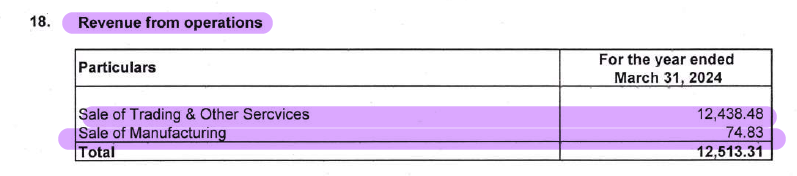

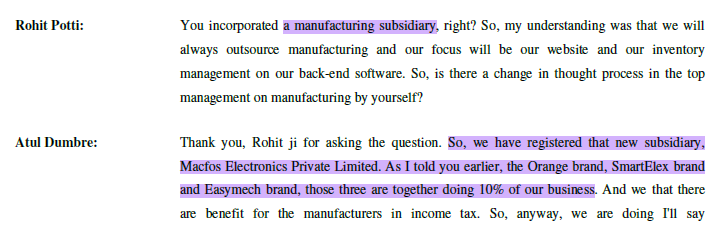

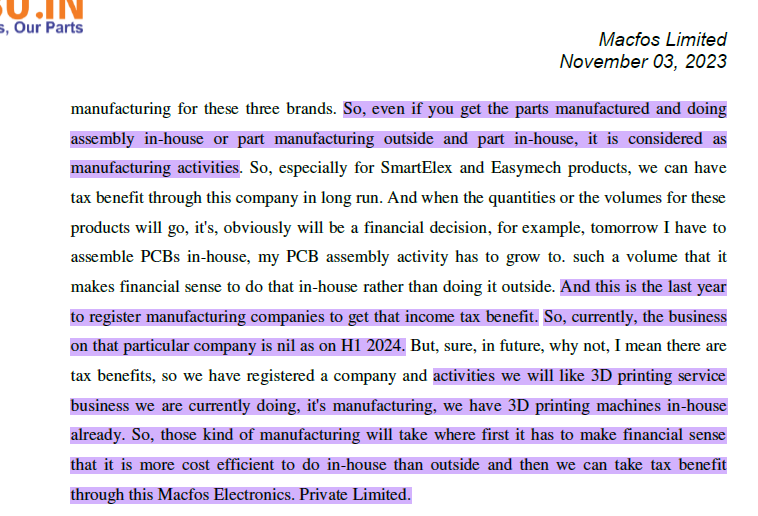

Formation of manufacturing subsidiary doesn’t mean that significant actual manufacturing is happening there. Please see excerpts from transcripts and annual report.

…

Anyway, my question was about R&D and not manufacturing. Also, I think there are gaps in information given that revenue is from 12 categories whereas purchases are entirely from five categories.

2 Likes

Don’t know why the numbers don’t add up. Can’t trust smallcaps too much.

Competition is huge in retail sector, even amazon has tough time squeezing margins if we exclude AWS business. Amazon India and Flipkart are still in loss, same case for most retail sectors.

If this company wants to grow it needs huge capital. And for manufacturing also they need huge capital.

Even the crisil report says capital requirements are risk in this company.

I don’t understand why FII and DII aren’t buying it either.

What are your views on long term margins of this business?

Let’s say once it matures 10 years from now what margins they will be making?

5%

10% ?

2 Likes

Presently they are working on 10% PBT margin. Cost of material is almost 80% of the sales value. As inventory turnover is high, above 6; they are maintaining a decent ROE.

-As sale increases they will get some economy of scale in procurement, and the figure 80% should decrease going forward. Thus, per unit profitability should go up.

-Almost 5% cost is there towards advertisement, rent, shipping etc. This should go down with ecnomy of scale.

-As number of SKUs is likely to increase, inventory turnover should reduce. However, higher SKUs will give competitive advantage to the company and greater pricing power.

-With introduction of self branded/ manufactured products, profitability should go up.

I think, they can sustain the profitability going forward and 10% PBT margin is not likley to reduce going forward. In fact it can go up by a few percetage points.

Rest, nobody knows the future.

3 Likes

If anyone attended today’s AGM, plz share the notes.

