One another additiona point on this from con call is tier3/ tier4 cients order dispatch is dependent on banks clearing the payments and at times there are delays from banks.

This will not be the case with corporates so payments and order closure would be faster with corporates.

5 Likes

The 100% delivery was since the stock got moved to BE section. Delivery is compulsory in such stocks.

1 Like

Finally, amongst all the concerns about Q3 numbers and delayed concall, Macpower seems to be at an inflection point of it’s growth cycle. Dare I say, Having tracked the company for over two years now- I have been able to pick up some nuances to it’s future prospects:

-

Land Allotment- Delayed or tactical?

The company still awaiting some policy incentives in the budget/scheme. But does this delay really make sense? (Was it possible for them to get it signed without these additional perks?) With massive demand from Tier 1 and Tier 2 customers—reflected in strong order flows for Ace Designers and Jyoti CNC—Macpower’s ₹100+ crore capex (including a 35-acre facility at token rates) and potential 6,000-8,000 machine output getting delayed over a few crores in incentives. Meanwhile, Jyoti CNC is fully booked for the next two years. Despite this, I trust management’s execution and expect FY26 to be a turning point, with a ramp-up to 2,500 machines and larger, high-value orders. -

JV Could Be a Game-Changer: If you want to go fast, go alone. If you want to go far, go together. A joint venture with a foreign player could be a major step up (possible post Gemany Exhibition), especially in high-end machines. Macpower is expanding from 7-8 acres to 40+ acres over the next 1.5-2 years, though scaling such a large setup will take much more time than the 9 months indicated in the concall- Potentially 1.5+ year.

So far, they’ve focused on entry- and mid-level machines (Turning Centers & VMCs), but with the Bengaluru R&D center and the introduction of 5-axis machines, they’re finally moving up the value chain. Some interesting product launches are expected soon, as hinted in recent calls. -

Backward Integration: Building from Within:

In India, backward integration is usually led by technocrats with deep industry expertise. Macpower is moving in that direction, targeting foundry, turrets, automatic tool changers (ATC), rotary tables, and spindles (already 50% in-house). These will be developed at their Bengaluru R&D center. This shift should bring better cost control, supply chain strength, and long-term efficiency. As indicated by large peers and Rupesh Bhai- the industry could sustain 20-25% EBITDA margins as long as the capex cycle continues, provided efficient utilization of the opportunity. -

Large Ticket Size Orders:?

With capacity expanding from 2,500 to 4,500+ machines over the next 1.5-2 years, scaling the order book is a task. Large orders haven’t started flowing yet, but they’re clearly preparing—recently adding 100+ people in sales and service. The next few quarters will be a test of their ability to grow their order book rapidly. They really can’t afford to be at the similar order book intake with such a large facility. A lots of exhibitions and marketing spend can be factored in FY26.

Valuations are a tricky part to comment on in the current market, but even in a highly probable case, if Macpower can do a 45-50 crores PAT in FY26 (which seems achievable with a ₹450 crore capacity at 18% OPM), the current market cap looks attractive coupled with the medium term growth levers.

Disc: Not Invested and No Recommendation

9 Likes

After Q3 result, i have exited 50% from it. For such a small company, missing out on numbers doesn’t fit me.

They knew about Imtex, mgmt could have guided conservatively. But didnt.

Will take next call after Q4

Just my 2 cents.

2 Likes

But by that time if Q4 does beat expectations, then you will not get the share at this price, while you sold at a cheap valuation since the stock crashed.

2 Likes

As far as my experience goes,

With current global scenario, and once investors loses confidence. It will take some time to trust the company again.

It wont get a 50 PE anytime soon.

Have all the rights to be wrong

4 Likes

It depends on how you evaluate the business, its a microcap, so there will be volatility.

Valuation is subjective and some will get it right and some wrong (thats why trade happens…)but if you ignore the noise and focus on what can it be down the line 4-5 years, how things are stacked, you may be able to better judge. Considering large expansion coming up, Industry has a tailwind, and management is capital efficient , I see reasonable runway for the company. road can be bumpy.

