Maharastra Natural Gas Limited is the company supplying piped gas if you are talking about Pune. Its not GGCL.

Regards,

Suhag

Maharastra Natural Gas Limited is the company supplying piped gas if you are talking about Pune. Its not GGCL.

Regards,

Suhag

As far as I know, Pune CGD is with MNGL in which IGL has a stake. Can you cite any link in which it says Gujarat Gas is developing Pune?

Well if what you say is true, there aren’t any good prospects for the company in the 9th round of CGD bidding. But I’m still trusting the mgmt for the time being when they’ve said they’ll bid for approx 20 cities.

http://www.pngrb.gov.in/pdf/cgd/bid9/Ninth%20Round%20CGD%20Bidding-Press%20Release-10.07.2018.pdf

http://www.pngrb.gov.in/pdf/media/PNGRB_Presentation_9th_Bid_Round_New_Delhi.pdf

http://www.pngrb.gov.in/pdf/media/EY_Presentation_9th_Bid_Round_New_Delhi.pdf

Technical bids will be opened b/w 12th to 18th July.

95% of the current 91 GA’s are situated in the west and north, there are hardly any in south. In the 9th round, most of the GA’s are going to be opened for the eastern & southern areas.

More than 400 bids received - historically however, only half of the GA’s offered were awarded ( 56 out of 106 ). So assuming the same trend - out of 86 offered maybe 40-45 will be awarded.

Best

Bheeshma

Some one mentioned MGL has not bid for any geographies which seems incorrect

RIL has withdrawn its bids however Adani IOCL combine has bid for 52 cities!

Anybody got an idea how many did MGL bid for?

I was not expecting that the bidding process will be less competitive than what it is since the value of these licenses is quite lucrative!

But in this humdrum we shouldn’t lose sight of the underlying opportunity of Natural gas consumption in the country. Once the dust settles, the winners will rule their respective markets for decades! One can only hope one is invested in the winners

Details of bids of other subsidiaries of GAIL, Mahanagar Gas Ltd and Gujarat State Petroleum Corp (GSPC) remained unknown

The details of bidders who are qualified at the technical level are being released and updated on the website

http://www.pngrb.gov.in/cgd-network-bid-2018.html

So far, MGL has bid for southern districts and i could find 3 bids by it

Best

Bheeshma

Thanks Bheeshma. This looks huge opportunity for the allied sectors as well like pipes, construction etc. Given the size and awarding at near future which are the company that can be looked at related to this theme?

Thanks

Ram

Interesting. Circles of Andhra and TN are very lucrative and naturally there are more than 10 bidders fighting it out there. Could see even Petronet LNG there. So eventually different entities of GAIL are trying to outbid each other here.

Regards,

Suhag

1 TOTAL BIDDER 15

2 TOTAL BIDDER 10

3 TOTAL BIDDER 5

OUT OF 86 GEOGRAPHICAL AREA, COMPANY APPLIED FOR ONLY 3 GAs AND OF THESE THREE THERE ARE 15, 10 AND 5 OTHER BIDDER IN THE COMPETITION ! ISN’T IT SHOWS THAT SOMETHING IS COOKING BETWEEN PROMOTERS?

I think one needs to see the population of these districts and vehicle count to get a sense. Its good that the excess cash with the co has a target now and these are interesting times for cgd entities with all these large scale investment opportunities. We will have to wait till oct to see what the final outcome is.

I think mgl is not that expensive and prices have fallen way below intrinsic value and dont know when it will happen but hopeful market reprices it eventually.

Best

Bheeshma

Disc - invested

Other than Vizag in visakhapatnam dist…the other 2 are poor districts and limited sq feet area

Visakhapatnam is the most populous city in Andhra

Vizag 681.96 Sq KM

Vizianagaram 27.90

Srikakakulam 20.8

Hi Bheeshma, just curious to know what the intrinsic value is as per your assessment

Thanks

Hi @Sandeepg

18-20 times 3 yr forward EPS - assuming an earnings growth rate of 3% , should be sensible to pay in my view. Its earnings growth fluctuates a lot with two-three years of sudden growth followed by three - four years of tepid or flat earnings. The 2017 and 2018 have been good so maybe it would be prudent not to expect much earnings momentum going forward, so 3% is good. With these assumptions - Rs ~1000 should be a sensible price to pay. Ofc, if results are good it would be nice but difficult to say at this juncture.

