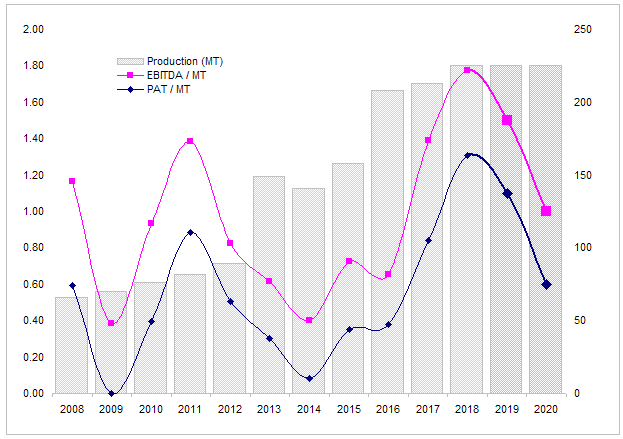

A sharp sell-off in Maithan alloys piqued my interest in the company to investigate what’s the reason for the sell off. Here is some data I collected from company presentations

FY

Production (MT)

Capacity

Utilization

EBITDA

PAT

EBITDA / MT

PAT / MT

Mar-08

66

81

81%

77

39

1.17

0.59

Mar-09

70

107

65%

27

0

0.38

0.00

Mar-10

76

107

71%

71

30

0.93

0.40

Mar-11

82

107

77%

114

73

1.39

0.89

Mar-12

89

167

53%

73

45

0.82

0.51

Mar-13

149

226

66%

91

45

0.61

0.30

Mar-14

141

226

62%

56

11

0.40

0.08

Mar-15

158

226

70%

115

55

0.73

0.35

Mar-16

208

226

92%

136

79

0.65

0.38

Mar-17

213

226

94%

296

180

1.39

0.84

Mar-18

225

226

100%

399

294

1.77

1.31

Mar-19**

225

226

100%

338

248

1.50

1.10

Mar-20**

225

226

100%

225

135

1.00

0.60

Rs Cr.

Source: Company IR presentations

** Estimates

Source: Company IR presentations

Note: FY 19 and FY20 numbers are estimates

Company is operating at full capacity and new greenfield expansion is not coming online for another 2 years. Which means production could remain flat at best.

EBITDA/MT and PAT/MT is at a 10 year high and can likely to come down to more reasonable level of Rs 1 Cr/MT and Rs 0.6 Cr/MT which are 10 year averages respectively. Assuming EBITDA/MT and PAT/MT drop to 10 year average in FY 2020, EBITDA works out to be 225 Cr and PAT works out to be 135 CR which is about 60% below current levels.

Current market cap is 1000 Cr so company is selling at 7.5 times FY20 PAT of 135 Cr. Looks reasonably priced. However, considering net cash position of 575 Cr as of Sept 2018, this company is actually selling at only about 425 Cr which is only 3 times FY 20 earnings. That’s what makes the valuations attractive but an expected fall in PAT will probably keep the buyers from jumping in. Margins can also take 2 or even 3 years to revert to mean which can stretch the timeline profitability will be impacted. That’s another factor that will keep the buyers away for a while.

One silver lining is that since company is operating at full capacity, EBITDA/MT may not fall to 10 year average. During 2009 and 2014 where margins fell to a very low levels company was operating at low capacity utilization and had recently expanded capacity. If that turns out to be the case, stock should provide decent returns.

Could you share your thoughts on corporate governance and how willing promoters are to share profits with minority shareholders. These seem to be important especially in current environment.

I realise such a judgement is subjective but any pointers would be useful.

Thanks

Hi @Yogesh_s - Average P/E for last 3 years or 10 years has been in the range of 4-6. Capacity constraint is a recent challenge. Any others reasons that you can think for such a low confidence by market in this business ? I am not sure if lack of utilisation leading to erosion in OPM% warranted such a low P/E.

@sarthakkumar19_

Corporate governance is a tricky subject. No company or promoter is black or white, everyone is some shade of grey. That shade changes from investor to investor and depends on stock price. Generally when price goes down, investors blame it on corporate governance as it is a catch-all excuse for justifying a fall in price.