Thanks

3 Likes

how can someone like an retail investor attend an AGM.

- Did Macfos gave the link to join?

- is it general practice for every company to share the link?

My husband is a long time user of Robu. He recently mentioned that the service side of the business has rather deteriorated and quotations aren’t being attend to as promptly as it used to. This has been the experience for the last few months now. Earlier service was a differentiating factor in favor of the company. I believe theyre facing a scale issue of maintaining service.

Position- Took an exit a few months ago

7 Likes

Please check your inbox for an Email from:

evoting@nsdl.com

Dated:

Aug 7, 2025, 6:25 PM

Subject:

8th Annual General Meeting (‘AGM’) of the Members of Macfos Limited to be held on 29th August 2025 at 03.00 p.m. (IST) through two-way Video Conferencing (‘VC’) facility / Other Audio-Visual Means (‘OAVM’).

The content of e-mail Has a Link to:

PDF at Page 7/30

THE INSTRUCTIONS FOR MEMBERS FOR REMOTE E-VOTING AND JOINING THE GENERAL

MEETING ARE AS UNDER :-

1 Like

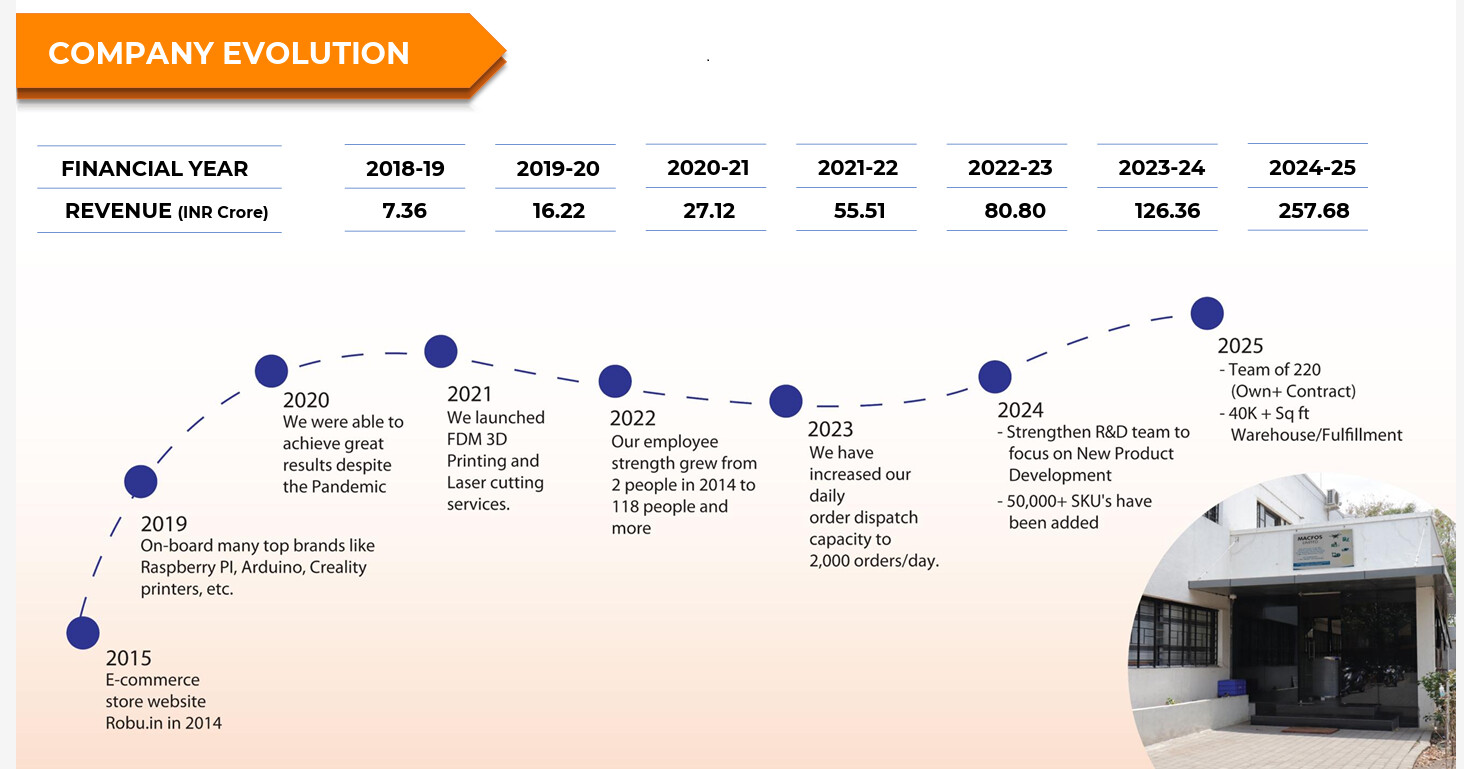

Macfos has come out with great results. Topline has gone up to 69 crores with with 6.8 crores of PBT. The results look weak as compared to last year due to one time order received last year.

Macfos.pdf (5.4 MB)

2 Likes

Has the company announced what percentage of the topline this time around was due to one-time bulk orders (or conversely, if the entire topline was non-bulk)?

Disc: Not tracking any longer.

1 Like

Last year one time bulk order was of 70 crores value, and 3 crores profit (profit margin was less in that order). If we remove this figure from 2025 results, Macfos topline was 185 crores and net profit was 15 crores.

In the present financial H1, the company has achieved a topline of 128 crores with PAT of more than 10 crores.

If we take 10 percent quarterly growth, in the current financial year the company is likely to achieve a topline of 280 crores with 23 crores of net profit.

But aint whole point is to increase bulk B2B order, as retail is mostly taken care off.

Macfos has come out with investor presentation.

-Total SKU has been increased from 71k (March 2025) to 102K (Sep 20250

-Average monthly website visitor is up by almost 25%.

