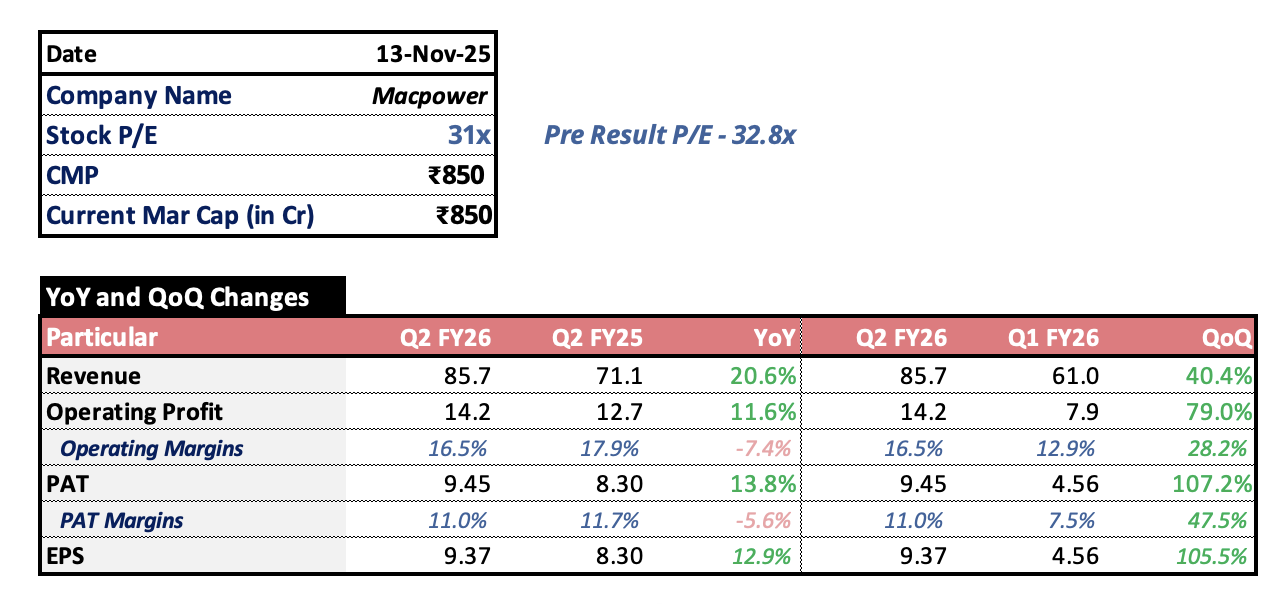

“Dear ShareholdersWe have commenced FY26 on a strong note, supported by a robust order book of ₹346 crore as of June 30, reflecting an 5% increase over FY25. With atypical execution cycle of four to six months, this provides solid visibility for sustained growth through the year.Our ongoing capex plan is progressing well. Phase-wise development includes a new facility focused on foundry, defence, and aerospace lines. Nearly 90%of local approvals for land acquisition have been secured, with final allocation expected in H2 FY26. This site will also act as a strategic base for future JointVentures—talks are currently underway with global partners for technology collaboration and international distribution.On the product front, we continue to drive innovation through automation and robotics. Our newly developed gantry and robotic-enabled models aredesigned for precision and scalability, significantly reducing human intervention.The NEXA series remains a key growth engine, having secured a ₹42 crore order for 160 machines during IMTEX 2025.Our focus areas—defence andaerospace manufacturing, expanded distribution, and strengthened technical and sales teams—set a strong foundation to achieve our ₹500 crore turnovertarget within the next 3–4 years.To support this trajectory, we are increasing our production capacity from 2,000 to 2,500 machines per annum by Q2 FY26. Our distribution footprint hasalso widened to 39 cities with the addition of new partners.Macpower remains debt-free with a net cash surplus, reflecting our strong balance sheet and financial discipline. We continue to prioritize cost efficiency,new product development, and responsible growth.Our unwavering focus on safety, sustainability, and stakeholder value reinforces our long-term commitment to excellence. With a healthy order pipeline of₹346 crore, growing sectoral demand, and ongoing investments in capacity and innovation, we are well-positioned to deliver industry-leadingperformance.

Not happy with only 5% growth in order book.