Few tangible pointers I look at

Debt is nil. That’s a positive. In fact company has paid down debt over the years.

Executive compensation - That’s high. However some of it is justified by good performance. OTOH, promoters taking money out through front door reduces chances that they will take it out of back door.

Taxes are being paid. That’s a positive.

Cashflow is strong. That’s a positive. In line with cash profits.

Management communication. I have seen last 10 years annual reports and company has provided enough information about the company without hiding key facts. They generally put a positive spin on everything but that’s their job so won’t call it a negative.

Walking the talk - My impression is that management is generally good at this parameter.

Cash hoarding - They are sitting on huge cash pile generated over last 3-4 years but I won’t call it a hoarding. They had to borrow heavily during 2012-2014 so they are being defensive here. Plus this is a cyclical industry so having a large pile of cash provides a safety net. And they have planned capex and they are looking at NCLT cases for inorganic growth as well. So overall not negative but this is where walking the talk will be the key.

Dividend is low. That’s negative. But it has gone up in last 3-4 years in line with earnings. To me dividend growth is more important that level of dividend. They have also delivered growth which is double the industry growth so they clearly have growth opportunities so I would rather have the management not distribute too much dividend but invest it back in the business.

Profitability is high. Even at the bottom of the cycle company is profitable while others reported huge losses. At top of the cycle company is reporting 40% ROE which is great. Over a cycle average ROE is 28% which is excellent.

Working capital is low and company is getting credit from suppliers. That’s a positive.

since smelting is a commodity business, such companies generally sell at book value even if the company is generating a high return on that book value. Market is valuing the company as a multiple of book value and not as a multiple of earning.

Another factor is that downcycle in this industry can last 2-3 years so investors prefer to stay away until there are signs of a turnaround. That can depress price.

company has been generating high ROE (E/B) which makes the E part of P/E high and results in low P/E since market is valuing the company on P/B basis.

Other companies in the industry are struggling so investors many be valuing the company based on the average multiple for the industry

This being a small commodity company m it likely that it will trade at a discount to larger companies.

As soon as earnings begin to rise, investor begin to anticipate the downcycle so price begins to drop. That’s depresses P/E as well.

SEBI has asked clarification from Maithan Alloys regarding this price rise. Lets wait for their reply.

Clarification Sought on Price Movement

Exchange Disseminated Time 28/02/2019 20:17:05

The Exchange has sought clarification from Maithan Alloys Ltd on February 28, 2019 with reference to significant movement in price, in order to ensure that investors have latest relevant information about the company and to inform the market so that the interest of the investors is safeguarded.

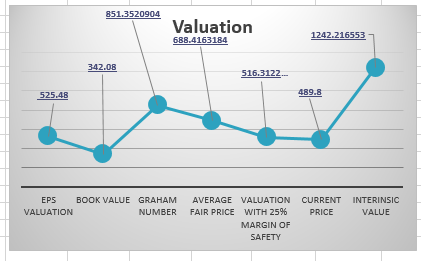

Reasonable valuation Request VP’s to check and found any mistake please point out Maithan Alloys VAluation.xlsx (110.0 KB)

But there are chances that it may slip further Let see How the story will roll out

Disc : Dose not held it yet This is not any recommendation , I am not any Sebi Approved Analyst Individual must Due their due diligence before investing It is on my Watch List

It is commodity converter and without having good view of the conversion margins and the underlying commodity, it is futile to look at valuation in isolation. It is a good company in the commodity sector but difficult to value IMO.

Q4 FY19 results: Revenue up (549.30 Cr vs 440.40 Cr) PAT down (70.10 Cr vs 88.98 Cr)

EPS down (24.08 vs 30.57)

Raw material cost up (272.27 Cr vs 206.29 Cr)

Purchase of traded goods up (52.36 Cr vs 14.29 Cr)

Maithan is the Highest bidder for Impex Metal & Ferro Alloys limited.

Regarding Impex Metal & Ferro Alloys Limited -

Impex Metal & Ferro Alloys Ltd.

