are the performance engineering, performance testing, security and vulnerability

piece and the other one which we are exploring is also the RPA element as well and now with

the new focus of combining the strength of the other entities within India, we will be looking at

outside of BFSI for even the normal testing as well." - Specialised testing and digital services now contributes 25 percent of the pie… up from 9 percent in 2019 (Vs Traditional testing and automation which is now just 75 percent from 91)

- In this calendar year revenue growth will be minimum 15 percent.

- Due to expected surge in growth EBITDA margins may fall but won’t go below 18 percent. This will purely be for the short term ie 4 to 5 quarters in FY22 onwards(though Q4 should be high margins). Will go back to above 22+ soon

In short: structural changes are happening starting with management change, product mix, new verticals and client acquisition… and there is something big brewing at expleo. Next 15 months should be a good test to see if promoters walk the talk. if they do then they’ll be set for a fantastic few years after especially considering the cash already available to them.

3 Likes

Now both alembic and Aurobindo is trading with P/E below 15 . And industry’s average is 39 .

Both are fantastic companies sales growth, profit , valuations all good …

May be Coz of US facing business , cut throat competition in generic druy, USFDA issues n low pricing power it remains undervalued.

Will it re- rate in near future or underperformance will continue?