-Total number of order served in more than 238K, up by 30 percent over corrosponding period last year.

-Average order value of INR 5365, up by 20% over corrosponding period last year.

On all the parameters, the company is doing well.

MacfosIP.pdf (3.3 MB)

The company is growing at a consistent rate of 50%. 2024-25 was an aberration because of onetime bulk order. If we remove that, the company had a tunover of 180 crores [Total number of orders multiplied by average order value; 396K*4632]. If the company achieve 280 crores topline this year, it is consistent in growth. The investor presentation shows that Robu2 is also progessing well.

As the company is growing at a very fast pace, it needs capital. Number of SKUs is growing and hence the company is forced to keep bigger inventory. In this H1 financials, the inventory level has gone up to 71 crore from 56 crores. Due to higher inventory, cash flow is likely to be negative in foreseeable future. From the Investor presentation, it is clear that the company is maintaining inventory obsolescence well. Probably the company has to be careful in this area.

1 Like

Retailer sector generally has low margins due to high competition, I don’t think more than 5% will be feasible in the long run, same as case of amazon or nykaa.

Position: took 100% exit about a month ago bcz this slow growth is not worth the risk in my opinion. I am still watching the quarterly (which is stagnant) results though.

1 Like

Macfos( robu.in)

(Fundamental analysis by-Dr pragnesh shah)

BUSINESS

1…E -retailing(45%)

Macfos is engaged in e-retailing of electronics items through its e-commerce store website ‘Robu.in’ and mobile applications.

2…B2B-offline channel(55%)

-Under the offline channel, we generally serve Corporates and SME

-In 2014, company started as totally a online store. We did not have any corporate customer per say, we were totally focusing on online sales or retail sales, B2C sales, for

first four or five years of our journey. And through the journey we realized that there is a lot of industrial customers who need the support as well as our products.

-And then we formed a corporate sales team around 2019 and started to sell to corporate customers.

-Our corporate sales around 2019-‘20 times where odd 5% of total sales.

Five years from that moment, today our corporate sales are almost 50%, half of our business.