But the risk is technology, if their focus is limited to backward integration of fabrication etc, cant expect much.

1 Like

Agree…Fy26 , though has good developments in terms of long term prospects…but the bottom line won’t be smooth and fixed costs will increase because of capex going live and also from what i could gather from concall their exhibition in Germany will result in expenses…Fy27 can be much better year in terms of bottom line visibility with more corporate clients instead of individual msme which depend on bank loans for orders

1 Like

After reviewing my investment thesis and after re-analysing the fundamentals of Macpower I exited from this scrip because of the following reasons (I may be completely wrong):-

1, Strength of Balance sheet is deteriorating because of continuous increase in inventory and debtors from last four years while surplus fund investment is reduced significantly in this period. Anyone can see it on screener.in.

2, It looks like Macpower is facing tough competition from players like COSMOS in entry level cnc machine ( management also accepted it on last concall ) and on higher end cnc machines, company is not getting any traction among established players in this field.

3, Hyper emphasis on Land procurement from Gujarat Govt. by the managment and deliberately highlighting the market value of that land. In earlier concall, they told that market value of that land was 70 to 80 crores and now they are telling its value is Rs. 120 crore. It seems that any JV or technology transfer from foreign companies is totally dependent on that land parcel as well as any fund raise.

4, In my view, even after the getting the land parcel, Macpower will need JV or technology transfer from foreign company to raise fund for capacity addition up to Rs.100 crores. Even after showing Macpower’s capability in Imtex 2025, it seems, till now, that company is unable to convince any company for JV or technology transfer.

5, One side Rupesh Mehta wants to establish Macpower as an import substitution and other side he is considering to export CNC machine to sanctioned country like Russia even after knowing that what happened to Lokesh Machines ltd.

6, On execution side, even after showing strong order-book and industry tailwind Rupesh Mehta continuously failed to walk the talk from last three quarters. Consequently, market is punishing the valuations.

7, Few other red flags are Sudden retirement of CFO as on 31 Dec 2024 instead of waiting till FY ending on 31 mar 2025, fire incident in Feb 2025 in unit-2, delay in presentation of PPT and concall after bad Q3 results etc.

Disclosure: - Exited and may re-enter in future if management walk the talk. It is not a buy/sell or hold recommendation.

6 Likes

Point 1 - While true, revenues and profits have risen as well over the past 4 years.

2. I do not think management confirmed tough competition. Obviously competition will be there, but Rupesh is trying to indicate that moving to more RnD driven manufacturing is key to grow.

3. JV is dependent on fund raise as they will need new capacity for this right? Management said that expansion will happen regardless of JV happening in last call so point 4 that they were not able to convince for JV does not add up as land acquisition is the key here. They are debt free, so taking on new debt is not too bad of a thing thought will impact profits in the short term.

5. Didn’t Rupesh say that apart from the 42 cr bookings they got from Imtex, there were more that they haven’t gone ahead with due to the ethical issues? Also the 42 crore bookings is only from Imtex. There would be many who could book later after coming to know about the company. So we cannot take 42 crore as the only measurement of how successful IMTEX was for them.

6. Yes, December 2024 execution was bad but I believe every company should be allowed to have a bad quarter. The management has guided for best ever March results and order bookings have gone up. Inflow did get affected due to IMTEX so that is one thing to check next quarter. I would say lets see how management walks the talk next quarter and honours the promises made this time around.

7. I think only the CFO removal should be considered as a red flag. I have seen companies that don’t even do calls and ppts when things go south. And the fire incident is just an unfortunate situation. Also wasn’t it retiring rather than resignation? So the CFO removal doesn’t look that bad as well.

6 Likes

I met the CFO personally in July 2024 and had a 1 hour discussion around many topics. Prima Facie looked like a really old man, looked more like 70+ to me easily or even more, white hair, thin, fragile gentleman. If anyone is really interested to dig deeper you could write an email to the CS and find out his exact age at the time of retirement. Though i never asked him his age, my questions were more based on the financials and forensic checks and how well versed was he with the financials, or how quickly he can respond to them. I did not find any issues. Hence rest my case.

