This mainly deals with the court case against the promoters for alleged honor killing/abetment of suicide, the case has been long pending in the court and this gives another political angle to it. personally this doesnt mean much to the business as the business is run by next gen now.

4 Likes

The stock has taken considerable beating since the promoter insider issue. And last few days its even more so. Wondering how long this issue is going to linger on stock price? Am not sure whether this charges on promoter will have any consequences on the business of the company.

4 Likes

My perspective on the latest results w.r.t last year:

-

As Operating Cash Flow went negative due to ballooned inventory and receivables, B/S has changed to net Debt from Net Cash.

-

Net Profit seems managed, considering Inventory Growth w.r.t Sales Growth.

-

Sales seems to be pushed, considering Receivables Growth w.r.t Sales Growth.

-

In the Conf. call, management insisted that majority of inventory growth is due to advance buying of raw material. My opinion is that 90% of inventory consists of items other than raw material, considering FY21’s Inventory notes and latest (FY22) P&L statement. //Need to validate after their AR is published//.

Keeping in context the managements commentary in the AR of FY19 about their heightened focus on the operating cash flow and working capital management to ensure better quality earnings, I consider the current development concerning. However, market’s neutral reaction to the stock price shows that my perspective is minority and pessimistic.

Hi Kedar (@zygo23554 ) – Request your current view on this business.

Disc - Not Invested.

9 Likes

Some additional points from call

Biz performance

- Besides Lyra doing well, price based growth mostly. Volume growth is missing since last 2 qtrs and in near future commentary as well.

- Near future commentary at best aligned to inflation in RM, enough to blame around and point at industry issues - RM etc

- EBO - exprerimental stage - no concrete scale plans yet. With most EBO in apparel sector doing well, doesn’t seem like there will be better times to be selectively aggressive.

- Inventory and cash flow - well coverd in above post, responses were around whats happeninb vs what are we going to do about it

Non Biz

- Divergence from Page solid performance ( EBO vs distributor driven channels behaving bery differently on demand), last year it was reverse case

- Street rumors around biz partition among two families- denial as expected

- Feelers well articulated in above post around demand challenges

Interesting that Dollar has recovered well post results and call (though performance and commentary were similar to Lux), inline with broader market. Lux is not reacting much to subdued calls nor participating in mkt pull backs. There doesnt seem to be any immediate triggers as well, combo of price and time correction.

What are possibilities from here? Just to be fair.

- Part of product portfolio doing very well - Lyra & exports. ONN small but seems to do well.

- EBO learnings as mgmt claims if delivers results - can be a new channel. Big IF.

- Most of bad is discounted in current price - could be wrong but one of sign is stock not reacting to bad news and consolidation around previous peak.

- Per Deck marquee names still staying invested. All trust is not lost.

- A consumption story around essentials - available at sub 20 PE. Second largest in category.

Invested

11 Likes

Yesterday I talked to few dealers in my city dealing in rupa, lux and dixcy. Everyone is saying brothers have separated. Also second question in concall was regarding this and I was surprised by the answer. Though mgt denied but they didnt dismissed this outrightly which is expected if nothing is there. @zygo23554 your thoughts will be highly appreciated.

Discl: Invested since 1200

7 Likes

One wrong act from a family member brought down the valuation to almost 50%.

There are 5 members with significant stake in this public listed company. Unlike a conglomerate it is not easy to split the business to everyone’s satisfaction, even if it gets divided into two parts. So the question remains how they will split it without shooting on their own feet.

Nevertheless family run business always have this kind of risk.

On Q4 results -

Economy segment across the market has seen muted performance while premium categories have done well. Volume growth is a serious concern right now across the lower price points where the channel is distribution led. Players with a good EBO footprint have done far better across apparel categories

Omicron disruption was there through Jan and Feb, given that context there appears to be nothing particularly bad about the Q4 results. Peers other than urban market focused Page Ind have done similar numbers

Spike in inventory can be seen in Page Industries, TCNS Clothing and Go Fashion too. Yarn prices are up almost 100% in 18 months, now spinners are taking a break in South India, loading up on inventory was the right thing to do. Page industries conf call specifically makes a mention that sitting on inventory is preferable to lost sales, for this reason their cash balance came down by 150 Cr in Q4. Go Fashion conf call also alludes to the same, their inventory is up 2x YoY for this very same reason.