PRODUCTS

Specialized E-Com Store for electronics items including

-Robotic parts,

-Drone parts,

-E-bike parts,

-IoT & Wireless items,

-3d printer & parts,

-Laser cutting

-DIY learning kits,

-Development boards,

-Raspberry Pi

-Sensors, Motors, Pumps,

-Batteries and its chargers, -Electronic modules & Displays

CUSTOMERS

Their business model (Robu 1.0) targets:

B2C (online) @ hobbyists, Students

B2B bulk supliers@ SMEs, startups

1-Students/hobbyists

2-Educational institutions,

3-Researchers and Developers

4-Engineering R&D labs

5-College robotics clubs

6-Startups (electronics, IoT, robotics, EV, drone, deep-tech)

7-Small & Medium Manufacturers (SMEs)

8-Early-stage hardware companies

They are NOT primarily serving:

-Big industrial giants

-Large OEMs

-Big mass production companies

Startups and SMEs form the largest share of B2B volume.

Given the above business model, here’s how startups (especially in hardware / electronics / robotics / deep-tech) can leverage Macfos / Robu:

- Prototyping & R&D Support

-Startups building hardware need a reliable source for electronic components: sensors, development boards, motors, etc. Robu.in provides a very wide range.

-For product prototyping, their 3D printing & laser cutting services can be very useful. Rather than outsourcing to many vendors, a startup can consolidate much of its prototyping with Robu.

- Supply Chain for Low to Medium Volume Manufacturing

-New hardware startups often don’t start at large scale. They may need small-to-medium volumes of PCBs, batteries, mechanical parts, etc. With Macfos supplying a broad catalog + offering PCB/lithium battery pack services, they can act as a flexible supply chain partner.

-Because they have a strong vendor network (210+ vendor tie ups per one of their presentations) , they likely have good relationships to source both standard and specialized components.

- Cost Efficiency & Inventory Options

Startups may not have large capital to hold big inventory. Buying via Robu’s platform might be more cost-effective than tying up with large distributors.

Having a single partner (Macfos) for a variety of parts reduces the complexity of managing multiple supplier relationships.

==========================

MOATS

1…EXTENSIVE & DIVERSED

PORTFOLIO OF ELECTRONIC ITEMS & PARTS (HIGH SKU)

=80,000+ SKU’s

=Competitive Landscape: Management claims no direct peer in India matching breadth (~80,000+ SKUs).

=Robu.in is positioned as a comprehensive one-stop store.

2…TECHNICAL SOLUTION PROVIDER

(Not just trading firm, Need to keep compatible Right products in right quantity)

= So for example, if you want to make a drone, you don’t just require motors. You require 20-odd products which are compatible with each other. And then you have to keep those products in optimized stock to serve the customer at the right point in time.

=So that is a way beyond trading. That is not just buying a motor and selling a motor. We believe that we are a technical solution provider kind of in our business sense. And I think that helps because we are technical people and we know our customers requirements. And we act on that basis.”

=Right product in right quantity, which gets rotated in 2.5 months to three months

3…BRAND

=There are five lakh people visiting our website every month, website plus app combined.

=So it’s just like building a brand.

4…UNIQUE PLACE FOR SMALL BULKY ORDERS

=For Arrow/Mouse/digikey, this business is

-Too small bulk business

-High shipping times, customs, MOQs (minimum order quantity), higher price for low-volume are other problems for these international giants

=These are the reasons why big companies will not enter in this business(Big fish in small pond)

COMPETITIVE EDGE

A…Why digikey, arrow, mouse will not compete or less compete for B2B

=Very small order value in compare to their global business

=High shipping times, customs, MOQs are other problems

B…Why superior to other online(robocraze, robokits,thinkrobo )

=Robu.in has highest Sku

=Due to higher sales, robu.in can give high discount offer

=Brand perception

C…Why amazone will not enter

=Very small market

=Need to keep high sku

=All these sku need to be compatible products

=Need high inventory that may decrease ROE

D…Edge over retail shops

=All products(even rarely used) available under one roof

=Robu has around 100000 sku.