4 Likes

Some interesting observations regarding the company & plausible ones. Just on the CFO part, I think we might be reading too much into it ![]()

As @gauravpersonal pointed the respectable man was old enough to retire & the same was the reason. He retired at the age of 68 & his replacement is also a person who’s been with Macpower for years.

Apart from that have nothing to add to the thread. A 90-100 crores quarter & a follow up good one in Q1 with a strong order book might again tilt the balance.

The only thing old investors can do is watch or latch to some other opportunity & the only thing new investors can do is latch( in case it fits their thesis)/ pass the opportunity.

The three things we can keep in mind is the scope of the industry, the competitive spirit of the promotor, the ability to scale with management retaining its integrity.

Of course one can’t ignore valuation. Right now the valuation seems cheap but cheap can become cheaper just like it seemed decently valued when it was soaring with ever highest quarters & the bright future seemed to get even more brighter ![]()

P.S. Have I been disappointed & the answer is yes. But then that’s part of investing. The drawdowns are part of the journey. For a small cap there’ll be periods of building. The market was in momentum mode but then what has not crashed ![]()

Disc: Invested, biased & no recommendation.

13 Likes

Some information on duty on imported machines :

The import duty on CNC (Computer Numerical Control) machines in India depends on the classification of the machine under the Harmonized System (HS) code. Here’s a detailed explanation based on CNC machine categories:

1. CNC Machines – General Duty Structure (HS Code 8466)

This is the category most CNC machines fall under, and it generally covers machines for milling, turning, drilling, grinding, and other operations in various forms.

- HS Code 8466: “Machines for working metal by removing material, other than the machines of headings 8456 and 8457.”

- Basic Customs Duty (BCD): 7.5%

- Integrated Goods and Services Tax (IGST): 18%

- Social Welfare Surcharge (SWS): 10% of BCD

Total Duty: Approximately 35% (Including IGST, Social Welfare Surcharge, and BCD combined).

2. CNC Turning Centers & Milling Machines (HS Code 8456, 8465)

CNC turning centers and milling machines are generally classified under the machinery headings like 8456 (machine tools for working stone, ceramics, concrete) and 8465 (machines for shaping or molding materials).

- HS Code 8456: Machine tools for working metals by removing material.

- HS Code 8465: Machines for working stone, ceramics, concrete, and shaping rubber or plastics.

- Basic Customs Duty (BCD): 7.5%

- IGST (Integrated GST): 18%

- Social Welfare Surcharge (SWS): 10% of BCD

Total Duty: Approximately 35%.

3. Used CNC Machines

For used CNC machines, the import duty is typically higher, as India is keen to regulate the influx of second-hand machinery. Used CNC machines are typically classified under HS Code 8207 (Interchangeable tools for machine tools).

- Basic Customs Duty (BCD): 10%

- IGST: 18%

- Social Welfare Surcharge: 10% of BCD

Total Duty: Approximately 30.98%.

4. Specific Exemptions and Concessions

- Machinery for Manufacture of Exempted Products: In some cases, CNC machines used for the production of certain specific products may qualify for a concession or exemption under special schemes. For instance, machinery used for export-oriented units (EOUs) or in certain special economic zones (SEZ) might benefit from reduced duty rates.

- Technology Upgradation Fund Scheme (TUFS): The Government of India offers financial assistance under this scheme to upgrade machinery for the textile sector, including CNC machinery. While this scheme primarily provides subsidies, it can also influence import duty rates for specific

6. Additional Costs

In addition to customs duty and GST, there may be additional costs like:

- Countervailing Duty (CVD): Imposed on some goods to offset domestic taxes and duties on equivalent goods.

- Freight and Handling Fees: These are specific to the port of entry and the logistics involved in transporting the CNC machines to India.

Conclusion:

To summarize, the import duty on CNC machines is typically around 35%, including a 7.5% basic customs duty, 18% IGST, and a 10% social welfare surcharge. The duty may vary based on the machine’s classification, whether it’s new or used, and any special exemptions or concessions that apply to the sector. For accurate and up-to-date information, it’s advisable to check with India’s Central Board of Indirect Taxes and Customs (CBIC) or consult a customs clearance agent.