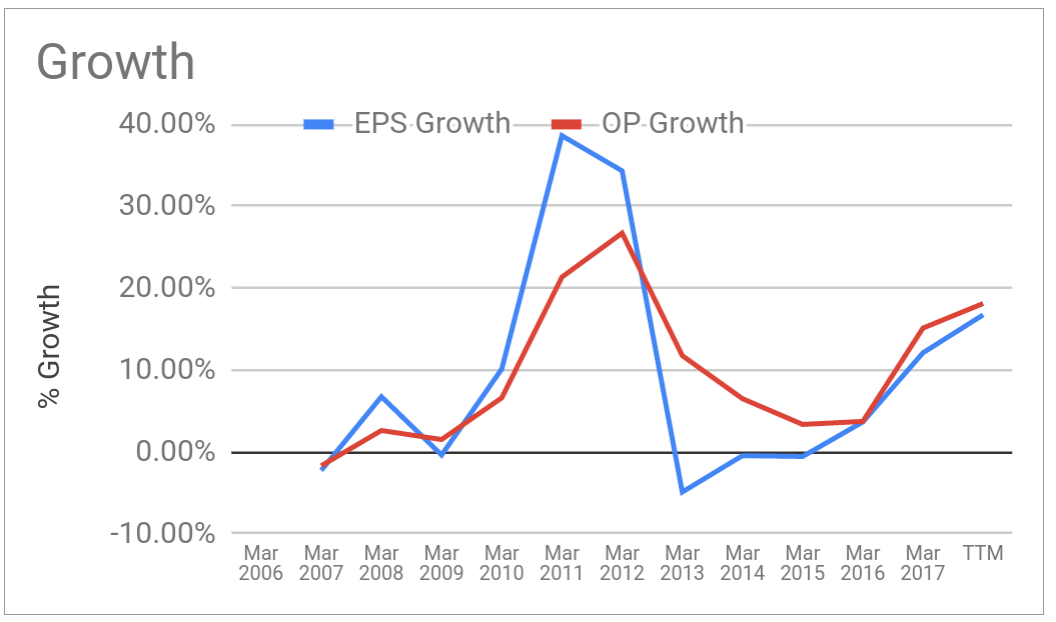

| Item | Mar-07 | Mar-08 | Mar-09 | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| YoY Growth in Earnings | -1% | 7% | 1% | 10% | 40% | 36% | -3% | 0% | 1% | 3% | 27% | 21% |

Best

Bheeshma

An interesting piece I came across today to understand the economics of CNG, PNG and its comparative advantage over conventional fuels like petrol, diesel and LPG cylinders.

Some points in summary:

I spoke with an IGL executive some days back and he said it takes around 1.5 to 2 months to fit a new connection. Frankly, I think this is a lot!

But he also told me they give an option to convert upfront cost of 6k in EMI of 500 pm. Think that’s good to motivate people to come on-board.

Does MGL do something like this if anybody knows?

Mahanagar charges 6500 out which 5k is refundable deposit . I think they had an emi scheme not sure will check my mgl bill

Just went through their latest annual report and earnings call transcript.

Here are my findings:

Pros:

Risks

Overall, this is a boring business with just same old stuff done with a simple demand-supply equation. But, with demand being consistent, boring is definitely good. I think this has a good potential to yield about 15% CAGR with the current business and with growth kicking in (aggressively expanding to other cities), I assume it could be as high as 20-25% CAGR.

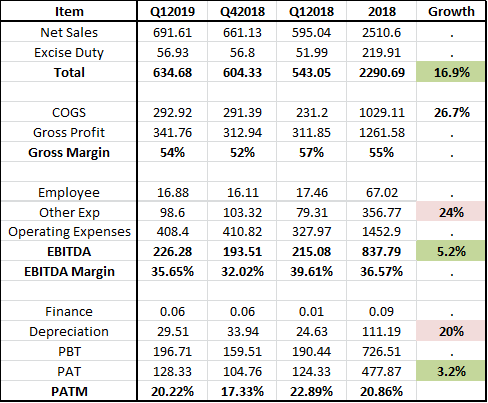

Mixed results by MGL. Sales growth of 16.9% & PAT growth of 3.2%. COGS has increased 26.7% leading to a reduction in gross margins from 57% to 54%. Other details are a show cause notice by PNGRB for slow work.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2eba5729-3318-4842-bc94-16f4e6c68bba.PDF

Best

Bheeshma

The numbers broadly look decent. Good to see a volume growth of ~12%, as I was expecting a growth of ~10%. The fall in gross margins is a bit of a dampener, but I think the hike in prices by MGL in June, should support the margins, going forward.

Regards

SJ

The sales for the current current quarter is adjusted by certain prior period trade discounts of nearly 13 Crore - this is for the period Q1 2015 till Q1 2019 - if you consider this being a ratable charge over that period - the actual impact on the current quarter should have been less than about 50 lakhs(on both top and bottom line). If you normalise the sales and PAT for this one time impact the margins and PAT should have been up by another 1.5%.

Thanks,

AJ

Disclosure: Invested.