Such high sku in physical store is not possible

=Can give more discount as like amazone due to higher sales

=Shops are not in every city

Retail shops are only in metro, small cities students have to buy online only

E…WHY B2B WILL NOT DIRECTLY BUY FROM MANUFACTURER

Why a large-scale enterprise customer who may be purchasing these products in bulk

would come to Robu and come to Macfos for its procurement requirements rather than doing it

direct?

a)…Authorized channel partners in electronic channel partner

(Manufactures dont sell directly)

=Bsically when you go into electronic distribution model, generally, a large-scale customer have,

even the small- or large-scale customers have to buy from the authorized channel partners

because the principle or the company who owns the product, they really do not want to get into

the local distribution country-wise.

= Their key strength is designing and developing these new

products and bringing them to the market .

=Yes, whenever there are

higher volumes, there are generally triparty meetings, the one with principal who owns the

product, the distributor who is Macfos, and then the customers.

b)…Support

And secondly, they need

N number of support

- If the product is not working they need some support locally

-who would support them, if they require small quantities because their production has increased a little bit

more at the last moment,

-Who will support if their product is not proving to the exact specifications where they want it to be.

-Or the credit terms, how would the manufacturer or supplier, let’s say, sitting in Europe will give credit terms, and if the payment is not served by that customer, how would they go about it.

So, all those kind of small things are taken care by local distribution.

So for all these practical reasons, generally, the thumb rule is they go with distribution partners.

======================

===========

COMPETITIORS

1…DOMESTIC

-As per management, "we do not see a single competitior, because we are doing multiple segments, around 70,000 SKUs as of today. So we have the most comprehensive portfolio.

2…INTERNATIONAL

-Three or four big players who are Arrow, DigiKey, Farnell, Mouser. So internationally, we believe that these are more of similar business

models.

A…We have stocking in India, so we have leverage in that.

B…These companies are mainly oem/large order suppliers

3…PHYSICAL STORES

Online business has clear edge above stores,as we discussed already

COMPARISION WITH DIFFERENT INDIAN ONLINE COMPANIES

A…REVENUE

1…Robu.in@ 255 cr in 2025 revenue

(32-38 million usd)

@200 employees

2…Robocraze@ 25cr

(3.2 million usd)

@ 50 employees

3…Robokitz@35 cr

(4.2 million usd)

@55 employees

4…Digikey india@

very less 1 cr revenue in 2024

=banglore team plans to 300 employees in next 3-5 urs

5…Electronicscomp.com

-13cr

6…Robotics dna

-Started in 2024

-employees@1-10

7…Sunrobotics

-14 e.ployees

-Rev@ 50lkhs to 1 cr

-Started in 2021

8…Flyrobo

-5 employees

-10lkhs

9…Thinkrobotics

-12 employee

-56cr

10…Indian robostore

-5-10cr

-7-10 employees

B …Daily web traffic(june 2025)

1..Robu.in@75000/day

Indian traffic Rank 2250

2…Robocraze@ 17000/day

Indian traffic rank@11090

3…Robokits@2000/day

Veru low traffic

4…Thinkrobotics@NS

Very low traffic

C…Playstore

1…Robu.in@5lkhs+

2…Robocraze@10k+

3…Fly robo@10k+

4…robokits@ no app

D…Youtube subsrber

1…Robu.in@44000

2…Robocraze@ 9500

3…Robokits@3700

4…Thinkrobotics@635

E…Insta

1…Robu.in@64000

2…Robocraze@30000

3…Robokits@negligible

4…Thinkrobotics@13400

F…starting yr

Robu.in@2014

Robocraze@2016

Robikits@2007

Thinkrobo@2018

============

GROWTH TRIGGERS

1…Increase SKU

=Robu is one stop solution for all

=Many times, this is the only site where customers can buy products.

=Customers will not buy one product from this company and other products from different one.

=So ultimately, increasing sku will attract more customers and it will make strong moat for company

2…INCREASING B2B BUSINESS

5%@ 2019

50@@2025

Historically focused on online/B2C; now strong penetration in small and medium-scale corporate customers. Large enterprise customers are not yet a major focus, but management expects this segment to grow

=Corporate sales have grown from ~5% of revenue in FY19-20 to ~50% in FY25.

=B2b..not just rnd and prototyping but also bulk products like digikey

=B2B REPEATATIVE BUSINESS

=We have essentially two types of businesses, one is our online business, another is corporate sales.

