Ranade explains: “there is a huge amount of expansion opportunities available in Mumbai, our authorised regions itself for example if we talk of mainland Mumbai, we are at around 25-30 percent penetration level so good scope is there over in Mumbai region. Even in the adjacent areas of Navi Mumbai, Thane district what we refer to, there is also similar type of penetration and maybe two years down the line there will new area of Raigad district which will be coming because there has been some announcement about new airport also coming, now formerly really launched and I think that will give us lot of opportunities for expansions”

natural gas prices have been marginally cut for Apr - Sep 17 period to USD 2.48 per mmBtu from USD 2.5 per mmBtu. Positive for Gas distribution companies

The flat volume is a cause for concern but MGL is slowly expanding its footprint on many fronts so i remain cautiously optimistic. I think the margin profile will remain intact at least for the next year due to the following reasons :-

Penetration levels are 25%-30% in mumbai & thane district. So there is decent scope ahead on that front.

The raigad district will come up in 3-4 yrs and ongoing developments in the navi mumbai international airport in raigad district will be a key trigger going forward. There seems to be some visibility on that front with development work already started.

Brent prices have gone up since the last 5 odd months after touching their historical lows and are expected to strengthen making natural gas more attractive. Once the exclusion of natural gas from GST and inclusion of fuel oil in GST issue is resolved there will be better clarity on this front.

They are actively scouting for M&A options & PNGRB bidding rounds. The 560 cr kitty that they have will allow them to move quickly. But there is currently no visibility on that front.

MGL has launched a CNG kit for two wheelers. Currently covers scooters, including the largest selling - Honda Activa. Reduces cost/ km to 60p. With petrol it comes to about 1.2-1.5 I believe. No information on cost of kit.

Leaks and all notwithstanding, mgl marches on. The companies con calls mention that poor infra and land avaliability are a big bottlenecks barring that demand far outstrips supply. They also mention that work is suspended in the monsoons and regular maintenance work cannot be carried out during this period. Poor infra and monsoons are probably the root cause of these leaks i guess.

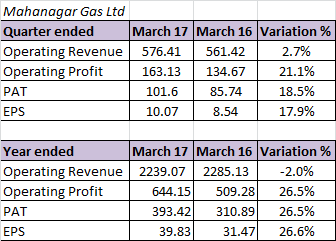

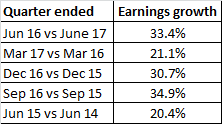

The most attractive part of MGL is consistent earnings growth.

In relation to its earnings growth I think that its reasonably valued and has limited downside. Of course, it will have some price shocks now and then in tune with the general ebb & flow of the market but one needs to give it some flexibility. Also the fact that it pays a decent dividend acts as further cushion

I believe the only risk that MGL faces is mass adoption of e-rickshaws in the MMR region. As of now, the state government has not indicated any inclination towards the same and the reason could be the powerful unions of Mumbai. But we never know - this can and might change courtesy our Supreme court.

Making CNG a part of GST is actually beneficial to the company. MGL has been raising this concern for some time now that excluding CNG was adding a tax burden to its consumers since they wouldnt be able to avail any tax credits making CNG less attractive for them.

Here is the proposal document by GAIL. Although this would likely increase the tariffs depending on the pipeline region, in the long run its a good news to the industry.

Meanwhile LPG cylinder price set to increase again for the fifth time since May, so roughly there is a hike every month. This no respite for LPG customers is good for PNG traction. Although not sure if there is a hike of LPG cylinders in Mumbai. Definitely IPG is set to scale.