Exported 85,300 mt of our total ferro alloyproduction in 2009-10. We intend to export 1,02,800 mt of ferro alloy in 2010-11 and the corresponding figures for 2011-12 are 1,35,300 mt. (from their website)

They were setting up a plant in Vizianagar with a capacity of 23,175 TPA for manufacturing of premium quality of Ferro Silicon and other Ferro Alloys

it is the sole marketing agent of Bhutan Ferro Alloy Ltd.’s

The company is highly dependent on the steel industry, which is cyclical in nature. Besides, the ongoing trade war between the US and China, a slowing global growth rate and ongoing political turmoil around Brexit in Europe have an adverse effect on the steel industry, leading to the company’s stock price dropping by around 50 per cent from its peak over the last one year. However, it has now recovered from that level. Besides, anti-dumping duty on steel products, a renewed push towards infrastructure and construction and robust domestic growth are some major tailwinds for the company. source : valueresearch

positive set of results with optimistic mgmt outlook.

revenue at 492 cr vs 481 cr yoy.

EBITDA margin - 15 % , good to see such strong margins in challenging times like this.

PBT at 69 cr , PAT - 52 cr.

“During the quarter, despite the domestic slowdown and a sluggish market environment, our Company was able to increase its Revenues by 7%. We were able to achieve the long term average EBITDA margins even in below-average market conditions. "

company expects steel prices to remain depressed for some time, but with 75,000 cr capex expected in the steel industry over the next 3 years, they expect increase in capactis by 16 million ton

With a complete basket of ferro alloys product, strong relationship with the customers and financial flexibility, we feel Maithan continues to be at a sweet spot and will be in a position to grow faster than the Industry.

Disc- Invested

I believe maithan alloy will take 2-3 years of patient holding before we see any positive. Though the fact that they are debt free and market leader should be comfortable and whenever the demand grows they should benefit more.

Have few questions from those who track this company closely:

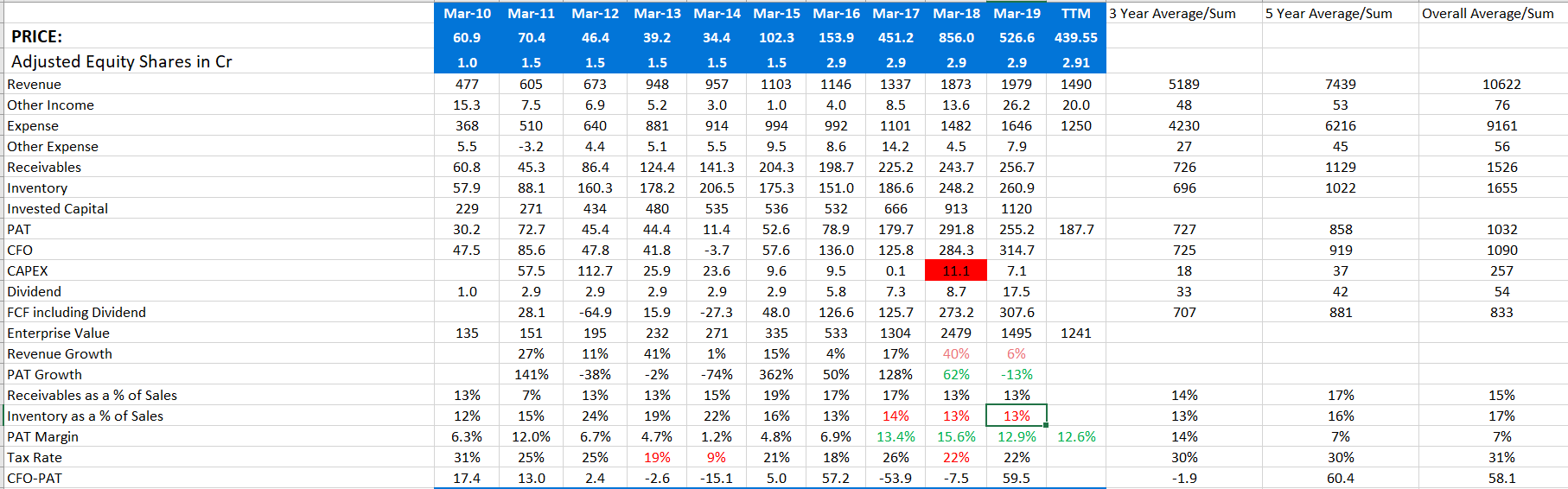

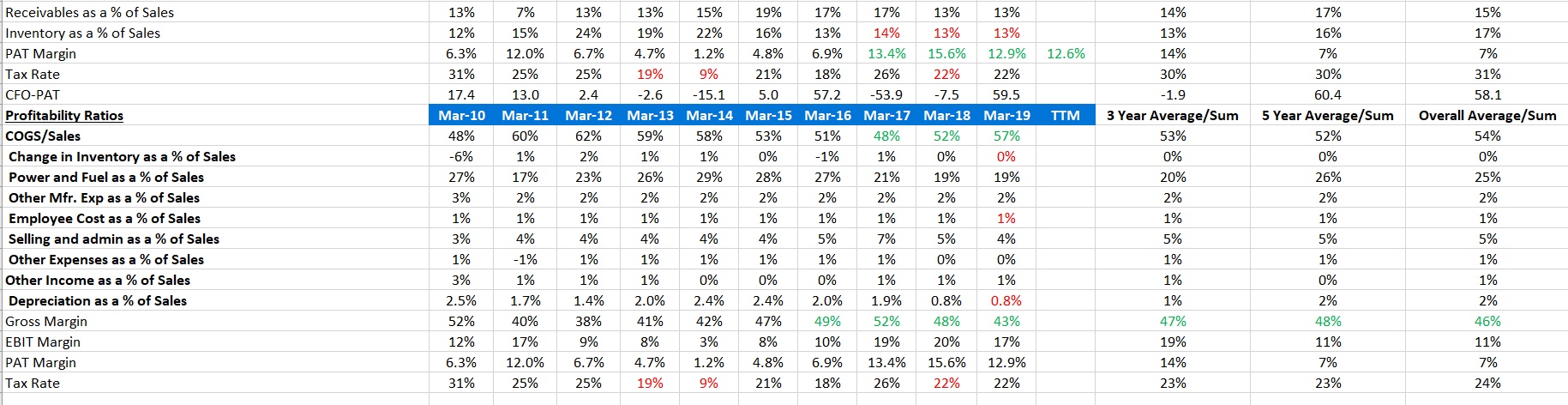

Company used to trade at low single digit PAT margin in early decade and the lowest PAT margin was in 2014 at 1.2% and current margin is 12.6% down from peak margin of 15.6%. If I try to see reason for such a margin swing, against my expectation of raw material cost, this comes due to swing in power and fuel cost which has come own from 29% to 19% of topline. The recent margin fall is attributed to 5% jump in raw material cost. What is the reason for such a drastic fall in power and fuel cost? Is it sustainable in long run, any views?

The raw material cost fluctuation range has been 48% to 62% of topline and from the bottom of 48% 2-3 years back , we are now at 57%. Is there something that history will not repeat or we can take this range as probabilistic raw material price fluctuation band, any insights?

Company went under major expansion between 2011-2013 and since then, there has not been any asset expansion and hence, depreciation looks too favorable to P&L. If I see depreciation as % of sales, its down from 2.5% to 0.8%. This should be ok considering it is 8 year old asset but the maintenance capex looks too low. In the process of going through old ARs but is there something to look in detail on depreciation, am I missing something or this quite normal?

Why tax rate is 22% n not 33%?

Fixed asset turns is at lifetime high of 8.6 against 10 year average of 4.8. I understand that capacity utilization may be at its peak. Frankly, surprised seeing such good numbers on asset turns, PAT to CFO conversion and CFO to FCF conversion. So, unlike a commodity business. Is there something special about the company that it is able to churn such good numbers?

Looks like company is churning lot of free cash flows and has not done any asset expansion in last 5 years, why then dividend payout is so low?

Sorry, in case any of questions are already answered as I am yet to go through whole thread and will check it.

They have 600 crores in cash on the books. They have kept this in cash because they plan to grow through acquisition. They are on the lookout for distressed assets which they can buy at a reasonable price.