2 Likes

Agreed that management should have given better guidance (especially for Q3 since they knew production capacity being diverted to IMTEX). Also the fact that they had to reduce client deliveries to prepare for an exhibition shows constraints on all kind of bandwidth - capacity, technical and management bandwidth.

However, what gives me comfort is that management did not use the bull run to dilute stakes. They are still quite conservative on maintaining healthy balance sheet.

It will take a few quarters of consistent delivery to gain market’s trust again. I hope the management learns the lessons and implements them.

Disc - invested.

2 Likes

I agree & one of the observations for me though I missed writing it out was that the promotor didn’t sell at the peak & leave aside that even when he knew that performance wasn’t going to be great.

Now getting big orders has been a visible challenge for them & somewhere feel they are trying everything to get as many orders as they can & have even ventured into developing new machines. Add to that the Opening of new centres, participating in exhibitions, exploring export, etc etc.

How these initiatives help, it’ll take a couple of quarters to see any tangible changes.

It’ll test the patience & even the conviction, so it’ll all depend on one’s investing style & needs from their investment.

1 Like

Yeah, management is too conservative, lack of ability to think far ahead.

Otherwise these constraints could have been met. IMTEX is not a new event.

Kindly share your views on From Machine Sales to Manufacturing-as-a-Service

3 Likes

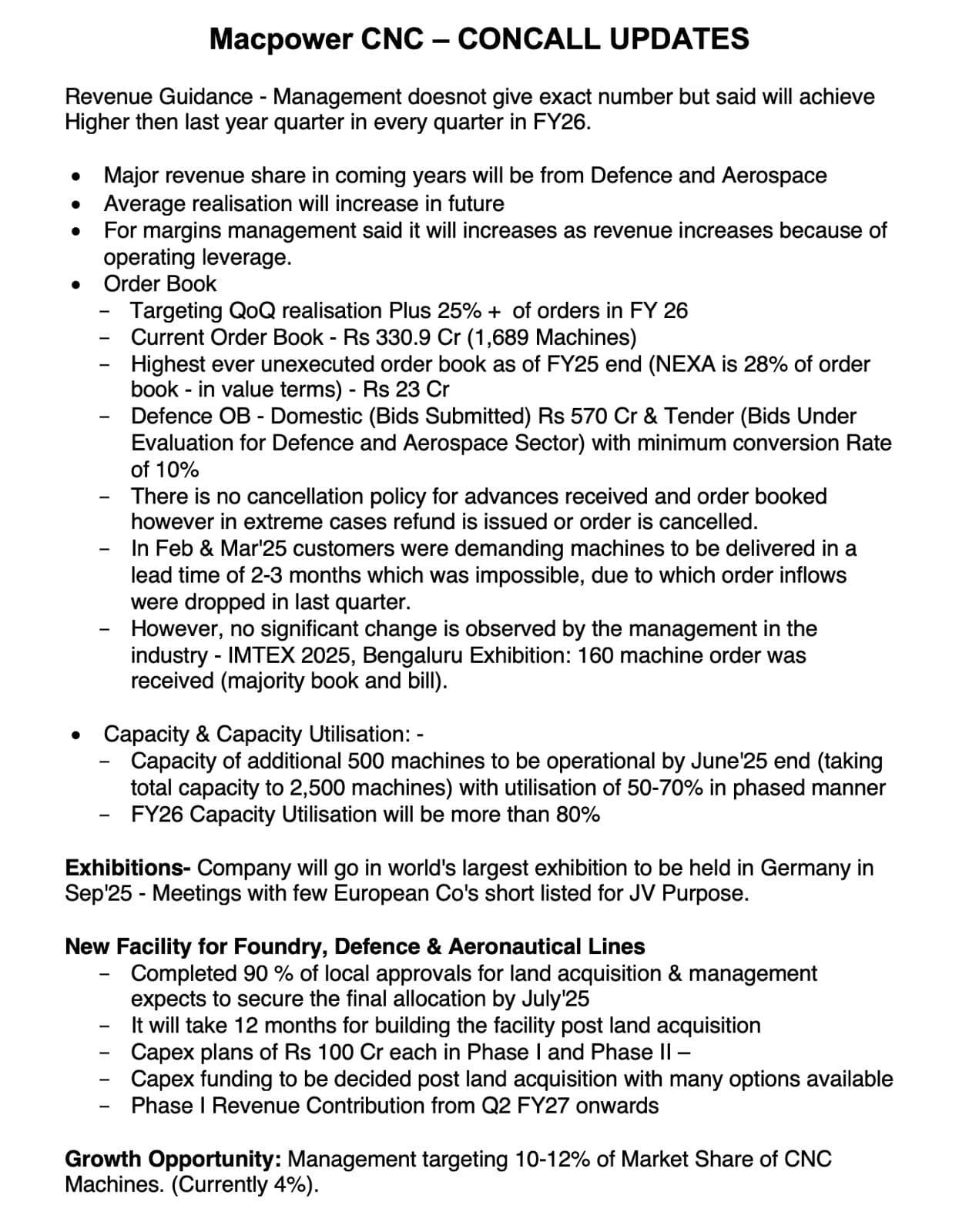

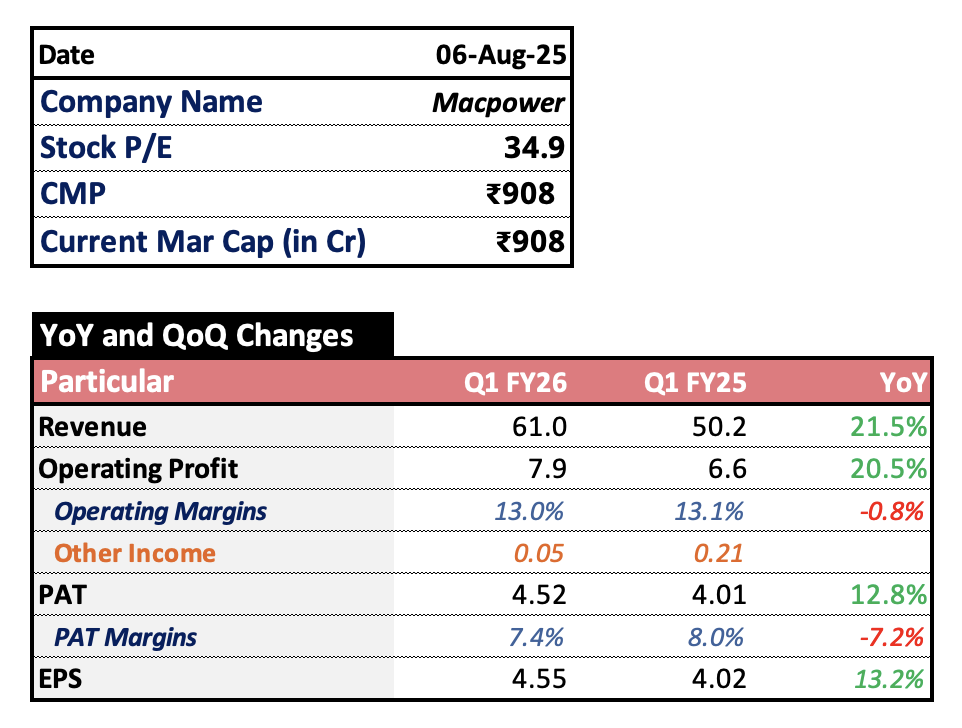

Q1 FY26 Results

- Decent set of numbers from Macpower.

- Highest ever topline in Q1 till date.

- Topline increases 21% and 13% Bottomline growth.

- Margins are not inline with topline because of increase in employee costs and Depreciation.

6 Likes

They are very decent results and I am pleased. Hoping that order book has grown too. Employee expenses and depreciation are anyway necessary to fuel growth so can’t complain.

Awaiting order book info and guidance

3 Likes