=So, generally our corporate sales orders are repetitive in nature, it depends on customer requirements.

=So, even if it is a company like let’s say Tata, Mahindra or Bajaj and if

they just want to set up a test lab or the R&D lab in their company, they are ordering few components, few multimeters or devices from us, it will be one-time purchase.

But even if they are making us some device which is like 400 piece, 500 pieces a month or 400, 500 pieces every quarter, it will be repetitive in nature

=So our B2B orders are generally repetitive in terms of if

they are production based orders. If they are lab based or R&D based orders, small prototyping,

then we have seen that they are repetitive from the type of customer but different products.

-We have strong corporate support or corporate sales team, key account managers to support

corporate customers. And I believe we have learned to make, to sell our products to, let’s say,

small and medium-scale corporate customers.

- Part of that journey I believe that would be to gain these corporate customers coming under the large-scale corporate customers in coming times for us. As of today, we are not doing a lot of large-scale customers

3…ROBU- 2.0

=ROBU 2.0 is centered on creating and developing more of our own brands and products while expanding our current distribution business.

= This strategic direction positions us favorably for long-term success, aligning seamlessly with our goals for the next 5 to 10 years.

-Company itself develops propietry products

-300 products

-special gocus on drones

-We have successfully supplied

drones to a few defense establishments in this H1

-good traction on theses products

=Here our main goal is not to replace imports, but to create products by identifying gaps in availability and pricing.

=We are keeping initial expenditure low, focusing primarily on man-

power and basic machinery.

=To speed up our product development, we’ve set up a small facility for limited-scale manufacturing.

=For higher volumes, we will continue outsourcing until it becomes cost-effective to produce internally.

It focuses on building and scaling our own range of products—especially in the drone category and other emerging tech.

=In long run, we wan to become tech company with our own products

=Over the past two years, this

has become a growing area of emphasis for us. We are seeing encouraging acceptance of our developed products, and we firmly believe that in the times

ahead, locally developed solutions will play a vital role in many strategic applications.

=This will give us a competitive edge in the future, aligning with our long-term goals for the next 5 to 10 years.

4…GOVT SCHEMES

-Atal Tinkering Labs (ATL 2016)

-Drone Shakti + Namo Drone Didi(2022)

-PMKVY (Pradhan Mantri Kaushal Vikas Yojana)

-Make in India + PLI Schemes (Electronics & Drones)

5…NATIONAL COMPETITION

Total recurring participants yearly in India → ~50,000+ students

6…Growth guidance:

-We will continue to grow in future with same rate as past

-Prev growth rate was 50% CAGR and 8% to 10% PAT margin

=========================

NEGATIVES

1..SMALL MARKET

=Company’ s future growth is dependant on b2b business which is repeatitive in nature.

= Otherwise online market is small

2…Import

=Heavy reliance on imports (90% of procurement), primarily from China and the UK, exposes the company to geopolitical risks and tariff fluctuations.

3…Inventory Management:

=SKU proliferation and higher inventory days pose operational risks; management is comfortable due to margin structure and internal rotation/aging metrics.

=Inventory management is a risk but it would also be the strength of the business. Maintaining such a diverse portfolio would require experience in the space which the first mover in the country should benefit from

4…Digikey cometition

DigiKey’s expanded India operation is a material threat, especially as it can now offer local billing, GST, and logistics—key pain points for Indian B2B customers. DigiKey’s scale, product range, and ability to invest in customer acquisition mean it can take market share away from MACFOS

=DigiKey Has Upped its Game in India… …by doing a tie-up with AqTronics Technologies

5…Margin Pressure:

=Margin dilution from rising B2B/corporate sales and large orders; management is countering with higher-margin proprietary products and category expansion.

=EBITDA margins have experienced pressure, dropping from 14% to around 10.2% over the past 2.5 years, primarily due to rapid expansion and the impact of bulk orders.

Disc…invested

5 Likes

https://www.ikigailaw.com/article/651/indias-proposed-drone-law-risks-clipping-the-industrys-wings

These policy changes could have an impact on the company’s sales.

Digikey is now providing pricing in INR on their Indian website.

