Magna Electro Castings Limited (MECL) is a micro cap company with market capitalization of just 67 crores.

Manufacturing started in the year 1990 by Mr N Krishna Samaraj, who has more than two decades of business experience.

Magna Electro Castings Ltd is in the business of Manufacturing & Supplying Ferrous Components in small and medium volumes to users worldwide.

Promoter details:

Company promoted by Krishna Samraj, who also the president for Institute of Indian Foundrymen (apex body for foundry in India). Promoter stake is increased from 36% in 2013 to 43% by 2016, surprisingly ELGI EQUIPMENTS also holds nearly 2% stake in company.

MECL Business & Product Overview:

MECL mainly engaged in the business of manufacturing & supplying ductile and grey iron castings in the weight range of 300 grams to maximum of 2000 kilograms. MECL also manufactures fully machined components from its in-house CNC machine shop. MECL caters to various end-user industries like auto, locomotives, valve, windmills, transmission, etc. The company has wind mills with aggregate capacity of 4 MW for captive consumption purposes and the power generated from the same feeds more than 77% of the power requirement of the unit.

The foundry products are used in various industries such as auto, auto components, railways, agro, tractors, textile, cement making, electrical machinery, earth moving machinery, power equipment, defense equipment, and aero and space industry its sustainable growth has become more important today than ever before given the emphasis of the government on “Make in India”.

Sectorial Growth pattern:

India is currently ranked third in global casting production. With an installed capacity of 10 million tonnes production annually and actual production of 7.5 million tonnes last year, it is second only to China(45million tonnes) and the U.S(12 million tonnes). India exported castings worth more than two billion dollars last financial year.

The Indian foundry industry foresees huge potential for growth, both in the domestic and export fronts. But what ails the sector is investment particularly from using the efficient technology upgrade.

The industry has risen gradually to emerge as the third largest producer of castings, the Indian casting industry has grown by over 43 per cent since 2008. This clearly shows the ever growing demand for the products.

Considered as the mother industry for all other manufacturing sectors and requires the capacity to meet the demand. Hence, nearly three billion dollar is the estimated investment needed for the industry to grow to meet the projected growth of 30 Billion demand according to estimates

Positives:

-

MECL is leader is adopting the latest technology in casting division such as 3D printing and Robotics use.

Three-Dimensional (3D) printing, in which a product can be made without a mould or a cast, is going to be the future of manufacturing sector, Indian foundry sector was lagging behind in adopting this fast-emerging technology.

MECL installed Robotic machines for several machine critical operations like fettling, which improves the product quality and solving the skilled labor problem. -

Availability of continues quality power is must for any manufacturing company, MECL power requirements are filled 80% by own power plants.

-

The Plant current utilization capacity of 70% and management also plant adjacent land for further expansion keeping in mind.

-

Magna has been successfully accredited for DNV GL rules for classification thus getting the Ships, Marine certification. This is another growth trigger, which Increases opportunity for getting orders from “SHIP BUILDING INDUSTRY” for supplying parts meeting adverse corrosive atmospheric conditions.

-

Magna has established warehousing in the USA, this facility along with bi-weekly container shipments, allows catering low volume requirements, which enables MECL to supply products just in time, to customers in the United States of America.

-

Implying the quality procedure followed by company, it is not surprising that MECL getting re-certification from the Performance Review Institute, USA, as an Accredited Manufacturer of Ductile and Gray Iron Castings which is mandatory for supply of castings for applications in locomotives, railway engines etc in the USA.

-

Well-established manufacturing facilities with in-house machining capabilities and financial profile marked by consistent improvement in the profit margins over the past 3 years. Its full foundry capabilities for various products sold to the valve, refrigeration, rail, hydraulics, automotive, wind turbine and other industries worldwide.

-

Long operational track record of 26 years in casting business, promoter integrity coupled with domain experience is other added advantage here.

-

Implementation of Thermal Reclamation process in its products manufacturing is going to reduce raw material usage to great extent. MECL has installed Furan Thermal Reclamation Sand Plant at a cost of Rs.200 lakhs for reclamation of sand. This installation will enable the Company to reduce dependence on the availability of sand and reduction of input costs.

-

Management conservative approach in saving the cash resources is evident from the fact that all the expansion and plant up gradation is done from internal accruals rather than debt route.

