The only way to achieve revenue growth above 8% is inorganic growth and they are looking for opportunities which is good.

Chairman’s message in annual report :

While there is ample scope for growing the business of MGL organically in its currently authorized

geographical areas, your company

is also continuously looking out for

inorganic growth opportunities.

MD’s message in annual report :

The proliferation of new license areas and

entry of new players will also provide

us with opportunities of growth through

organic and inorganic routes.

The comments are more intrsting then the article… though it talks a lot about the company. Can anyone confirm on this, if this is the situation faced by many.

I too got my house renovated. Their service is slow as the meter shifting is sub contracted to a third party. However it was not as bad as the ordeal faced by the author . There was a week delay but my expectations were low as it was a sarkari company.

Now, few of the questions we need to ask ourselves

Without the sops from the government, how competitive would the EV’s be when compared to CNG variant of the vehicle (I am meaning total cost of ownership - including maintenance cost etc).

How does it pan out with the sops announced by the government.

Cost of migration (how many of the existing customers are willing to migrate) - depends on the ‘sweetness’ of the offer based on above two points.

I have not yet seen any experienced based study at large scale on how the cost-benefit analysis pan out for the customers.

Personally, I feel EV’s would definitely capture a significant market share and would act as a “de-growth” factor. Closely watching out the commentary by the company in specific and/or the industry in general.

Disc: Invested. The post does not in any means an advice to buy/hold/sell.

Edelweiss has done some stress case studies on this and as per the several stress case scenarios carried by Edelweiss, they found that total cost of ownership for CNG vehicle is 36% lower. For example the cheapest CNG vehicle Maruti Alto is priced at approx Rs 4.5 lakh. It is almost 50% less than the cheapest EV Tata Tigor, priced at approx Rs 8.5 lakh. The comparison between Tigor’s EV and CNG variants found that CNG’s ownership cost is 11% lower even if CNG cost is hiked by 50% & E.V battery cost falls by 25%. In an extreme case where CNG gas input cost is up by 100% and EV battery cost is reduced by 40%, CNG’s Total cost of ownership would still be 6% lower. Further the issue with EVs is also the time it takes to charge a vehicle. Roughly, a 30KWh Tata Tigor EV will typically take 2.5 hours to charge. Similarly, the distance traveled on a full charge will be relatively limited to 142km for a Tata Tigor EV versus 234km for a full tank of CNG and 480km for a full tank of petrol. Another issues comes at availability of charging points for EVs which is currently very very less in compare to CNG Stations which is gaining popularity as the share of diesel cars has significantly reduced to 29% in FY20 from 48% in FY15.

Looking at the consumption of CNG in Mumbai, there are chiefly 4 major consumers:

BEST

Auto Rickshaw / Black-Yellow Taxis

Fleet and Aggregated Cabs (Ola / Uber / Meru)

Private Owners

The cost concerns of ownership primarily affect the Auto Rickshaw / Black-Yellow Taxis and Private Owners. The BEST has been steadily adding electric buses to its fleet. Similar considerations are underway with the Fleet Cabs, with Meru by Mahindra already being all electric (but a lower market share). The transition of auto-rickshaws and cabs is all but inevitable a few years down the line. Quite curious to see how it unfolds and what are the drivers for it - another environmental push cannot be ruled out. The SOP related to chargers in housing societies would help set up a decent infra for electric, but that may be restricted to private owners.

I agree with your assessment of EVs being a de-growth factor for MNGL. I anticipate a little faster de-growth since major CNG consumers like BEST are directly advantaged by policy changes.

Disc: Invested. The post does not in any means an advice to buy/hold/sell.

Could anyone please enlighten me as to any fundamental reason why MGL is trading at a steep discount relative to its Peers IGL or Gujarat Gas - while being superior in almost every quantitative measure (ROE, OPM, Yield, Debt Ratios etc). Growth is lower - understood.

I have just dipped my toes into this Business so I am still analysing it quantitatively.

Just want to understand whether this is really an inefficiency in Market Valuation or whether there is any way in which its Business is inferior to its Peers.

Look forward to hearing from anyone who has been following this for a while.

No high growth opportunities unlike other gas companies. Smaller scale of operations, and possibly a saturated market in areas except Raigad.

No investments/JVs in other GAs. Sole reliance on Mumbai. There is no way to expand apart from receiving licensed through auctions. Highly regulated sector.

I think that current price reflects the weight of below factors:

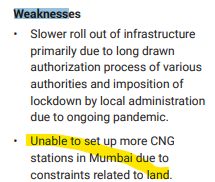

Lack of expected growth as business caters to limited geography [Majorly Mumbai, which lacks land to setup CNG stations]. From FY21 AR -

Even the past numbers reflect this fact.

CNG stations (No.):

FY11-12 → 150

FY20-21 → 271

Pipeline Steel (Kms):

FY08-09 → 250

FY20-21 → 522

Pipeline PE (Kms):

FY08-09 → 2500

FY20-21 → 5394

Post ongoing expansion/seeding phase[5~8 Yrs.] of city gas, I expect industry’s ROE to weaken due to government interventions since the sold product is replacing goods [Petrol, and LPG] that are part of political manifestos.

Isn’t the government intention the same i.e to replace petrol, how can the govt intervene against their own intentions?

Petrol is a letdown for countries like India, which imports most of the product as capital outflows from the country, hence such countries are doing more to support EV & Solar industries in an attempt to become self-reliant.

Another factor is the environmental concern hence anyone & everyone who doesn’t own petrol will always prefer the alternate

Right now, regulations are evolving and supporting the businesses. However, once CNG is adopted by the masses over the next 5~8 Yrs, govt. may cap (my assumption) the pricing power of such businesses. Hence, ROE would be impacted.

I take a slightly different view on adoption, looking at Maruti’s CNG plans:

"Further Elaborating on the uptick in preference for CNG vehicles in the country, Srivastava said that Indian customers are very sensitive towards running costs of their cars. “That is where CNG cars come in, there is so much demand for CNG cars right now,” he added.

He noted that CNG car sales are also growing as new cities are getting added to the CNG gas distribution network. “There used to be only 1,400 filling stations, now the figure has crossed 3,300 mark and is slated to touch 8,700 mark in next 1.5 years,” he said. By 2025, the figure could touch 10,000-mark."

I think this will create a bit of a flywheel: more stations → more convenience for CNG cars → higher CNG adoption → more interest in setting up CNG stations by franchisers → …

Personally, valuations don’t seem demanding for 10x TTM P/E for a cash-cow with subscription-like revenue characteristics, on the right side of energy tailwinds, with very high returns on capital. Growth is the key risk of course along with government interventions, but the price does not seem very high and the management has generally been pretty transparent on these.

Disclosure: currently the largest holding in portfolio