Anybody who uses both, Macfos and Digikey, can answer following questions?

- For the same product, who is more expensive?

- Who is faster in terms of delivery?

- Who is better in terms of resolving disputes because AqTronics might be helping Digikey for the INR pricing but are they even the ground boots for them to solve customer queries / disputes?

- I think somewhere in this thread, one member had mentioned about deficiency in the after sales service of Macfos. Any recent experience regarding the service?

- Generally 80:20 (Pareto principal) is applicable everywhere. So for the products (like 3D printer, drones etc) for which Macfos claims to have specialization, do they satisfy the customer with ~80-90% parts of that product?

Disclosure - Invested for last ~2 years

1 Like

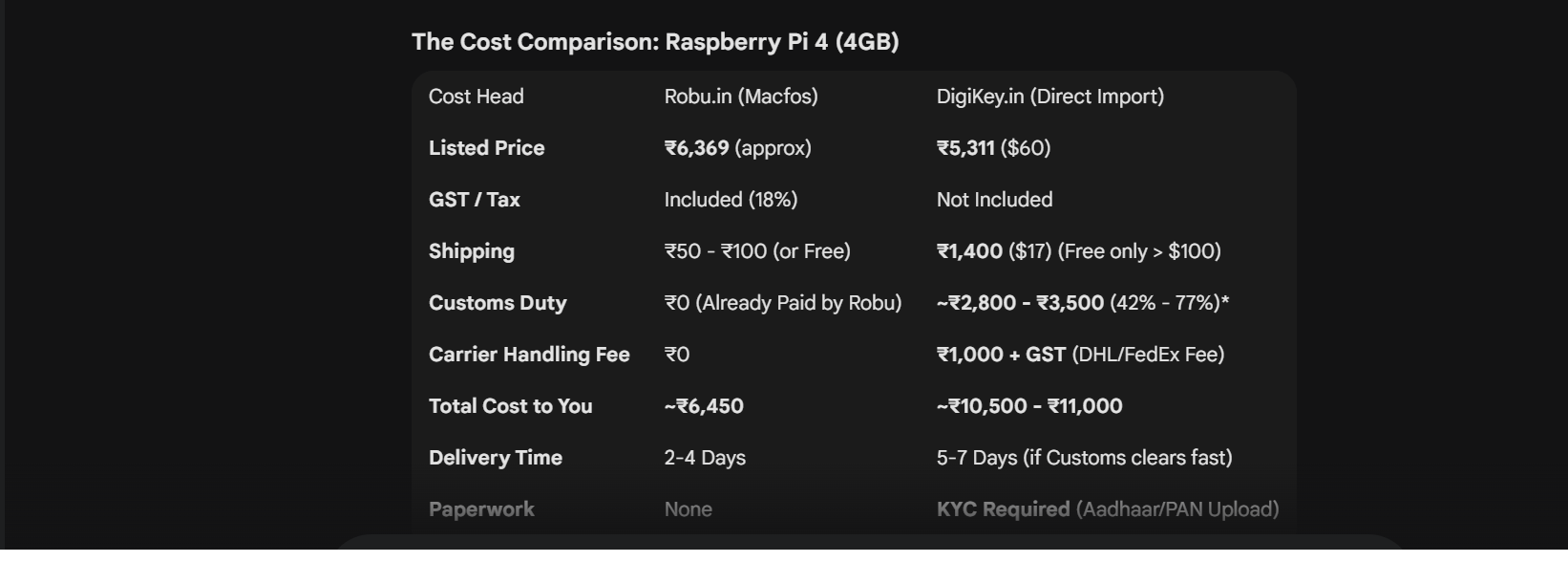

I just compared cost of a popular product on both the platform- Robu and Digikey using Gemini. Have a look.

7 Likes

Thanks Rajesh. This is pretty useful info. This suggest ~40% price gap which to the best of my understanding is quite substantial for this industry.

Delivery time for Macfos is also better than that of Digikey.

1 Like

Sageone has reduced it’s holding in Macfos.

| Sep 2025 | Dec 2025 | ||

|---|---|---|---|

| Macfos Ltd | 4.94% | 2.97% | changed |

4 Likes