Negatives:

-

Skilled man labor and implicit cost is main worry for any manufacturing company, but automation, adopting the latest technology and plant upgradtion are some of the initiatives should be followed. MECL is already taken some of the these initiatives in automation using robotics etc. -

High cost of capital: The industry requires investment to the tune of at least $3 billion to meet the increasing demand for castings, estimated at 25 to 30 million tonnes in 10 years. The annual production of castings (both – ferrous and non ferrous) is 10 million tonnes and turnover around $18 billion at current production rates. This is only 10 per cent of global production by weight where opportunity exists. -

Consistent quality power supply is must for these kind of manufacturing process, but currently 77% of power requirements are fulfilled by it’s wind mill division.

Thermal Reclamation technology

Thermally reclaimed sand is better than mechanically reclaimed sand as well as fresh Sand for following reasons:

• Thermally reclaimed sand undergoes lower thermal expansion causing better mould stability.

• Thermally reclaimed sand is better than fresh sand because it is more rounded in shape causing lesser binder demand.

• Irrespective of the binder system in the previous cycle, thermally reclaimed sand can be used with any chemical binder system in the subsequent cycle.

Financials:

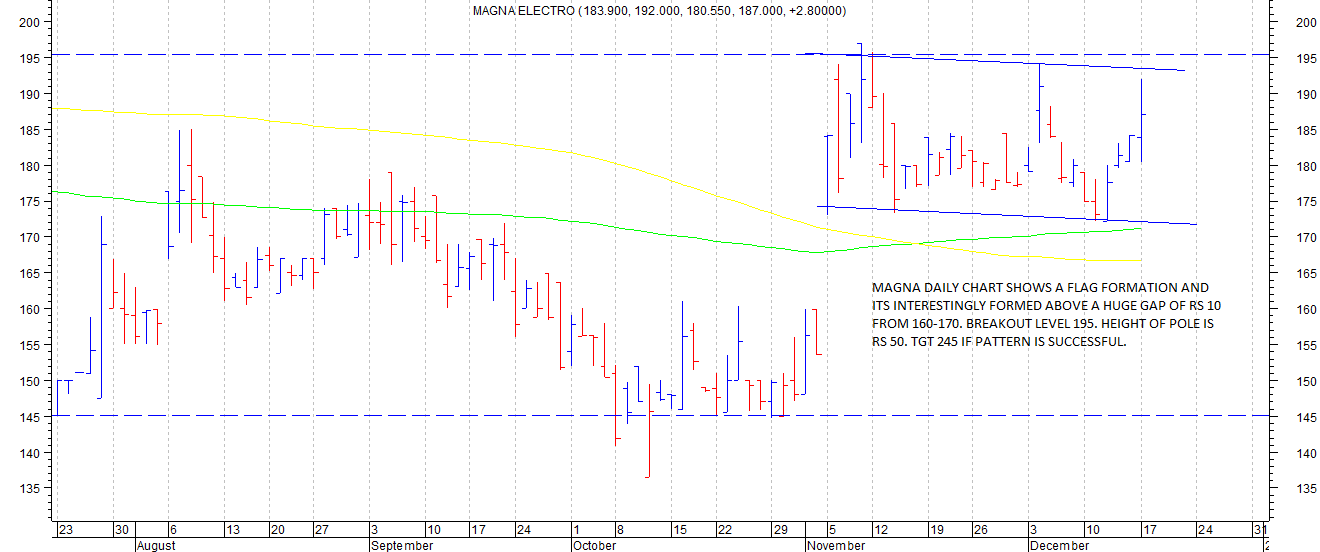

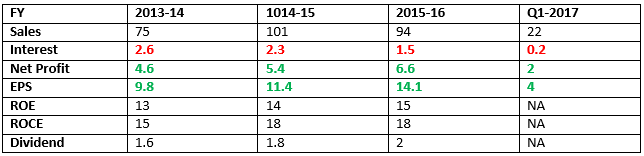

Observation: Reduction of finance costs, improvement in profits, good return ratios and increasing the dividend payout are indicators for any good company, MECL is one such company surprisingly Market capitalization is less than sales. Currently the stock is trading @146rs with an EPS of 15rs and PE of 9.

Disclosure: Hold 1% of my portfolio with an average price of 146rs.