Operating cash flow for many businesses in FY22 looks muted purely because of the Q4 phenomenon where higher prices spiked inventory value much higher compared to FY21. Reading too much into this wouldn’t be right given that one sees this across sectors and companies

23 Likes

Some buying from promoters

Buying entity has both senior Todi brothers, one can view this in context of rumors around split among brothers - may not put them to rest but directionally seems common interest sustains.

3 Likes

Muted results with EPS of 16.87

0aff65a6-26f2-4b9d-ac38-7462c19397e1.pdf (6.3 MB)

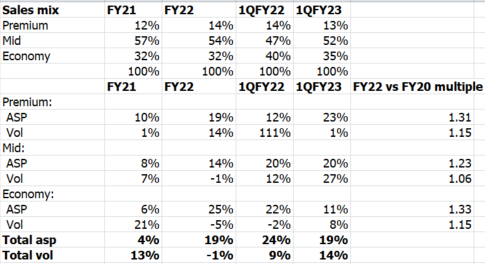

Underlying trends on numbers look decent. High cost inventory impacted nos as to be expected. No laggard between premium, mid premium & economy or brand wise. Broad based growth. All segments especially premium doing reasonably well when looking at sales growth vs value & vol growth. Lyra esp doing well & now ~17% of sales. South inched up yoy from 2% to 4%. 1 way to look at economy segment is ASPs are up 33% FY22 vs FY20, and it grew 8% in volumes this quarter, though on the back of a somewhat favorable base but still. Odds are high I think that margins, cash flows, WC should be back on track from Q3 onwards.

For the next 1-2 years, overall sales & earnings growth outlook should be around 10-12% only. Onus will be on delivery of consistent margins, profitability, free cash flows, resumption of ~20% dividend payouts which can aid multiples to go up. Keen to see what payout they give in FY23, muted in FY22 11% citing covid, vs 18%+ FY20. Imp to see mgnt willing to part with cash.

There are of course factors here not to like. Hence multiples are where they are. For example, CFO has come in from future group for which NCLT has ordered an audit recently. Insider trading case, messy past, unfav treatment to minority shareholders, breakup. Takes long time to get confidence in the market, and that can only happen by consistent delivery. I think management has been trying & has delivered too partially, and the risk reward at current prices are appealing.

Disclosure: invested

5 Likes

This week there was a distributors meet in Dehradoon. And in all likelihood demerger is on the cards. With Ashok & Pradeep todi sperating, this meet-n-greet with distributors was called by Ashok todi to check and see how many distributors would stick by him. Both companies will be launching same products and would now compete against each other. It is now all in distributors hands whose products they would choose to push.(Ashok todi is admired among distributors, he is the company’s face) In all possibilities Lux cozi would remain with Ashok todi and Lyra would go to pradeep todi. Excact details have not yet been disclosed. So take everything with a pinch of salt. I could be wrong too so please do your own due diligence.

P.S- ( My family owns a distributorship )

20 Likes

Lyra and Lux cozi have separate products under them … do you mean if demerger happens we will have banians under Lyra brand and Lux Cozi leggings !!!

1 Like

No that is not what i meant. Among the existing brands, cozi would be with Ashok todi and lyra with pradeep since these two are the most established brands. Ashok todi would then go ahead and launch a new brand in the leggings segment to compete with pradeep’s lyra and as would pradeep todi do to compete with cozi

4 Likes

Won’t they have a non compete clause like how Ambani brothers had?

Mukesh Ambani had to wait for that clause period to end before making Jio commercial operation.

(In 2005 they split up with non compete clause and in 2010 mutually agreed to scrap that agreement).

Source:

While this gets settled, common sense dictates that it is hurting, though silently, the current operations, and future vision because there is no one Lux in the minds of management.

Upcoming festive season followed by winters, reducing raw material pressure might make top/bottom line look better for the rest of the year, but one needs to assess their investments with the impact of potential split.

1 Like

In such cases one will need to see the finer details. Many of the brand/trademark is owned by Biswanath Hosiery Mills, Lux Industries was paying a small royalty to this company for use of this brand. The ownership of BMH is once again with the senior Todi’s and their immediate relatives/spouses.

A protracted legal battle is likely to get stuck for years given the ownership structure. What could happen is a gentleman like agreement in the meanwhile to operate the businesses in parallel till they figure the exact details of the aspects out. Demerger and separation is a lengthy process even in cases where the separation is amicable.

