Hi,

I am Rahul and working in Software industry.

Learning about investing in stocks since four years. But started investing actively since last 1 year.

Actually i am becoming passionate about investing since last 2 years.

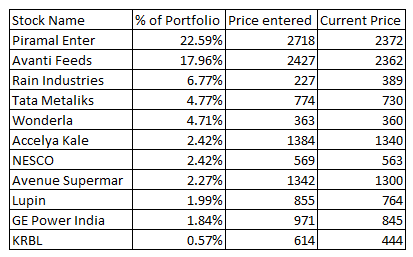

I gone through different portfolios in the VP Forum and i am creating my portfolio now.

can you please provide your valuable feedback on my portfolio.

I am learning from VP forum and appreciate your feedback on my portfolio.

Hi Rahul, Your stocks are very well researched ones in Valuepickr. They all have good prospects of doing well. I have pel, avanti, rain, tata met, accelya and dmart in my pf. I am keeping all for the long term. My only comment on your pf will be the % of the allocation. In my view, <3% allocation is not going to make much impact on the overall pf. More than 15% allocation in a stock also is very risky. You have higher allocation for pel and Avanti. Please go through the recent posts in pel and Avanti threads. There are near-term headwinds. So as retail investors we are not privy to all information to pre-empt allocation changes. It is safer to follow allocation guidelines strictly to minimize any unforeseen headwinds.

You have bought what is already known and over owned in my view . If you do what everyone is doing you will do average by very nature of this act.

In markets you make above average money by betting against the consensus and being right. Otherwise you will do average.

Most of the time what everybody likes carries the most risk as none on the -ves are built into the price and what everybody hates carries the least risk as all the -ves are built into the price.

I hope you get the gist of what i am trying to say. I would give 5 star to this portfolio in 2013-14 that time these were not well known & over owned stocks.

btw you are missing manappuram finance in your portfolio .

What kind of appreciation you are looking for the portfolio over 3-5 years? What earning growth each of these companies will provide on annual basis for the selected period? When / why will you sell these stocks?

@sajijohn Thanks for your feedback. I agree with you that more than 15% is very risky and i would need to stay in the market for long time. Currently, due to my limited knowledge, i found only few stocks which are very interesting. I will definitely keep the 15% limit for each stock in my portfolio while investing. I have one more question. Do i need to rebalance my portfolio frequently once one of my stock increases or decreases the value thereafter allocation will increase upto 40% or more…

@AmitContrarian Thanks for your feedback and manappuram finance idea. I will work to improve my knowledge on various companies and sectors which can help me find better companies in future. One more thing is sometimes the known stocks also gave decent returns like Asian paints, HDFC bank gave more than 8x returns in the last 10 years. Expecting the same for PEL & Avanti since both are still in growth & expansion phase.

@1.5cr Thanks for your feedback on my portfolio. I will work on improving the allocations.

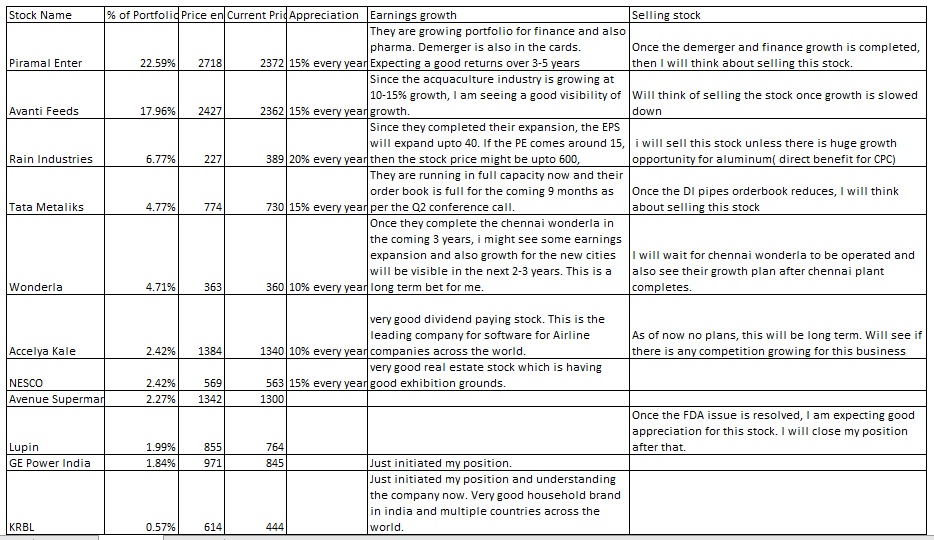

@Yatharth Thanks for your feedback on my portfolio. I am looking for decent appreciation of around 15-20% over 3-5 years. Please find the below screenshot with explanation about appreciation, earnings growth and sell plan for each of the stocks.

The thing is you can count these kind of stocks on finger but many thousands of businesses have disappeared if you look at last 30-40 years.

So, the probability of finding new Asian Paints or HDFC bank is upseenly low whereas probability of finding a business that going to disappear is very high that’s how capitalism works.

Hindsight everything looks so easy and clear but it’s hard to tell what future holds.

I can only mention what I would have done if I were you…I would reduce PEL(I presume the earlier purchases of PEL were higher than your average price) as it reaches overbought territory on the charts and allocates that to Nesco, Tata metallics, Accelya or rain industries. I would keep the Avanti as such and wait for couple of quarters and see it’s performance and take a call. The margin of safety is a factor I consider to decide which one gets more allocation. You have good MOS in rain industries.

You have a decent portfolio with good names and like fellow members have suggested needs a bit of allocation tweaks. Krbl and avanti have roughly the same biz models. The company supplies the feed/seeds and purchases and processes the produce before selling. Both are leaders in their respective domains but are dependent upon commodity prices. So they are cyclical but can survive market weaknesses. Accelya, Dmart and Wonderla are all good businesses to have and pure quality. Wonderla and Dmart in particular have got really long runaways. I would increase allocation to both. Accelya is a stable niche co with good div yield and is an asset to have provided you reinvest the dividends. PEL thread is a good read and people seem to have divergent views on the biz model. Its ur call but a significant part of its biz is a finance operation with a lot of leverage lending to developers in a hostile regulatory environment.

I also feel wonderla and dnart are fine businesses but With all due respect dont yu think cmp is not a good place to buy. Perhaps a 15-20% correction is needed in both? Accelya still seems better priced to buy?

Wish to know your views on current price.

Regards.

Dmart i think can increase its ROE to 30-35% from the current 16-17% and has ample opportunities to retain and reinvest at the same rate. If it does that for the next 10-15 years at the run rate of 15-30 stores per year while maintaining the ROE the valuations while high still seem to be alright to me. However there will be no margin of safety so if anything goes wrong it will impact valuations. The Edelweiss report projects its ROE at 32% by FY20. Wonderla is also a 22%-25% ROE business with a strong advantage as indias only debt free chain of amusement parks. It is based in south india which has leading tourism numbers. Plus 1/2 its land is still not utilized. Chennai park once it comes on board will add to its margins significantly. Given these prospects - I think Wonderla is severely undervalued and Dmart is priced maybe a little on the lower side if assumptions pan out. These values will also keep on increasing/decreasing as the business unfolds.

Accelya while a good business is not able to retain much of its profits and distributes it to shareholders - so dont see the growth more than 10-12% happening. However, it has a tremendous return ratios so great business again and worth holding onto.

with an Index PE of nearly 25 , u stand to lose , all the cos are good , but u will have to short some of them , try selling rain for a profit now . always follow ur intuition , for example check sundaram brake linings ,