The stock price right now assumes nothing positive can happen to the business over the next 1-2 years, growth if any will be hygienic and not the 20%+ p.a. that the business was delivering over the past many quarters. The stock market tends to price in the expected pain upfront rather than wait for the real scenario to play out. The key question to ask right now would be - what is being priced in?

Volume growth printed a decent number in Q1 after 2-3 Q’s of stagnation.

15 Likes

Lux Ind under its sub brand Venus has signed Salman Khan as a brand ambassador. commercials will soon be aired.

Looks like the family dispute is still not factored in. It should go to 1000 once that is fully priced in. If @Ankit_Agarwal1 is to be believed. Starting a new brand and establishing it would take its own sweet time.

We are still very much in neighbourhood to May 2021 prices

2 Likes

COIMBATORE EPFO:Establishment Search.pdf (62.6 KB)

I read one article from 2point2 Capital. Where we can check the employee count and employee PF payment from EPFO website i found this data only for following

Lux industry ltd Coimbatore

Employee Count is as on Jun 698 and Amount is 567422. Average PF Is 812/Employee

and for

Artimas Fashions Private Limited

Employees count 43 and Amount is 82056

Average PF Is 1908 in this case.

I didn’t found data for the WB Plants.

Also total employee count for the Compony is

2021 - 2382

2022 - 2678

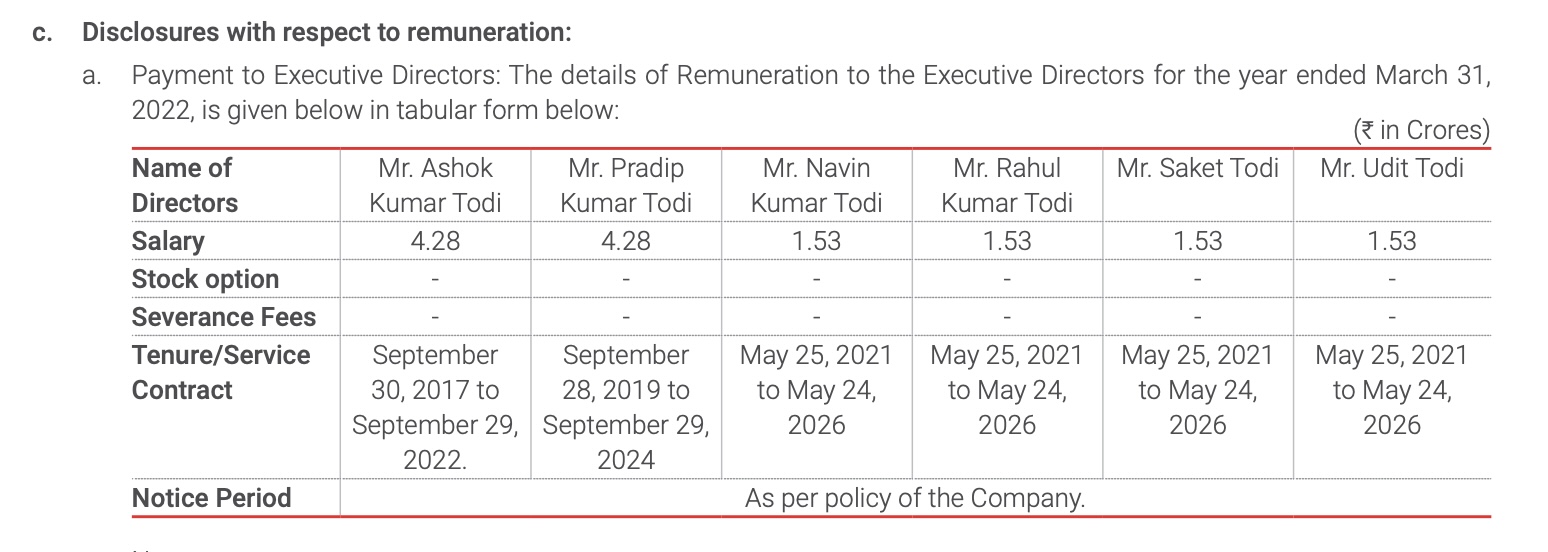

Salaries for promoter is 42800000

Is is 405.49 times the MRE

So when I calculate the Average salary of employee in LUX It is coming only

Yearly 105551.30

Monthly 8795.94

Which for Per day will be come as 293Rs below the government minimum.

Not un expert but went to verify it.

In 2022 AR Both Todi promoter taken 50% increments at the time when they have negative cash flow.

Which seems very low for corporate

2 Likes